The Nifty 50 isn’t just a key benchmark for domestic Indian investors — it’s also widely used by global ETFs, index funds, and institutional investors. Its calculation mechanism directly impacts index fund tracking efficiency, market representativeness, and global capital allocation logic, making it a critical piece of infrastructure in the Indian capital market.

What Is the Nifty 50 Index?

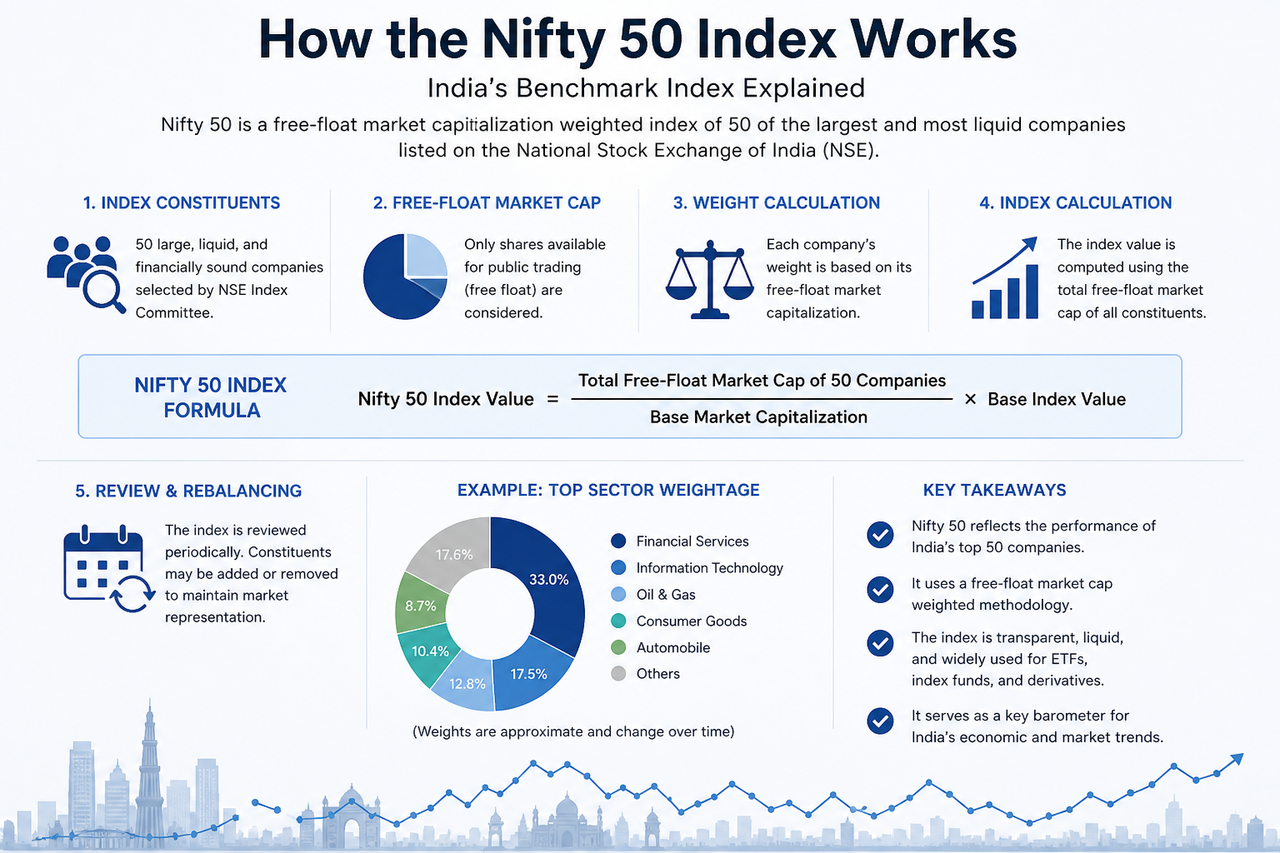

Introduced by the National Stock Exchange of India (NSE), the Nifty 50 is a core stock index that covers 50 large-cap blue-chip companies in the Indian market. It’s widely used to reflect the overall performance of India’s capital market and serves as a key benchmark for ETFs, index funds, and derivative products.

Unlike some traditional indices, the Nifty 50 doesn’t simply track stock price movements — it uses a free-float market capitalization weighting method. This means a company’s influence on the index is primarily determined by the size of its shares actually available for trading in the market.

Because the index spans key sectors like finance, technology, energy, consumer goods, and manufacturing, the Nifty 50 is also considered a vital window into India’s economic structure and industry development trends.

What Is Free-Float Market Capitalization?

Free-float market capitalization is a core concept in the Nifty 50’s calculation mechanism. It refers to the portion of a company’s total market cap that is actually freely tradable in the market.

For example, even if a company has a high total market cap, if a large number of shares are held by founders, the government, or long-term strategic investors, the proportion of tradable shares will be lower. When calculating the Nifty 50, only the value of freely tradable shares is considered.

Free-float market cap is typically calculated as follows:

$\text{Free Float Market Cap} = \text{Share Price} \times \text{Outstanding Shares} \times \text{Free Float Factor}$

The main reason for using this mechanism is that it more accurately reflects the size of the market capital that can actually participate in trading, while reducing the excessive influence of controlling shareholders on index weights.

The overall index value of the Nifty 50 is calculated based on the sum of the free-float market capitalizations of all constituent stocks. The index starts with a fixed base value and is continuously updated as the market changes.

Its core calculation logic is as follows:

$\text{Nifty 50 Index Value} = \frac{\sum (\text{Free Float Market Cap of 50 Companies})}{\text{Base Market Capital}} \times \text{Base Index Value}$

When constituent stock prices rise, their free-float market cap increases, pushing the index upward; conversely, prices falling drives the index downward.

Due to the market-cap-weighting mechanism, price changes in large companies generally have a greater impact on the index. For instance, share price fluctuations at Reliance Industries or HDFC Bank typically affect the index more noticeably than those of medium-weight companies.

How Are Component Weights Allocated?

In the Nifty 50, not all companies have the same impact. The higher a company’s weight, the more its stock price movements influence the index.

Weights are primarily determined by free-float market capitalization, so large financial institutions and technology companies typically hold higher proportions. For example, HDFC Bank, Reliance Industries, and Infosys have consistently been among the top-weighted stocks in the index.

The weight calculation logic is as follows:

$\text{Company Weight} = \frac{\text{Company Free Float Market Cap}}{\text{Total Free Float Market Cap of Index}}$

This structure means that even if some smaller constituent stocks surge significantly, they may not necessarily drive the overall index performance noticeably, while large-cap companies with higher weights can more easily influence the index direction.

How Are the Nifty 50 Constituents Adjusted?

To maintain market representativeness, the Nifty 50 undergoes regular constituent adjustments and rebalancing. The Index Committee typically reassesses company eligibility based on the following criteria:

- Free-float market capitalization

- Stock liquidity

- Average daily filled amount

- Industry representation

- Listing duration and compliance status

If certain companies experience a prolonged decline in market cap or insufficient trading activity, they may be removed from the index; meanwhile, newly emerging large-cap companies may be added.

This dynamic adjustment mechanism helps the Nifty 50 continuously reflect changes in India’s economic structure. With the growth of the digital economy and technology sector, for example, the influence of IT and internet-related companies in the index has also increased.

What Happens During Index Rebalancing?

When the index rebalances, ETFs, index funds, and quantitative institutions typically need to adjust their holdings synchronously to ensure their products continue to accurately track the Nifty 50.

For example, if a company is added to the index, passive funds usually need to buy the corresponding stock; conversely, removed companies may face selling pressure from passive funds. As a result, index adjustments can sometimes have a significant impact on the short-term prices of related stocks.

In addition, rebalancing changes the industry weight structure. For instance, a decline in the weight of the financial sector or an increase in the weight of the technology sector may affect future index trends and market risk structure.

What Is the Difference Between the Nifty 50 and Price-Weighted Indices?

Some traditional indices use a price-weighted approach, such as the Dow Jones Industrial Average (DJIA). In this model, stocks with higher prices have a greater impact on the index.

In contrast, the Nifty 50 uses a free-float market capitalization weighting mechanism, so it focuses more on the overall market size of companies rather than simply the stock price level.

| Comparison Aspect |

Free-Float Market Cap Weighted |

Price Weighted |

| Core Basis |

Company market capitalization |

Stock price |

| Impact of Large Companies |

Higher |

Not necessarily |

| Market Representativeness |

Stronger |

Relatively limited |

| Common Indices |

Nifty 50, S&P 500 |

DJIA |

This design makes the Nifty 50 more suitable as a long-term market benchmark and easier for ETFs and index funds to replicate.

Summary

The core calculation logic of the Nifty 50 is built on the free-float market capitalization weighting mechanism. Its index changes depend not only on stock prices but also on the proportion of tradable shares, company weights, and industry structure.

Through regular constituent adjustments and rebalancing, the Nifty 50 continuously maintains its market representativeness of large-cap Indian listed companies and serves as a critical benchmark for ETFs, index funds, and the derivatives market.

FAQs

How is the Nifty 50 calculated?

The Nifty 50 uses a free-float market capitalization weighting mechanism, calculating the index based on the sum of the free-float market capitalizations of its 50 constituent stocks.

What Is Free-Float Market Capitalization?

Free-float market capitalization is the market value of shares that can actually be traded in the market, excluding shares held by the government, founders, or long-term strategic holders.

Why Do Large Companies Have a Greater Impact on the Nifty 50?

Because the index uses a market-cap-weighting mechanism, stock price fluctuations of large companies with higher weights have a more noticeable effect on the index movement.

Is the Nifty 50 Adjusted Regularly?

Yes. The Index Committee regularly adjusts the constituent stocks based on market capitalization, liquidity, and industry representation.

How Does the Nifty 50 Calculation Differ from the Dow Jones Index?

The Nifty 50 uses free-float market capitalization weighting, while the Dow Jones Industrial Average uses a price-weighting mechanism.

Why Do ETFs Emphasize the Nifty 50's Calculation Method?

A transparent and stable calculation mechanism reduces tracking error and improves replication efficiency for index funds.