Amid growing competition in stablecoin returns and increasing demand for DAO treasury management, “on-chain cash management” is moving beyond simply holding USDC or USDT. It is shifting toward a new asset class that pursues verifiable collateral, real return, and DeFi composability. The key to RWA tokenization is not about superficially labeling TradFi assets and putting them on-chain, but about rebuilding trust and transparency through fund structures, credit ratings, audits, and regulatory licenses—enabling fixed income to circulate on-chain as collateral, settlement currency, and return-bearing instruments.

Starting with the fundamentals of RWA, this article breaks down the overall architecture of OpenEden's fixed-income system, the underlying TBILL assets, the on-chain return distribution mechanism, compliant custody and auditing, how it differs from traditional fixed income, industry challenges, and its market positioning within the on-chain fixed-income space—helping readers understand how OpenEden truly brings real-world assets on-chain.

What Are RWA and Asset Tokenization?

RWA (Real World Assets) refers to physical or financial assets that exist within the traditional financial system—such as government bonds, commercial paper, real estate, and private equity—that are mapped into on-chain tokens through legal and technical processes. This grants holders the corresponding rights to income, ownership, or claims linked to the underlying asset.

Asset tokenization typically involves three layers: the legal layer (a fund, trust, or SPV that holds the assets), the custody layer (a licensed institution that safekeeps the underlying assets), and the technical layer (smart contracts that record shares and handle subscriptions and redemptions). All three are indispensable: on-chain tokens without real asset backing are “air RWA”; off-chain assets without on-chain credentials cannot integrate into DeFi portfolios.

OpenEden chose the asset class with the highest liquidity and clearest risk profile—short-term U.S. Treasury bills—as its entry point. This allows it to build a scalable RWA issuance stack, on top of which it layers return-bearing stablecoins (USDO) and multi-strategy portfolios (PRISM).

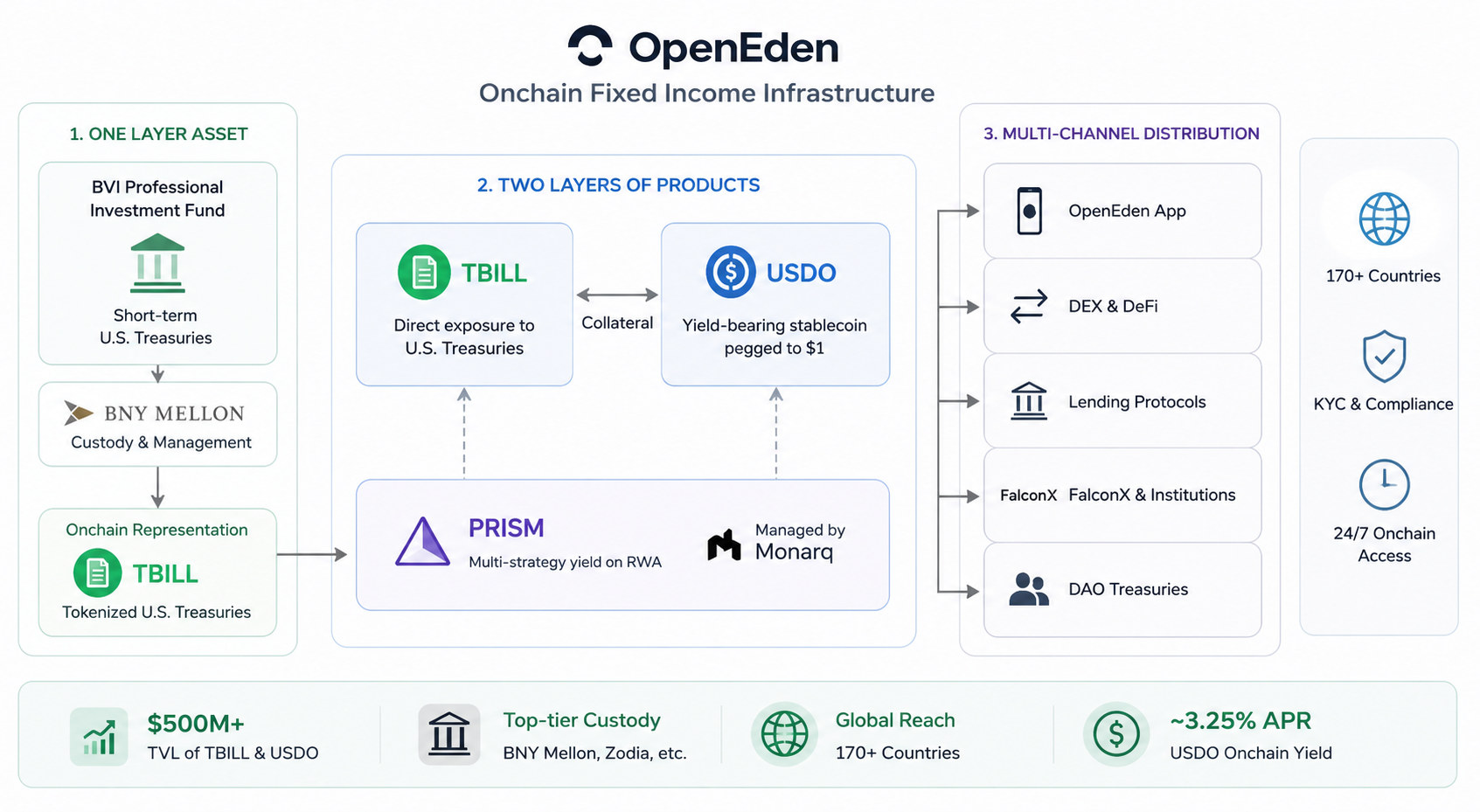

How OpenEden's On-Chain Fixed-Income System Works

OpenEden's on-chain fixed-income system can be summarized as “one underlying asset layer, two product layers, and multi-channel distribution”:

- One asset layer: A BVI professional investment fund holds short-term U.S. Treasuries, which are custodied and managed by BNY Mellon. These are mapped on-chain as TBILL tokens.

- Two product layers: TBILL provides direct U.S. Treasury exposure. USDO is a return-bearing stablecoin pegged to $1, minted against collateral such as TBILL. PRISM overlays a multi-strategy quantitative portfolio managed by Monarq on top of RWA.

- Multi-channel distribution: Through the official app, DEXs, lending protocols, and institutional channels like FalconX, serving DAO treasuries, DeFi protocols, and institutional investors.

Users subscribe to TBILL using stablecoins like USDC, or trade already-circulating tokens on the secondary market. Holders of USDO accrue on-chain returns of approximately 3.25% APR through rebasing or the appreciation of cUSDO. The entire system operates 24/7, breaking through the trading hours and geographical limitations of traditional funds, while maintaining compliance requirements like KYC and accredited investor status.

As of early 2026, the combined TVL of TBILL and USDO has exceeded $500 million, with integrations with custodians like Zodia and BNY, and payment gateways covering 170+ countries. This indicates that it has evolved from a single product into a full-fledged fixed-income infrastructure.

Analysis of TBILL's Underlying Asset Structure

TBILL is the cornerstone of OpenEden’s fixed-income system. Its underlying structure is as follows:

| Layer |

Description |

| Legal Entity |

Professional investment fund domiciled in the British Virgin Islands (BVI) |

| Investment Management |

OpenEden licensed entity + BNY Investments Dreyfus as sub-advisor |

| Underlying Assets |

Short-term U.S. Treasury bills (T-Bills) plus a small cash buffer |

| Custody |

BNY Mellon directly custodies the Treasury holdings |

| On-Chain Mapping |

TBILL token, priced as Fund NAV ÷ Total circulating tokens |

| Credit Rating |

S&P AA+, Moody’s Investment Grade A (among the first tokenized Treasury products to receive such ratings) |

TBILL tokens correspond 1:1 with the fund’s net assets. Subscriptions are made with USDC at the day’s NAV, while redemptions burn the tokens and return stablecoins (net of fees). The fund’s NAV is published after each business day, and holders can view account statements and on-chain reserve proofs through the Dashboard.

The critical feature of this structure is bankruptcy remoteness: the on-chain protocol operator, the fund issuer, and the underlying asset custodian are separate legal entities. Even if a risk event occurs at any level, the underlying Treasuries remain the property of the fund holders and are not commingled with any other liabilities of the protocol.

How OpenEden Distributes Returns On-Chain

OpenEden uses different on-chain return distribution mechanisms for its various products:

TBILL: Returns are not explicitly “paid out.” Instead, they are reflected in the token's NAV, which increases as the interest from Treasuries accrues. Holders realize capital appreciation when they sell or redeem, similar to traditional money market fund shares.

USDO (rebasing model): The balance is automatically adjusted daily using a bonus multiplier. The formula is USDO balance = shares × bonus multiplier. The amount of USDO in a holder's wallet increases day by day, intuitively reflecting an annualized return of approximately 3.25%, with no manual claim required.

cUSDO (non-rebasing model): Designed for DeFi protocols that do not support rebasing, the token quantity remains constant while the unit price rises as return accumulates, providing an equivalent return to USDO. Tokens are freely interchangeable via a permissionless wrapper at any time.

PRISM / xPRISM: Users stake PRISM to receive xPRISM. The value of xPRISM reflects the performance of Monarq's multi-strategy portfolio through a transparent conversion mechanism. The target blended APY is approximately 6%–10%, offering higher returns than single Treasury exposure but with greater complexity.

The common thread among these mechanisms is that return ultimately originates from real-world asset interest (Treasury coupons or strategy excess returns). This is automatically recorded and distributed by on-chain contracts, reducing the need for manual intervention and trust assumptions.

Compliant Custody and Asset Audit Mechanisms

The compliance and audit framework is a core competitive advantage for OpenEden’s RWA model. Key elements include:

- Regulatory Licenses: The TBILL fund is regulated by the BVI Financial Services Commission. USDO and PRISM are issued by OpenEden Digital Limited, which is licensed by the Bermuda Monetary Authority (BMA) and uses a Segregated Accounts Company (SAC) structure to isolate assets.

- Institutional Custody: BNY Mellon acts as both investment manager and custodian for the TBILL fund. BNY, with trillions of dollars in assets under custody, directly holds the underlying Treasuries—not the protocol itself.

- Audits and Ratings: The fund’s financial statements are audited annually per BVI requirements. Key processes in the TBILL Vault are audited by Ernst & Young with no material high-risk findings. Smart contracts are audited by multiple firms, including Hacken and Verichains. S&P and Moody's have given the fund investment-grade ratings.

- Transparency: Daily NAV reports, on-chain reserve proofs, monthly statements from an independent fund administrator, and publicly available smart contract addresses allow holders to cross-verify the consistency between on-chain tokens and off-chain assets.

In March 2026, FalconX added USDO to its institutional collateral and lending system. Prior to that, USDO was already used as a settlement currency for OTC trades by institutions like Galaxy Digital and DeFiance Capital, demonstrating that its compliance and audit framework is gaining mainstream institutional acceptance.

OpenEden vs. Traditional Fixed-Income Investments

| Dimension |

Traditional Treasuries / Money Market Funds |

OpenEden (TBILL / USDO) |

| Trading Hours |

Business days, bound by time zones |

24/7 on-chain transfers and trading |

| Minimum Investment |

Often high for institutions |

Fractional on-chain, but KYC required |

| Composability |

Hard to use in DeFi directly |

Usable as collateral, LP, settlement currency |

| Transparency |

Primarily quarterly or monthly reports |

Daily NAV + real-time on-chain verification |

| Custody |

Banks or brokerages |

BNY Mellon + smart contract recordkeeping |

| Return Form |

Interest or NAV growth |

Rebasing / NAV growth / strategy tokens |

| Regulation |

Single-jurisdiction fund rules |

Multi-jurisdiction compliance (BVI + Bermuda) |

OpenEden does not aim to replace traditional fixed income. Instead, it provides a parallel channel for on-chain native capital—DAOs, protocol treasuries, and crypto institutions—to earn returns linked to U.S. Treasuries while retaining the programmability required for DeFi. For purely traditional investors, existing channels may still be more cost-effective. But for entities already operating on-chain, OpenEden significantly reduces capital idleness and cross-system friction.

Key Challenges Facing RWA Protocols

Despite OpenEden’s leading position in the compliant RWA space, the entire sector faces common challenges:

- Regulatory Uncertainty: Different countries are moving at different speeds on tokenized securities, stablecoins, and RWA, potentially limiting where products can be sold.

- Return Environment: In a Fed rate-cutting cycle, falling Treasury returns will reduce the appeal of TBILL and USDO, intensifying competition with high-return stablecoins.

- KYC vs. Decentralization: Requiring compliance checks builds trust but restricts the reach of permissionless DeFi.

- Cross-Chain and Liquidity Fragmentation: TBILL and USDO are primarily native to Ethereum; while multi-chain cUSDO is expanding, liquidity remains concentrated in a few pools.

- Smart Contract and Operational Risk: Audits reduce but cannot eliminate the risk of bugs, oracle failures, or composability issues with integrated protocols.

- Competitive Pressure: Players like Ondo, Franklin Templeton, and BlackRock BUIDL are entering the space, making TVL and institutional relationships critical battlegrounds.

OpenEden must continuously balance “compliance depth” with “ecosystem breadth” to maintain differentiation as RWA scales.

OpenEden's Future Positioning in On-Chain Fixed Income

In the near term, OpenEden is evolving from a “tokenized Treasury issuer” into an on-chain fixed-income infrastructure. USDO is becoming a tool for institutional collateral and OTC settlement, PRISM addresses multi-strategy return needs, and EDEN/xEDEN align protocol revenue with token holders.

Medium-term goals include applying for a higher-tier license in Bermuda (Class F), expanding into Asia-Pacific compliance hubs like Hong Kong (already working with EX.IO, etc.), embedding TBILL and USDO into more lending and payment use cases, and launching additional tokenized fixed-income products.

The long-term outlook depends on whether the RWA super cycle endures. If on-chain treasury management, return-bearing stablecoins, and tokenized Treasuries become standard DeFi building blocks, then OpenEden—with its credit ratings, BNY custody, and vertically integrated fund structure—could secure a key position in the “on-chain Treasury” niche. Conversely, if regulations tighten or yields remain low for an extended period, growth will likely rely more on institutional customization than retail adoption at scale.

Summary

OpenEden’s RWA model uses a four-layer structure—licensed fund, institutional custody, investment-grade ratings, and on-chain smart contracts—to safely and transparently map U.S. Treasury returns into composable on-chain assets. TBILL provides direct exposure to Treasuries, USDO packages that return into an everyday on-chain dollar, and PRISM extends into multi-strategy returns.

Understanding OpenEden means understanding one typical path for RWA to move from “narrative” to “infrastructure”: trust comes from TradFi compliance and custody, value comes from real interest, and liquidity and composability come from DeFi. When all three are in place, real assets can truly come alive on-chain—and that is the core logic driving OpenEden’s continued expansion in the on-chain fixed-income market.