Curve’s “optimal trading path” is not a multipath routing algorithm in the traditional sense. Instead, it uses mathematical curve design and liquidity structure optimization to allow stablecoin swaps to settle efficiently within a single pool. This design reduces path complexity while lowering slippage and fee related losses.

In decentralized finance, stablecoin trading often relies on multiple liquidity pools or cross protocol routes. Curve internalizes this process through a dedicated mechanism, allowing funds to complete the most efficient swap within a single structure. This capability makes Curve a core component of stable asset trading infrastructure.

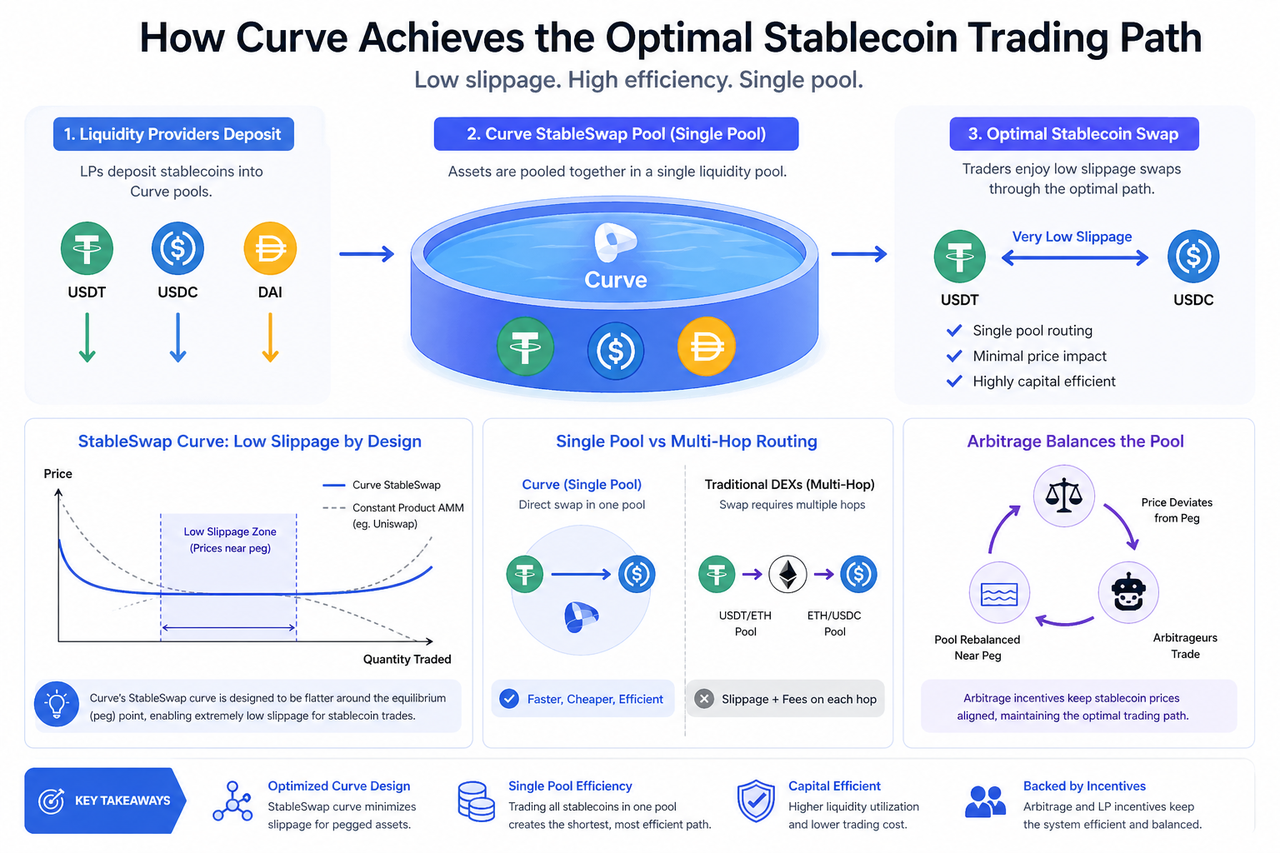

The Core Mechanism Behind Curve’s “Optimal Trading Path”

How the StableSwap Curve Defines the Trading Path

At the center of Curve is the StableSwap curve. It combines the constant product model used by traditional AMMs with the constant sum model, allowing the trading curve to take different shapes across different price ranges.

When asset prices are close to their peg, the curve becomes flatter, so trades produce almost no slippage. When prices diverge, the curve gradually shifts into a more protective structure to prevent liquidity imbalance. This dynamic structure is what fundamentally defines the “optimal shape” of the trading path.

How the Single Pool Structure Reduces Path Complexity

Unlike DEXs that require multihop swaps, Curve uses a single liquidity pool to support multiple stable assets, turning the trading path from “multinode routing” into “direct single pool execution.”

This structure reduces the cumulative slippage that can occur across pools and lowers uncertainty in the trading path. Once funds enter the system, they can settle through the shortest path, improving overall trading efficiency.

How Liquidity Distribution Affects Trading Efficiency

Curve’s liquidity providers collectively create market depth, and the way their capital is distributed directly affects the quality of the trading path. When liquidity is concentrated around the central price range, trades rarely move away from the optimal path.

This structure allows Curve to maintain a consistently low cost trading environment for stablecoin swaps. Even under higher trading volumes, it can preserve path stability.

The Dynamic Balancing Mechanism When Prices Move

When an asset moves away from its peg, the StableSwap curve automatically adjusts trading weights, encouraging arbitrageurs to step in and correct the price deviation.

This mechanism not only restores price equilibrium, but also indirectly optimizes the trading path through arbitrage, allowing the system to return to a low slippage state.

Differences Between Curve and Traditional DEX Path Models

| Dimension |

Curve |

Traditional DEXs, such as Uniswap |

| Path Structure |

Optimal single pool path |

Multipool routing path |

| Slippage Performance |

Extremely low for stable assets |

Depends on liquidity depth |

| Trading Logic |

Curve optimized path |

Routing algorithms search for a path |

| Suitable Assets |

Stablecoins / similar assets |

All asset types |

Curve’s advantage lies in “path internalization,” meaning the trading path is determined by the mathematical model itself rather than by external routing calculations.

Curve’s Role in DeFi Path Systems

Curve does more than provide trading functionality. It is also used by many protocols as DeFi path infrastructure. Lending protocols, yield aggregators, and stablecoin systems often integrate Curve directly to reduce complexity at the trading layer.

In this structure, Curve acts like a “default shortest path layer,” allowing assets to move through the DeFi network with the fewest possible intermediate steps.

Conclusion

Through its StableSwap curve design, single pool liquidity structure, and dynamic arbitrage balancing mechanism, Curve creates an “optimal path” for stablecoin trading. Its core strength is not traditional routing optimization, but an endogenous mathematical model that compresses the trading path directly at the protocol layer into the lowest cost structure, significantly improving swap efficiency for stable assets.

FAQ

What does Curve’s “optimal trading path” mean?

It refers to a mechanism that uses the StableSwap curve and single pool structure to settle stablecoin trades within one liquidity pool at the lowest possible slippage.

Does Curve use routing algorithms to optimize trading paths?

It does not rely on traditional multipath routing algorithms. Instead, it uses a mathematical curve to directly determine trading path efficiency.

Why can Curve reduce slippage?

Because when prices are close, Curve uses an extremely flat trading curve, so trades create almost no price impact.

How is Curve different from regular DEXs in path design?

Curve uses an endogenous single pool path structure, while regular DEXs rely on multipool routing to find the best trading path.

How does Curve’s arbitrage mechanism optimize trading paths?

When prices deviate, arbitrageurs correct the imbalance, helping the curve return to a stable state and restoring the optimal trading path environment.