The first quarter of 2026 was a busy and transformative period for players in the payments sector.

On January 11, Google introduced the Universal Commerce Protocol (UCP) at the National Retail Federation Annual Conference in the US, seeking to establish a universal language for AI Agent-driven commerce. That same week, Revolut announced it would be among the first EU payment methods compatible with Google AP2, PayPal disclosed its acquisition of Cymbio—a merchant directory synchronization company—and Mastercard launched the Agent Suite.

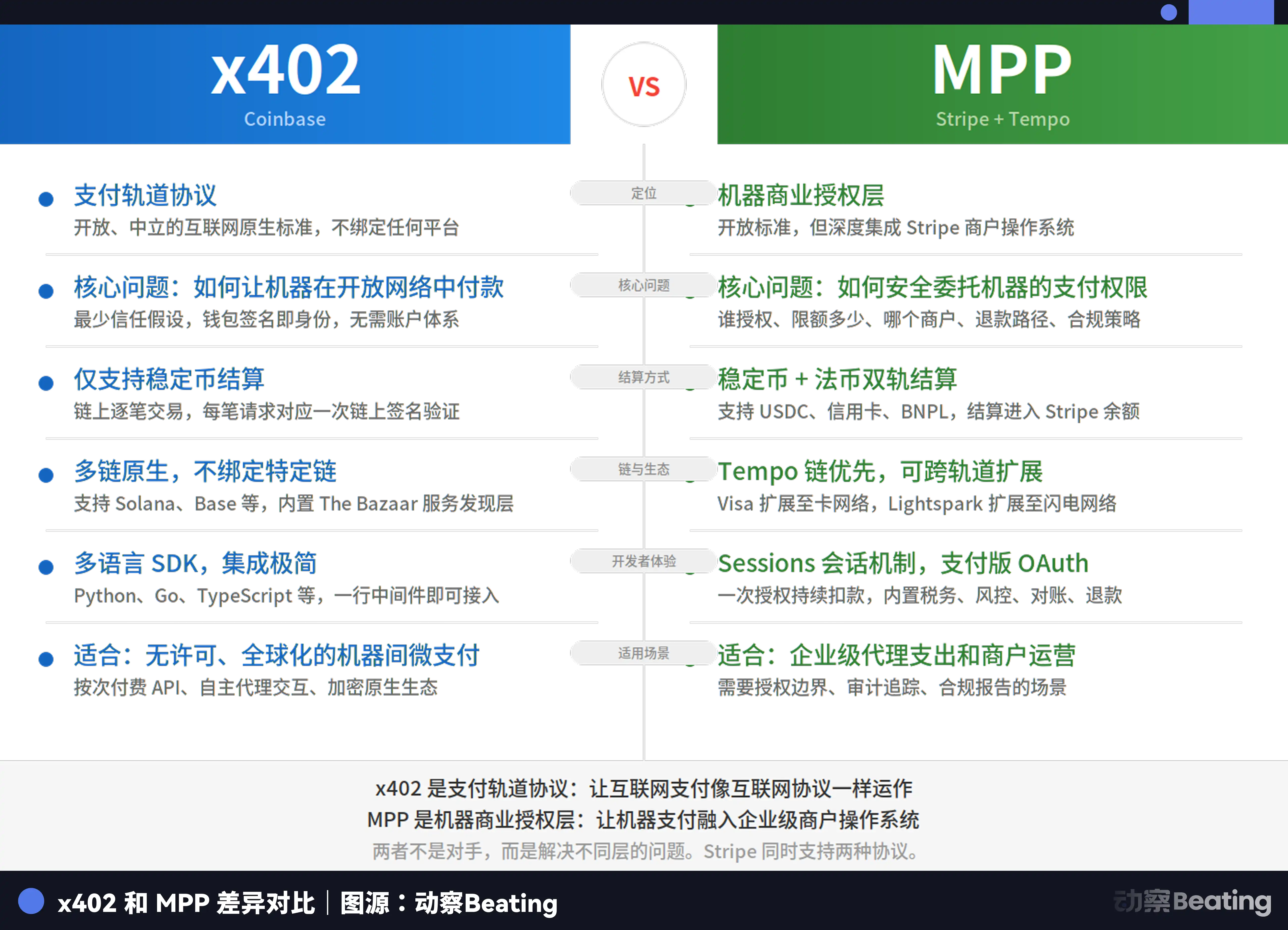

In February, Coinbase officially released Agentic Wallets, allowing AI Agents to manage their own wallets for autonomous spending, earning, and crypto asset trading. The x402 protocol was deeply integrated with Google’s ecosystem, processing over 50 million transactions.

March saw an even greater surge of activity. Circle unveiled Nanopayments, Ramp launched Agent Cards, Mastercard announced its acquisition of stablecoin infrastructure provider BVNK for up to $1.8 billion, and the Tempo chain—incubated by Stripe and Paradigm—went live, accompanied by the launch of the Machine Payments Protocol (MPP).

In just three months, the industry witnessed more than a dozen major moves—some encouraging, others concerning. While these events may appear disconnected, they all signal a fundamental shift: as the cost of machine-to-machine transactions approaches zero, payment giants’ true adversary is no longer each other, but the concept of zero cost itself.

Key Events Recap

Zero-Cost Era: No Winner-Takes-All

Just six months ago, the debate was about who would legislate for AI Agents. Stripe’s ACP, Google’s AP2, and Mastercard’s Agent Pay each pursued their own approaches, vying for the right to define the landscape.

Today, that battle has effectively ended—not because any single party prevailed, but because all stakeholders recognized that winner-takes-all is not possible.

Google’s UCP, launched at the start of the year, integrated all mainstream standards and governs commercial transactions within the Search and Gemini ecosystems. The MPP protocol, jointly released by Stripe and Tempo, supports integration with Mastercard and Visa, enabling autonomous machine payments. Mastercard’s Agent Pay manages auditable authorization for high-value transactions.

What was once a territorial contest has become a process of boundary-setting. The current protocol landscape means decisive competition has shifted elsewhere.

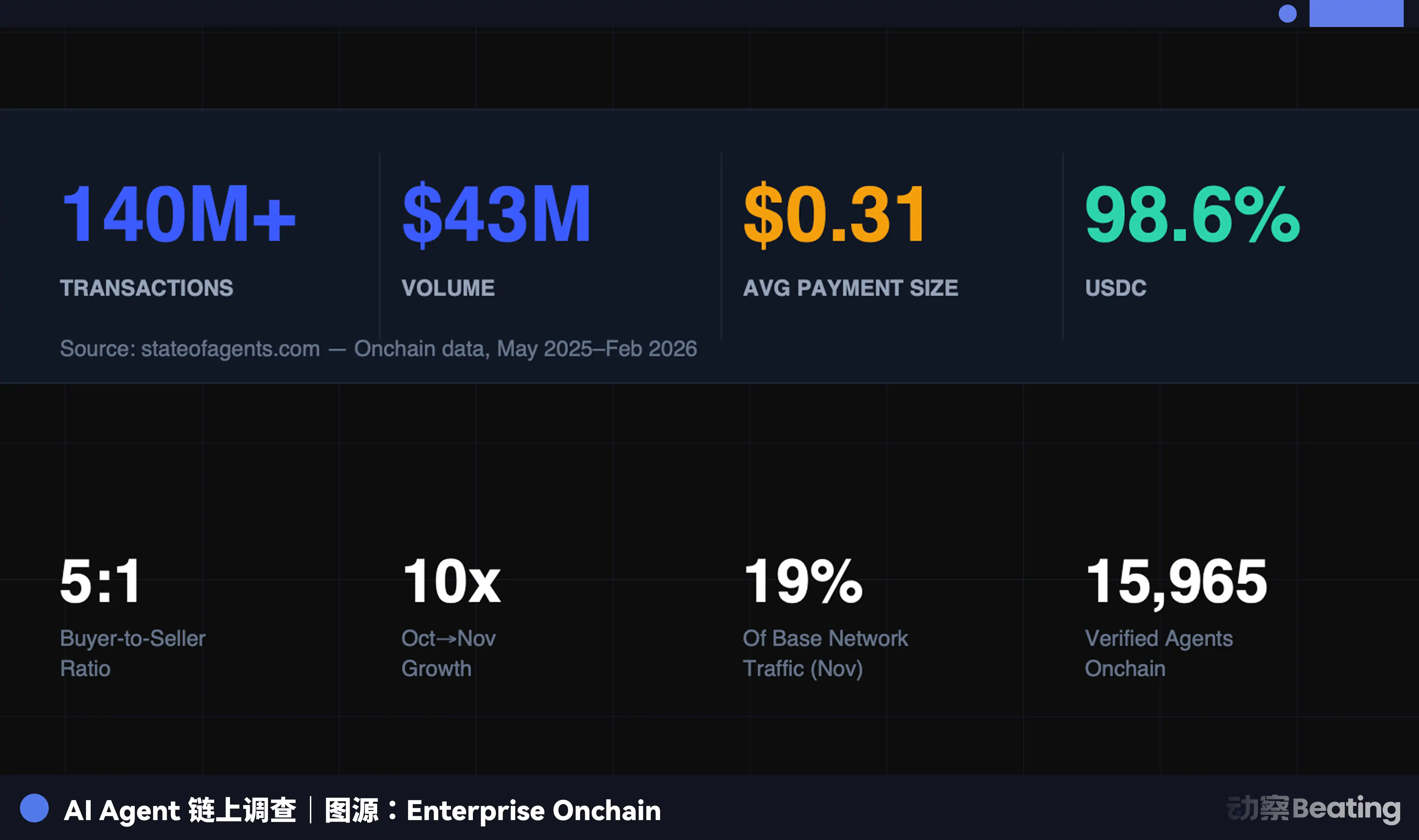

Let’s examine data from Enterprise Onchain: Over the past nine months, AI Agents completed 140 million payments totaling $43 million, with 98.6% using USDC. The average transaction value was $0.31, and more than 400,000 AI Agents now have purchasing power.

Here’s what these numbers reveal:

First, autonomous machine transactions: 140 million payments were executed without human intervention, bank approval, or credit card verification. Code interacts with code, protocol with protocol—processes that once required human signatures, reconciliation, and settlement are now handled entirely by machines.

Second, extremely small transaction amounts: With an average value of $0.31, most payments are micropayments for API calls, computing power, or data access. In traditional payment systems, such transactions are impossible, as minimum card network fees would exceed the transaction value.

Third, costs approaching zero: By leveraging the x402 protocol, payments are embedded directly in HTTP requests. Circle’s Nanopayments aggregates thousands of micropayments off-chain and periodically batches settlements on-chain, reducing developers’ per-transaction gas fees to zero. Circle absorbs on-chain settlement costs at the batch level.

Machine-to-machine transactions eliminate checkout pages, payment gateways, and intermediaries—this is the source of concern.

Currently, zero cost is limited to machine-to-machine micropayments. Stablecoins are not truly free; on Ethereum mainnet, gas fees for a small stablecoin transaction can exceed 20% of the transaction amount. Stripe created Tempo specifically to address this challenge.

On the consumer payment layer, card networks still offer advantages that stablecoins cannot replicate: unified consumer protection, consistent user experience, and flexible routing capabilities as a foundational abstraction.

Yet, the underlying concern remains unchanged. In high-frequency machine micropayment scenarios, zero cost is already a reality—and the gap is widening rapidly. Deloitte predicts the global Agent market will reach $4.5 billion by 2030. This is an entirely new transaction universe, tearing open a massive gap at the edge of traditional payments.

The Giants’ Response: From Toll Collectors to Bridge Builders

Faced with the threat of zero cost, traditional payment giants have adopted varied strategies, all rooted in the same logic: if fees can’t be collected in machine-to-machine micropayments, then control the bridges between legacy and new systems and charge there.

Visa’s approach is integration, not resistance. USDC settlement is now live in the US, with crypto-friendly banks like Cross River Bank and Lead Bank onboard. Visa Direct supports stablecoin preloading and direct payments.

In short, you can use stablecoins, but you must use Visa’s pipes. Visa also helped develop MPP, extending the protocol to card payment scenarios—a classic case of joining when you can’t beat them.

Mastercard spent $1.8 billion to acquire BVNK, gaining the bridge between fiat and stablecoins. BVNK enables fiat-stablecoin conversion across all major blockchain networks in more than 130 countries—precisely the critical infrastructure for the AI Agent payments era.

Mastercard’s Chief Product Officer Jorn Lambert responded directly to claims that stablecoins threaten the card business, stating the card business remains solid and the acquisition is to expand into new areas like remittances. Fundamentally, as stablecoin transaction volumes surge, controlling the settlement bridge between fiat and stablecoins means controlling the flow of value.

Stripe’s ambitions are unmatched. It owns its own blockchain, Tempo, its own protocol, MPP, and the Open Issuance platform, which lets enterprises issue their own stablecoins and share reserve yield—this is vertical integration at its finest.

Tempo, MPP, and Open Issuance together mean Stripe is no longer just a payment processor—it’s becoming a foundational infrastructure operator for the AI Agent payments era.

PayPal followed a different path. Its acquisition of Cymbio was about controlling merchant directory distribution, not payment channels. Cymbio’s Store Sync technology allows merchants to synchronize product catalogs across multiple AI shopping platforms with one click, eliminating the need for small and medium merchants to adapt to each AI platform individually.

As AI Agents replace humans in product discovery, whether a merchant’s catalog is visible to AI becomes a matter of survival. PayPal is betting that in the Agent Commerce era, being discovered by an Agent is valuable in itself.

Ramp’s Agent Cards represent an interesting middle ground. They issue virtual cards to AI Agents, operating on the Visa network. Each transaction is dynamically authorized and does not expose real card information—essentially turning corporate expense cards into Agent wallets.

Whether this is a continuation of traditional payments or simply a transitional solution remains to be seen. If machine-to-machine transactions ultimately shift to native stablecoin pathways, Agent Cards may represent the last opportunity for traditional card networks in the new era.

The New Era: Where Does Profit Come From?

One question remains largely unanswered: On the zero-cost track, transactions themselves generate no fees. So, who profits?

Circle’s Nanopayments earns revenue from infrastructure service fees; Stripe’s Open Issuance profits from reserve yield; Mastercard, following its acquisition of BVNK, profits from fiat-stablecoin conversion services.

All three models share a common trait: the fee has shifted from the transaction itself to the conditions enabling the transaction. They are essentially infrastructure rental, not transaction taxes.

This marks a fundamental shift in business models. For fifty years, payment networks’ moat was network effects: more merchants led to more consumers, and vice versa, fueling a flywheel that profited from scale-based commissions.

In the world of machine-to-machine transactions, that flywheel breaks down. Machines only need a stable, programmable, low-cost settlement layer—whoever provides it becomes the new infrastructure provider.

Payment giants will survive; that’s not in doubt. The real uncertainty is: in an industry powered by commissions, as commissions lose their importance, where does power go?

Statement:

-

This article is reprinted from [BlockBeats], copyright belongs to the original author [Kaori]. If you have any objections to reprinting, please contact the Gate Learn team, who will handle the matter promptly according to relevant procedures.

-

Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute investment advice.

-

Other language versions of this article are translated by the Gate Learn team. Without mentioning Gate, you may not copy, distribute, or plagiarize any translated article.