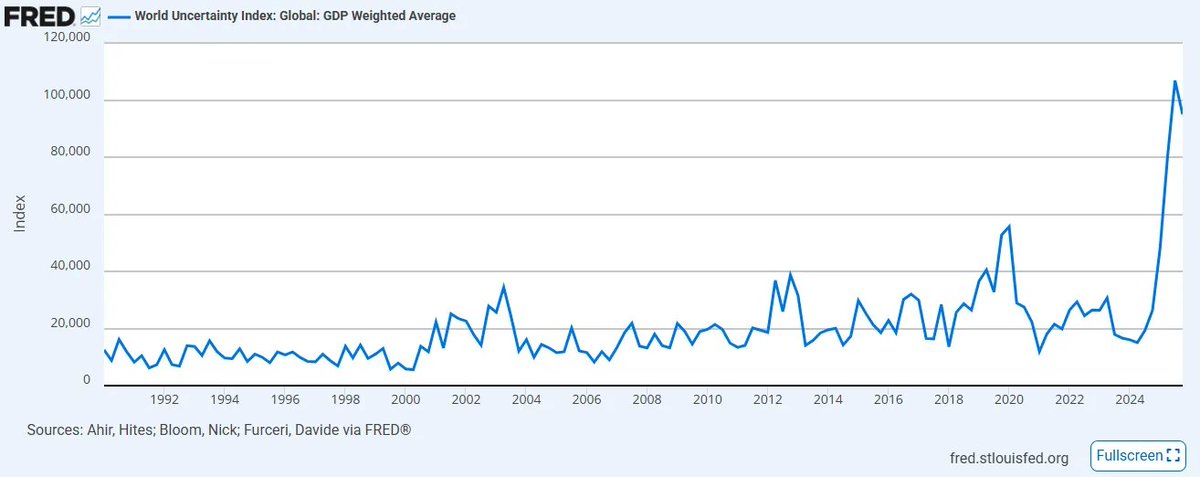

The IMF-constructed World Uncertainty Index registered its highest level recently since its inception in 2008. The lack of directional and coordinated clarity around policy and trade has meaningfully worsened sentiment since its prior all-time and is likely to go higher, especially as shaky old world alliances are thrust into an unprecedented global conflict in the Middle East. Simultaneously, the accelerating adoption of exponential technology like AI has only deepened the confusion, for experts and laypeople alike, about how productivity-driven deflation reconciles with a credit-driven, inflationary monetary framework. To make matters worse, private credit is experiencing an epic meltdown for having aided this fragile capital supply chain by manipulating the price of capital at the cost of liquidity.

Just during this past week, we saw:

-

Iran naming Mojtaba Khamenei the new supreme leader as U.S. crude oil surged nearly 40%, marking its largest weekly gain since 1983

-

Anthropic suing the Defense Department over “Supply Chain Risk” designation

-

Blackrock capping withdrawals from its $25Bn direct lending fund at 5% after investors sought to cash in nearly 2x that amount

No one can expertly prognosticate what is going to happen on these delicate issues, because these are unprecedented events (though worth noting that the above three events are not independent of each other; more on that later). At moments like this, it is important to step back and re-underwrite not what you don’t know, but what you know with absolute certainty that is, in fact, responsible for directly causing the above mentioned events. As Sherlock Holmes famously instructed Watson, “when you have eliminated the impossible, whatever remains, however improbable, must be the truth”; the task therefore is not to chase the unknowable, but to anchor yourself to what is already, irrefutably true, directly at the root of the problem.

With that mindset, there are three such certainties in the uncertain decade ahead that have only become stronger in my opinion. When I say certain, I mean these are 100% probability events. The only true unknowns are the exact timing and, to some extent, the exact severity, but the arrival of each event catalyst is guaranteed within our lifetimes. And by anchoring ourselves to what is not in question, we can transform a pervasive sense of helplessness into genuine belief of conviction about how to prepare for the world ahead.

None of what you will read below is meant to be sensational. It is merely a compilation of facts.

Certain Truth #1: The global population pyramid is inverting, and every asset class built on top of it will follow

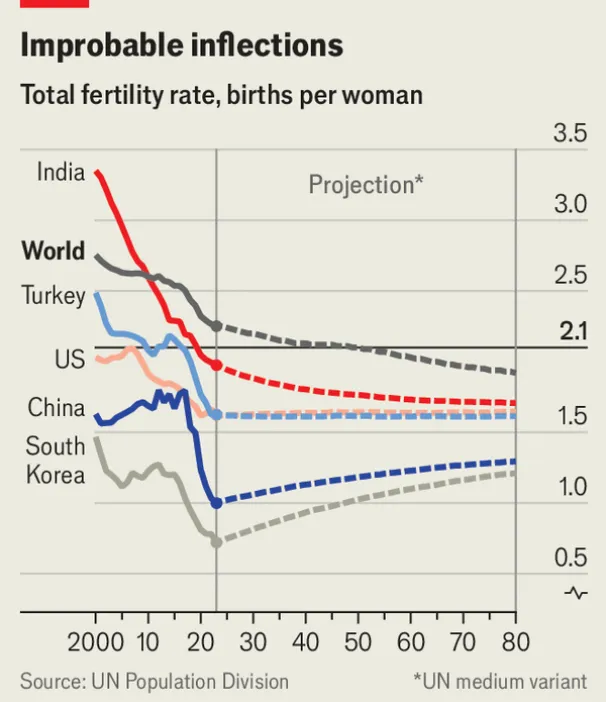

In 2019, the World Economic Forum sent a seismic tremor through institutional consensus when they declared: “For the first time ever, there are more people over 65 than under 5.” Seven years on and a devastating global pandemic later, societies all across the world are now feeling its heavy weight and wrath, and it’s only getting worse.

3

3

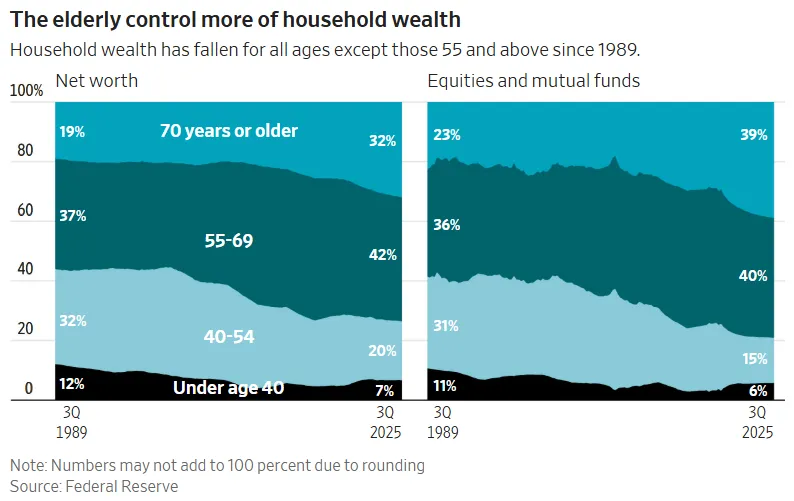

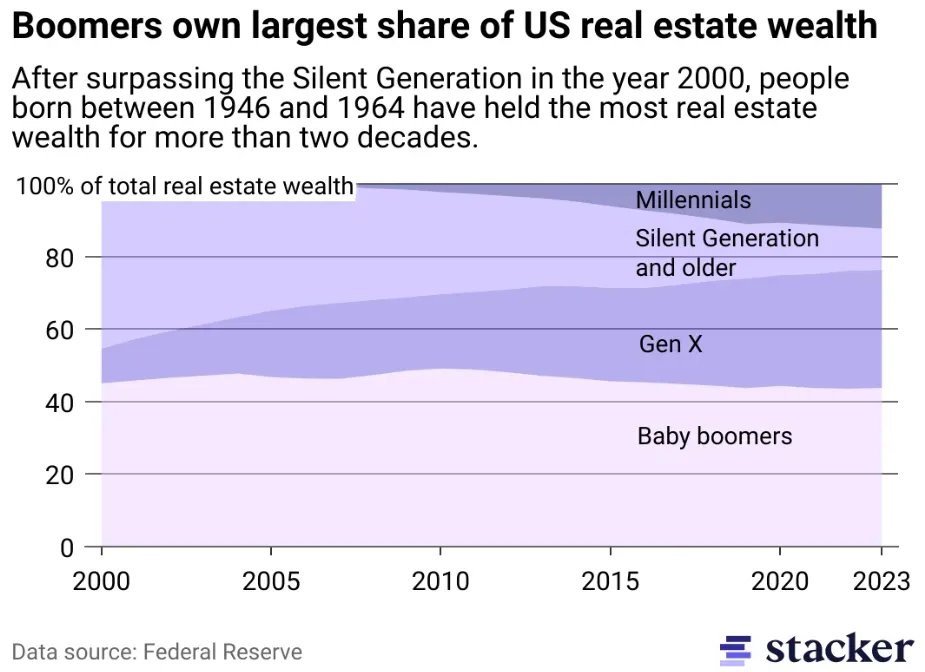

Global fertility rates are dangerously close to falling below replacement level and in developed markets, that threshold is already a distant memory. Declining birth rates combined with aging populations will produce the highest dependency ratio human civilization has ever known. To make matters worse, the gerontocracy across the developed world will eventually need to access liquidity to fund their ever-lengthening lifespans. The result will be a great generational wealth transfer: one where the accumulated financial assets of an entire aging cohort must find deep liquidity to exit through. That pool of capital is staggering in scale: U.S. equities alone sit at approximately $69 trillion in total market capitalization (where Boomers alone own roughly $40 trillion+), while U.S. residential real estate adds another $50 trillion (and Boomers and older generation is estimated to own over $20-25 trillion despite representing less than 20% of the population). Together, nearly $60-70 trillion in wealth will need to exit the capital asset system, and it will all be looking for the exit right at the time when the next young demographics have decreasing income pricing power and little disposable wealth.

4

4

When that generation eventually becomes forced sellers, it will almost certainly usher in a prolonged period of asset deflation. The underlying physics of the stock market are, at their core, just trends in demographic; markets rise when the population of asset-accumulating savers grows reliably toward retirement. Nowhere is that more obvious that the fantastic implosion of “private credit,” another $2 trillion time bomb sitting in pensions, endowments, life insurance companies all in the near-fraudulent business of artificial liquidity transformation against the youth).

But once the younger generation internalizes that they are being cast as exit liquidity for their parents, they will simply stop stepping up. Nobody willingly buys a forever-declining chart. This is precisely why the Trump administration is pushing child investment accounts. It is why equity tokenization is being aggressively pursued: to make it easier than ever for foreign capital to absorb U.S. equities. And it is why RIAs are defaulting to computerized model portfolios at scale, without pausing to ask the most important question of all: but why?

These are all mechanisms designed to blunt the inevitable: there will be no bid when Boomers price-inelastically sell unless you conscript the young, the foreign, or the machines. Consider the design of the Trump child account itself, which forbids diversification of any kind. Bonds, international equities, and alternatives are explicitly prohibited; only U.S. equity index exposure is permitted. And after age 18, the account converts to an IRA, complete with severe withdrawal penalties, a deliberate straitjacket compared to a standard UTMA account, which grants full liquidity with no restrictions upon adulthood. What becomes obvious is that this is, in fact, not a wealth-building vehicle for children. It is a one-way, forty-plus-year locked conduit that has been engineered, whether intentionally or not, to turn an entire generation into captive exit liquidity for the one that came before it.

Nowhere will this be more obvious than in real estate, which sits at the epicenter of the greatest asset bubble of all time. One generation’s exploitation of duration by the deliberate, decades-long hoarding of fixed supply has severed home prices entirely from the underlying economic productivity of their communities. For most residential and commercial real estate (excluding trophy assets which operate within an altogether different economy), affordability is a fiction. The generation whose wages simply never kept pace will not be buying these homes at current prices. For those lucky enough, many properties will be passed down naturally to children. In the cases where there are none, they will eventually be sold into a market with structurally fewer bodies and fewer household formations. Again, the arithmetic is brutal and unavoidable: an epic housing deflation is not a possibility. It is a conclusion.

To accelerate the liquidity events, this deflationary pressure will be perversely compounded by rising property taxes as real estate completes its transition from investment asset to consumption good, one increasingly indexed to government expenditure inflation: public schools, social services, municipal infrastructure, and the generally swelling cost of services over goods. The fiscal pressure alone will force selling that markets were never built to absorb. Mayor Mamdani’s move to explore a property tax increase in New York City is not an anomaly; it is a harbinger for the grand bargain of the “Inert Capital Asset Tax” era to come, and it will be especially acute in cities where wealth inequality has already reached levels that make the status quo politically unsustainable. This brings me to my second certainty.

Certain Truth #2: Wealth inequality will reach a breaking point, and the wealth tax will be the answer nobody wanted

The demographic challenge described above is best understood as a vertical collapse, a population pyramid slowly inverting, its base hollowing out as the weight of elderly dependents above grows too heavy to support. Yet in addition to the vertical demographic implosion to come, there is a persistently widening gap along the horizontal axis as well that is far more sinister: income inequality.

When we encounter headlines such as “10% of the World Population Owns 76% of Global Wealth” (Source: UN’s World Inequality Report 2022), it is important to understand a critical distinction. This is not a story about some countries getting disproportionately rich while others fall behind. It is a story about what is happening within each country, globally: the gap between the wealthy and everyone else is widening everywhere, across every geography, and accelerating across every measurable time horizon.

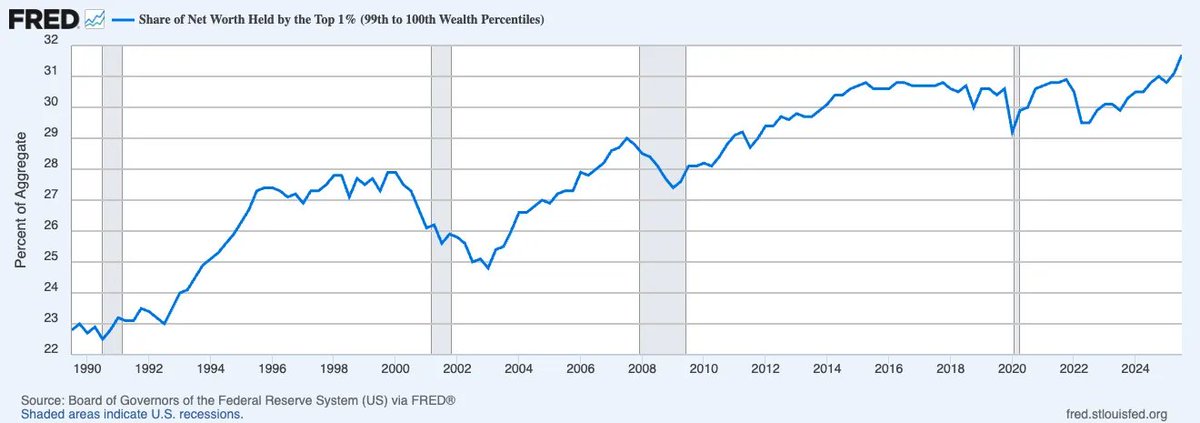

And to be more precise as careful readers will have already noted, the problem extends beyond income inequality: it is wealth inequality. At no point in recorded history has a greater concentration of wealth been held by the top percentile than right now. Consider how the share of net worth held by the top 1% in the United States has marched relentlessly upward, now approaching one-third of all national wealth.

The distinction between income and wealth is critical here. Income, as a transactional construct, or “money in motion,” functions as a market-rate measure of productivity. Wealth does not. Non-capex wealth is “money at rest”: not inherently productive, and in a credit-driven zero-sum game, a drag on the circulating money supply that an economy depends on to function. When wealth concentrates like it is doing today, it stops moving, and the consumption velocity that sustains broad economic activity quietly suffocates.

In that scenario, without meaningful productivity growth to create new resources, a wealth tax, despite its ongoing controversy, becomes an almost inevitable outcome of fiscal nihilism. This is because the only viable mechanism to rebalance the equation is to tax wealth itself, no matter how imprecise or unsound it may be. A wealth tax can be considered simply to be the mirror image of social security; as one extracts from the bottom to subsidize survival, the other extracts from the top to sustain it. Both are, in their own way, a confiscation of unrealized events. The only difference is the direction: one runs vertical (ie. from the young), the other horizontal (ie. from the rich).

The implementation process has already begun. On February 12, 2026, the Dutch House of Representatives passed a landmark piece of legislation that will impose a flat 36% tax on the annual increase in value of stocks, bonds, and cryptocurrencies, regardless of whether those assets have been sold. The bill now awaits Senate approval, where the parties that supported it already hold a majority, making passage all but certain. Whether this is morally defensible, mathematically sound, or legally enforceable is beside the point, and those who fixate on these questions will miss the bigger plot entirely. The right question is far simpler and far more consequential: what happens when this comes for the rest of the world?

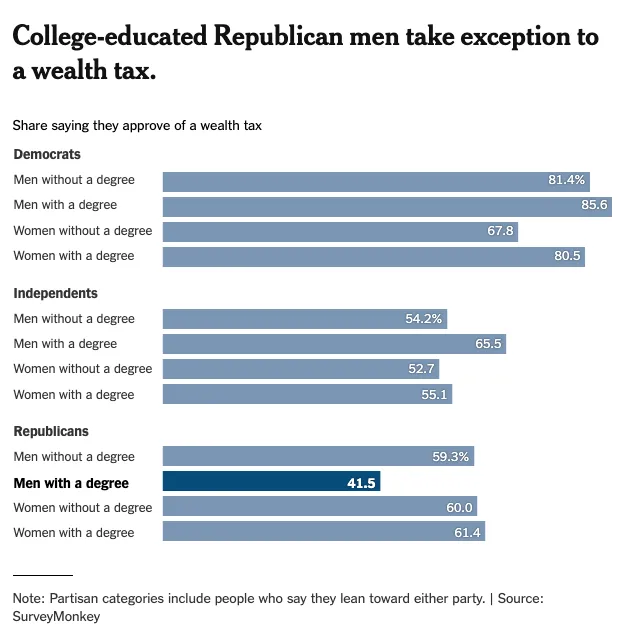

Look no further than the birthplace and last bastion of capitalism itself: America. Consider the New York Times survey on public sentiment toward a wealth tax. Support is nearly universal across every demographic segment (except college-educated men, a rapidly shrinking cohort of the population).

This is central to understanding the “citizenship” of capital. It is widely assumed that capital account liberalization is a given feature of the modern world, but the less fortunate know that capital can be gated anytime, as China, Russia, and others have demonstrated, when nation-states choose to do so. The problem historically has been defection: when any single country imposes a wealth tax, capital simply flees to the next jurisdiction. But as the fiscal nihilism becomes universally felt as global political will converges towards only one choice, a collective bargaining arrangement becomes inevitable, one where the safe havens that have long profited from the prisoner’s dilemma are no longer permitted to opt out.

Upon the Netherland’s recent decision, the EU is already in active discussion about tax coordination frameworks designed specifically to prevent capital flight between member states. In the mid-21st century, the global passport of capital will be revoked and replaced with a Schrödinger visa that is simultaneously valid and invalid, depending on who is watching and enforcing. The local imprisonment of capital will only intensify the demand for “outside money” capable of bypassing the compliance layer entirely. Welcome to the rebirth of the price specie economy, backed by hard money.

Under David Hume’s framework articulated in his 1752 essay “Of the Balance of Trade,” modern investors have long defaulted to thinking of outside money as assets like gold or Bitcoin, something stateless, jurisdictionless, answerable to no sovereign. But now four hundred years later, a new category of outside money is emerging that is fundamentally redefining the notion of comparative advantage itself. It is time to consider a new essay for international relations: “Of the Balance of Intelligence.”

Just as Hume argued that trade surpluses and gold flows determined the relative power of nations, the new determinant of comparative advantage will be the concentration of productive AI infrastructure, specifically who owns the compute, who controls the data, and who sets the rules of the models that everything else runs on. Capital will flow toward intelligence supremacy the way it once flowed toward manufacturing supremacy, and the nations, institutions, and individuals who grasp this earliest will define the new hierarchy of wealth. Which brings me to the third certainty.

Certain Truth #3: AI will destroy the relative value of Labor, and redefine the value of Capital for the intent-based economy

In Das Kapital, Karl Marx described capital as “dead labor which, vampire-like, lives only by sucking living labor, and lives the more, the more labor it sucks.” This infamous quote highlights the socialist view that capital in the form of accumulated labor reflexively exploits itself as it consumes living labor of workers to increase its own value forever.

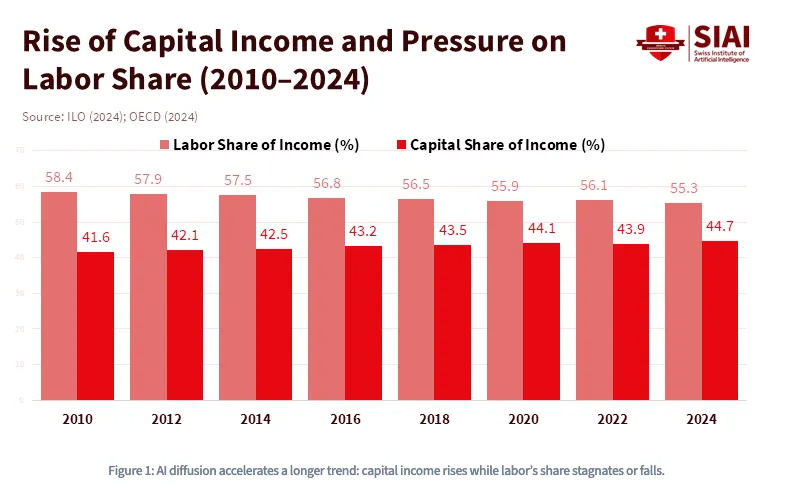

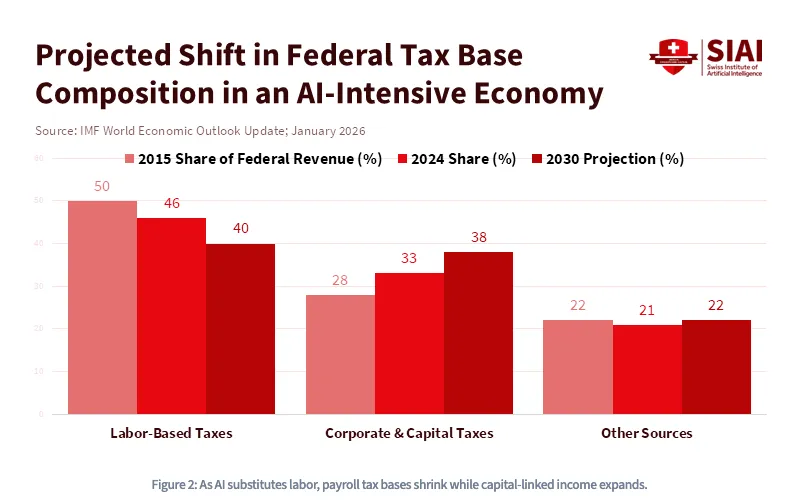

However, Marx makes a crucial mistake in his analysis when he emphasizes that capital is naturally inert on its own and requires the constant consumption of human labor to generate profit. Through the meteoric rise of credit and now artificial intelligence, we are about to enter a new paradigm where “the vampire” is not only fully dynamic, it bypasses even human labor to require mostly the constant consumption of kinetic energy to generate profit. As the graph below illustrates, this trend has been building for over a decade by the the steady rise of capital income relative to labor’s declining share, and AI will drive it past an inflection point of no return.

Since 1980, labor's share of U.S. GDP has declined from roughly 65% to under 55%, and that was before LLMs hit the market. Goldman Sachs estimated in 2023 that generative AI could expose 300 million full-time jobs to automation.

In other words, AI is not only capital intensive—it is labor destructive. The rise of AI will permanently alter the underlying economic principles of a functioning society, reshaping the relationship between capital and labor in ways that cannot be undone. More specifically, as the cost of labor converges with the cost of compute, a new form of capital war will emerge on the global stage, demanding government subsidies and radical industrial and fiscal policy on a scale never before attempted. In this world, capital will be king. Asset ownership will be the only barrier between dignity and the permanent underclass. This is precisely why the IMF projects that in an AI-intensive economy, the federal tax base will shift away from labor income and toward corporate and capital gains taxes.

Yet capital itself will also be redefined, for asset ownership is not limited to financial assets alone anymore. The voracious AI industry feeds on a second ingredient, one that is arguably more valuable and more non-fungible than pure energy itself. That ingredient is data. Specifically, the data footprints you generate every day that provide context for inference and learning. The world is moving toward a paradigm where premium value will be assigned to human thoughts, activities, prompts, tastes, and above all, intents. Your intents will be valuable. When intent thereby becomes capital, it will give rise to a structurally different economic order where asset ownership will look strangely non-custodial, operating outside the rails of KYC/AML financial institutions as we know it. Agent systems are already being provisioned with crypto wallets to autonomously pay for compute, APIs, and data. This is a practical certainty for a world in which value needs to move seamlessly across an autonomous world of agentic systems that favor explicit transaction-based usage, where labor and capital co-exist in a Schrödinger state of superimposition.

Historically, financial assets stayed neatly inside regulatory lanes set by financial watchdogs, like the SEC, CFTC, FINRA, FASB, etc. But as assets evolve into something more ontologically “active” where your data footprint becomes collateral and intent becomes monetizeable outputs (as consumption based pricing models take over via open, API based products that can embed context), AI systems will blur the lines of regulatory perimeters in every direction. The FCC has jurisdiction because your cognitive exhaust is traveling over spectrum. the FTC has jurisdiction because the harvesting of intent is a consumer protection issue. the DoD has jurisdiction because data sovereignty is national security. In other words, the superimposition doesn’t stop at the asset level, but rather it metastasizes upward into the regulatory architecture itself. And when no single authority can draw a clean border around what a “financial asset” actually is anymore, the definition of money (who issues it, who protects it, who can confiscate it) becomes the most contested geopolitical question of the century at the global level.

Welcome to the era of agentic money.

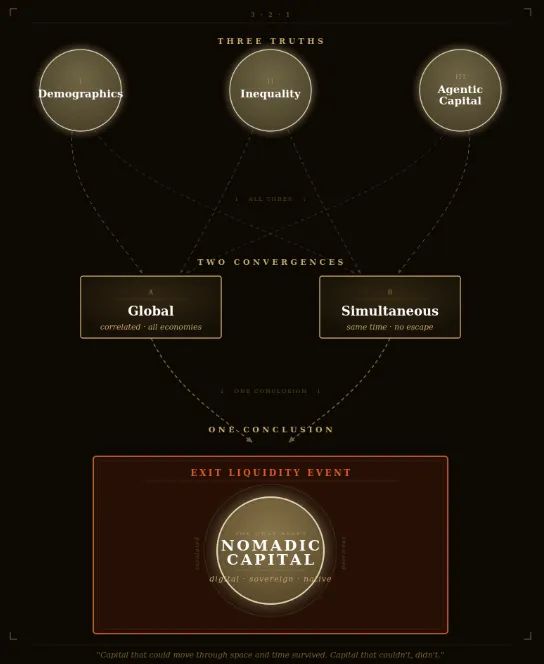

Three Certainties, Two Convergences, One Conclusion

If you have read this far, you are probably feeling a sense of unease—perhaps finding yourself once again adrift in great uncertainty. But remember: the entire purpose of this essay is to find clarity. So let’s reaffirm the most clarifying pact together: all three of these forces—demographic collapse, wealth inequality, and the AI-driven displacement of labor—are going to happen. These are not independent risks to be weighed and hedged in isolation; they are converging simultaneously by definition. The pyramid is collapsing vertically while the floor splits horizontally, and the tectonic pressure beneath both is being amplified by a technological revolution that plays no favorites except one: capital.

Many investors attempt to navigate this uncertainty by offering partial prescriptions to partial problems, a rotation here, a hedge there, a thematic bet on AI infrastructure, a hopium-laced bet on crypto. The most seductive counterargument, and the one most likely to keep conventional investors comfortably sedated, is the techno-optimist escape hatch: that AI-driven productivity growth will expand the pie fast enough to outrun the demographic collapse. It is a compelling view to behold. It is also precisely the kind of reasoning that sounds sophisticated while missing the point entirely.

Productivity gains have never, in recorded history, distributed themselves fast enough or equitably enough to preempt the political and social fractures that inequality produces. The Industrial Revolution didn't prevent labor uprisings; it caused them, even as it created unprecedented aggregate wealth. And crucially, AI is not a neutral productivity multiplier: it is, by its architecture, a capital concentrator. Every dollar of productivity it generates accrues first and most durably to whoever owns the compute, the data, the model. The optimists are not wrong that the pie will grow. They are wrong about who gets to eat it, and that distinction is the entire argument.

Once you zoom out far enough to see the truly irreversible global phenomena for what they are, directional conviction becomes surprisingly available.

-

It is 100% certain that global demographics will deteriorate as major country populations age and contract

-

It is 100% certain that wealth inequality will widen to the point of triggering historic global capital restrictions both across national borders and within them

-

It is 100% certain that AI will structurally favor capital over labor, giving rise to a new form of liminal capital at a scale the global economy has never encountered

And most critically, the key descriptor across all three bullets converge to this: global. Generational demographics, asset allocation, and the cost of capital have never been more correlated in history than they are right now, and that correlation is only tightening. Furthermore, the correlation is tightening not only across space, but also across time as the wealth demographics are irreversibly one-way. This means the convergence, in addition to being global, will also be simultaneous.

Together, this creates what I see as the ultimate collective bargaining problem of the modern century: the Prisoner’s Dilemma of Generational Exit Liquidity. It asks questions like:

-

Will the young voluntarily step up to “own a piece of US capitalism” when it also feels like the government directive is to “hold your parents bag?”

-

Will the wealthy billionaires voluntarily choose to get heavily taxed when their friends flee towards “tax-efficient” planning?

-

Will AI companies voluntarily slow down development while their mercenary competitors continue to distort the cost of capital, with or without you?

The Nash equilibrium will emerge as all players defect as the rational dominant strategy, regardless of what anyone else does for the price of inaction is too great to bear. So when the moment comes, everyone will rationally seek exit liquidity at the same time.

This Faustian bargain of liquidity must be understood not as a mere possibility, not as a tail risk to be modeled and hedged against, but as the single most predictable mass coordination event in the history of human capital markets. Some will argue that in a deflationary world you want bonds, nominally interest-bearing instruments, or AI equities riding the exponential curve. Perhaps. But my north star is simpler and more structural: you want to own things that will not let you become someone else’s exit liquidity. In that framework, the last things you want to own, in order, are housing, bonds, and U.S. equities. These are duration manipulation instruments engineered, whether intentionally or not, as the greatest generational wealth heist in history.

What you want to own instead should satisfy the three conditions simultaneously, in reverse.

-

First, what is demographically least-owned today with the greatest potential to be owned more tomorrow

-

Second, what is most likely to serve as a jurisdictionless safe haven when capital mobility becomes severely taxed, restricted, or seized entirely

-

Third, what most closely resembles the form of capital that an autonomous, agentic world will actually use seamlessly without intermediaries to perform the productivity functions that will replace the cost of human labor

When the Ottoman Empire breached the walls of Constantinople in the fifteenth century, the Byzantine merchant class lost everything denominated in imperial trust: land, titles, treasury bonds. You name it, everything was gone. But the young ambitious scholars and the young enterprising traders who had moved their portable wealth, such as manuscripts, gold, knowledge westward into Florence, ultimately ignited what would be later known as the Renaissance.

Among this group was a young Byzantine scholar named Johannes Bessarion. Born in 1403 in Trebizond on the Black Sea, he fled Constantinople with crates of irreplaceable Greek manuscripts carrying essentially the entire intellectual inheritance of the ancient world. He was the man who gave the West the most books and manuscripts in the 15th century, and thereby created one of the earliest “information technologies”: Biblioteca Marciana, the first open-source repository (ie. public library) in Latin European history. That collection, sitting in Venice, became the direct source material for Aldus Manutius, who used it to print Aristotle’s complete works and dozens of Greek classics, igniting the printing press revolution that would cascade into the Reformation, the Scientific Revolution, and the Enlightenment. This portable, sovereign, jurisdictionless capital Bessarion carried across a border compounded into five centuries of Western civilization.

Capital that could move through space and time, survived. Capital that couldn’t, died.

This brings us to our final conclusion, the one radical decision worth considering as you stand before the trap of many conventional options:

What you want to own is nomadic capital. Capital that is portable across the demographics of time, political borders, and AI-native ecosystems. Capital that can bypass the monetary Strait of Hormuz. Nomadic in the 21st century means digital. The specific instruments may vary as reasonably high agency people will each arrive at different conclusions; the

Radical Portfolio Theory

provides one such viable framework across owning 60% compliance assets and 40% resistance assets. But if you follow the three conditions with disciplined deliberation—to own what the young will eventually need, to own what no government can easily reach, to own what the autonomous economy will actually transact in—the destination becomes less a prediction and more an outcome. The uncertainty becomes the inevitability.

There is, after all, only one radical asset in history that was designed from its first line of code to satisfy all three simultaneously. For the high-agency minded, this is the easy part.

The rest is just timing.

Disclaimer:

-

This article is reprinted from [dgt10011]. All copyrights belong to the original author [dgt10011]. If there are objections to this reprint, please contact the Gate Learn team, and they will handle it promptly.

-

Liability Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute any investment advice.

-

Translations of the article into other languages are done by the Gate Learn team. Unless mentioned, copying, distributing, or plagiarizing the translated articles is prohibited.