From models, computing power, to cloud and security, OpenClaw may influence the benefit logic of U.S. stocks. This article reviews investment opportunities along the industry chain—from chips, cloud, to security companies—in the Agent era.

(Background: Even crayfish experts face setbacks! OpenClaw leaked top secrets of its own servers due to a syntax error.)

(Additional context: Don’t blindly follow OpenClaw. Crayfish AI is powerful, but not necessarily suitable for you.)

Table of Contents

Toggle

-

- What is OpenClaw? Why does it impact U.S. stocks?

-

- Token Killer: The Super Flywheel of Large Model Service Providers

-

- Reasoning Never Enough: New Narratives for Chip Companies

-

- The True Carrier for Agent Scaling: Cloud Computing

-

- Enterprise Agent Logic to Be Verified, Benefiting Native AI Companies

-

- Hidden Benefits for Security Companies

-

- Conclusion: Short-term Sentiment, Mid-term Reasoning, Long-term Ecosystem

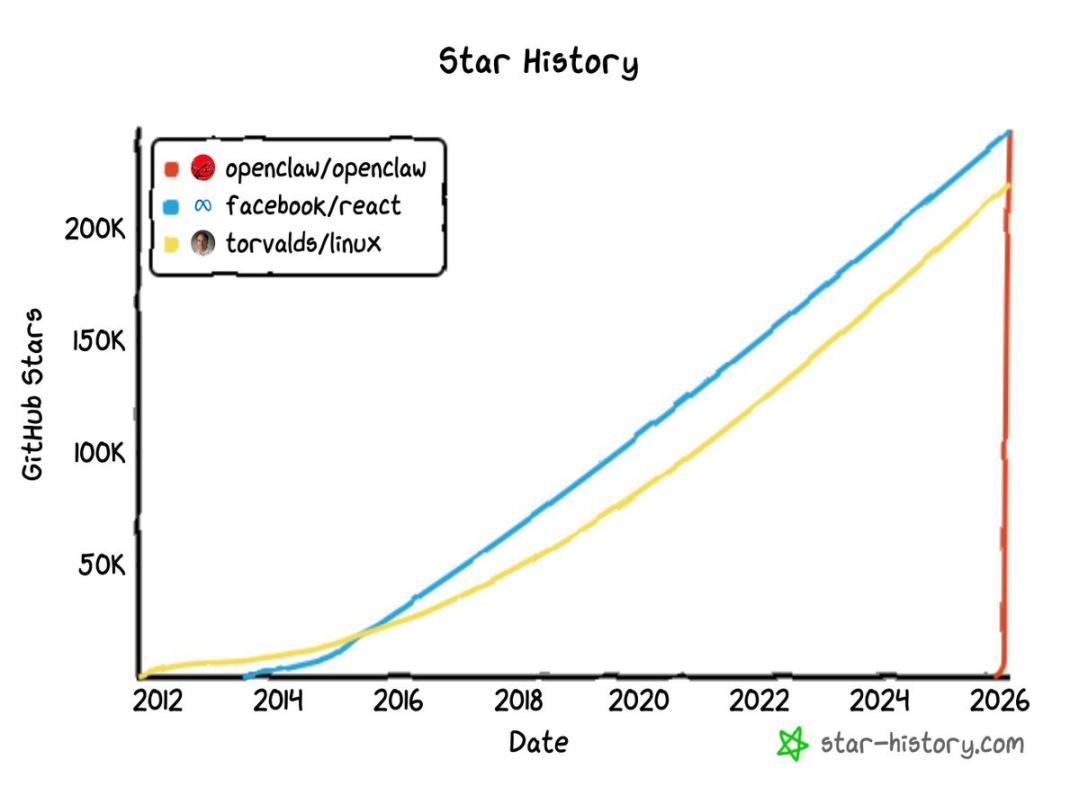

In November 2025, Austrian independent developer Peter Steinberger quietly submitted a project—Clawdbot (later renamed OpenClaw)—on GitHub.

At the time, no one paid attention. Everything spiraled out of control by late January 2026.

Between January 29 and 30, the project gained tens of thousands of GitHub stars in a very short time, quickly surpassing 100,000. By March 3, this number had exploded to nearly 250,000, topping the star rankings and surpassing Linux. For reference, star counts for popular open-source projects like React (one of the most popular front-end frameworks globally) and Linux (the core OS powering servers) usually take over a decade to reach 200,000 stars; OpenClaw’s curve was almost vertical.

Initially named Clawdbot as a pun on Claude, Anthropic sent a legal letter on January 27 demanding a name change. The project then briefly became Moltbot before finally settling on OpenClaw. Yet, name changes did not slow its spread—in fact, they generated more buzz. On February 16, Sam Altman announced Steinberger joined OpenAI, and OpenClaw would be transferred to an independent open-source foundation supported by OpenAI.

From an independent developer project to a strategic pawn of tech giants, this little crayfish took less than three months.

OpenClaw’s popularity in the tech community is well known. But where is this fire now burning? This article attempts to analyze, from a capital markets perspective, the industry chain behind OpenClaw’s explosion and the U.S. stocks that may be revalued.

1. What is OpenClaw? Why does it impact U.S. stocks?

First, the essence. OpenClaw is not just another chatbot; it’s an open-source AI Agent framework.

What’s the difference? Chatbots receive your questions and reply with text. OpenClaw receives your commands and then acts—browses, runs code, calls APIs, manages files, connects to over 12 messaging platforms.

The operational modes of the two can be summarized in a table:

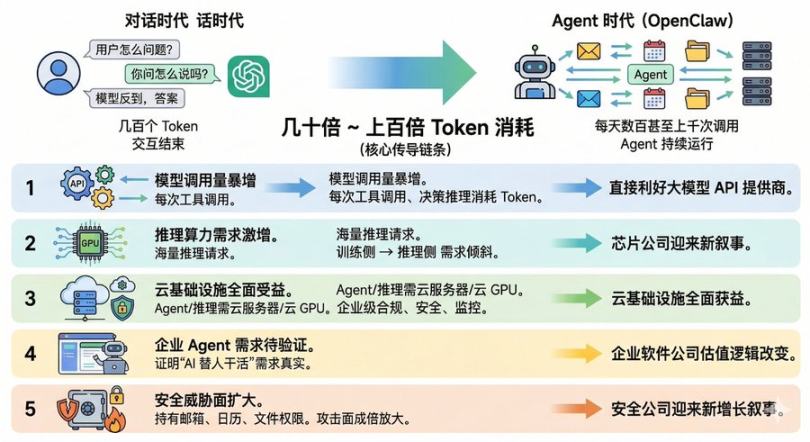

In simple terms, it has evolved from a chatbot into a true digital employee, signaling a fundamental shift in AI business paradigms. In the dialogue era, users ask a large model a question, get an answer, consuming a few hundred tokens, and interaction ends. But in the Agent era, a single OpenClaw may make hundreds or even thousands of calls to the model daily. The token consumption per user can be dozens or hundreds of times higher than traditional chat users.

This amplification factor is the core transmission chain through which OpenClaw influences U.S. stocks:

- First layer: Explosive increase in model calls. Each tool call and reasoning decision by an Agent consumes tokens, directly benefiting large model API providers.

- Second layer: Surge in inference computing power demand. Massive Agent calls mean huge inference requests, shifting GPU demand from “training” to “inference,” creating a new narrative for chip companies.

- Third layer: Full benefit to cloud infrastructure. Agents need cloud servers to run, models require cloud GPUs for inference, and enterprise-level Agents demand compliant, secure, and monitorable cloud infrastructure.

- Fourth layer: Enterprise Agent demand to be validated. OpenClaw’s open-source approach proves the real need for AI to “do work for humans,” and companies commercializing Agent capabilities may see valuation shifts.

- Fifth layer: Security threat surface expands. When Agents hold email, calendar, and file permissions long-term, attack surfaces multiply, creating new growth narratives for security firms.

Below, we analyze each link in this chain to identify benefiting U.S. stocks.

2. Token Killer: The Super Flywheel of Large Model Service Providers

If Agents become the mainstream interaction paradigm for AI, API revenue for large model providers will grow exponentially.

Currently, the two biggest Agent model providers, OpenAI and Anthropic, are not publicly listed. Therefore, the most direct listed proxies in the capital markets are MSFT and GOOGL.

First, Microsoft, as OpenAI’s largest external shareholder, benefits from every API call to GPT-4 or GPT-3 via Azure OpenAI Service—contributing revenue to Microsoft’s cloud business. Steinberger’s joining OpenAI and transferring the project to an OpenAI-supported foundation suggest a tighter integration of OpenClaw’s ecosystem with OpenAI models. If future default model recommendations in OpenClaw favor OpenAI first, Microsoft effectively gains an entry point with 240,000 GitHub stars—an influential developer gateway.

Meanwhile, Alphabet (GOOGL/GOOG) benefits in another dimension. Google’s Gemini series is one of the main models supported by OpenClaw, especially Gemini 2.0 Flash, which offers highly competitive inference cost-performance. More critically, among top model vendors, Alphabet is one of the few that can directly invest in AI models via secondary markets.

It’s also worth noting that the market currently seems underpricing the API consumption driven by Agents. GOOGL has not shown significant stock movement since February due to OpenClaw, and MSFT has experienced valuation correction. The market’s expectations still rely on “chatbot” logic for model valuation, not the ongoing Agent economy.

3. Reasoning Never Enough: New Narratives for Chip Companies

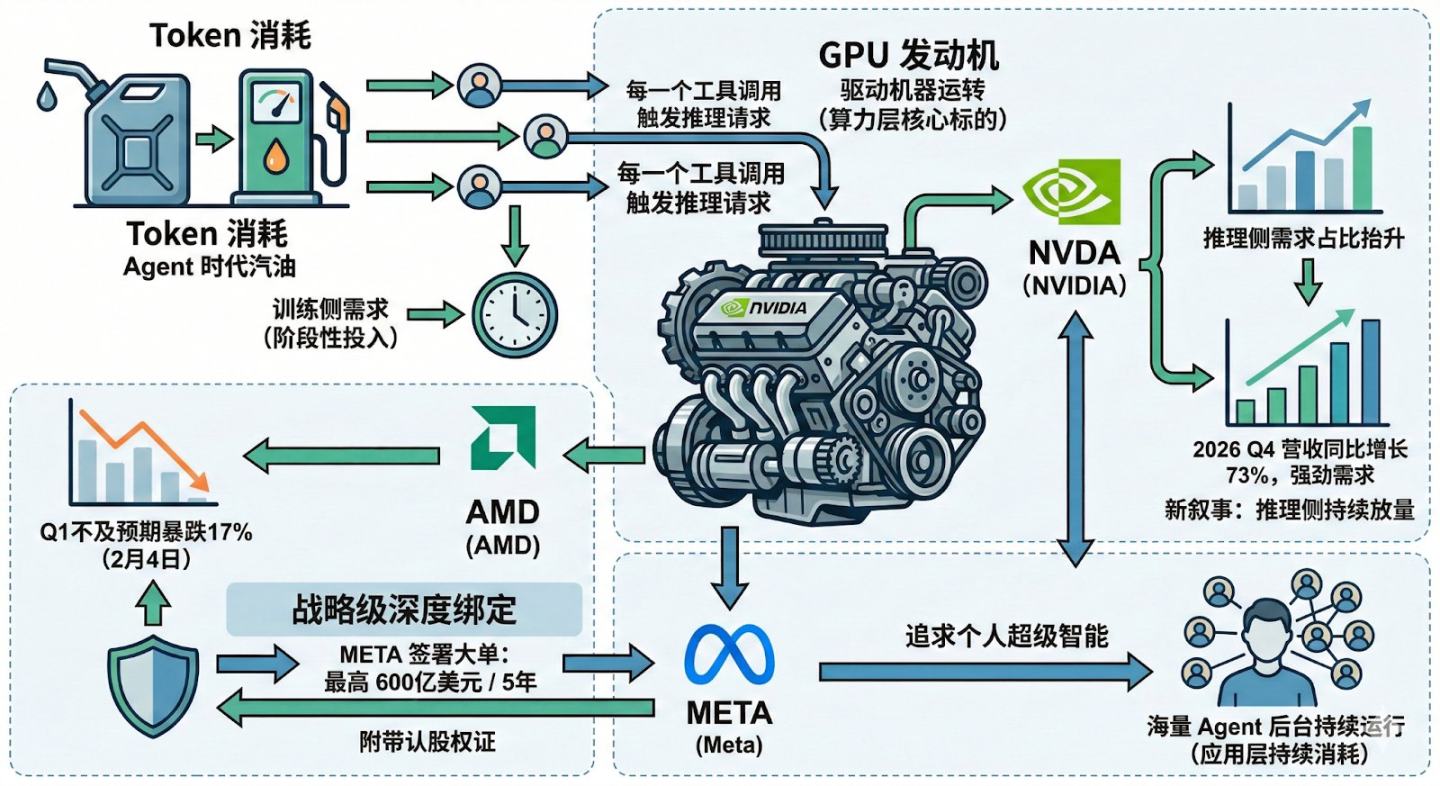

If token consumption is the fuel of the Agent era, GPUs are the engines driving this machine. The most immediate beneficiaries are NVIDIA and AMD.

Over the past three years, chip valuations have been mainly based on training-side demand, with companies competing to buy GPUs for training ever larger foundational models. But training is a phase-based investment, while inference is a continuous consumption—each tool call by an Agent triggers new inference requests. As Agents move from labs to millions of users, inference demand could significantly increase.

This explains NVIDIA’s new narrative. If the training-side growth slows, what can sustain GPU demand? The answer is sustained inference volume. NVIDIA’s latest earnings show a 73% YoY revenue increase in Q4 2026, with strong demand, supported by the rise of the Agent paradigm, providing a more sustainable underlying logic.

Similarly, AMD’s stock plummeted 17% on February 4 after missing Q1 revenue expectations. But just 20 days later, Meta announced a five-year, $60 billion AI chip supply deal with AMD, including up to 160 million warrants—more like a strategic deep binding.

Why does Meta need so much inference power? To pursue “personal superintelligence,” which requires massive backend Agent operation. OpenClaw confirms not just a product direction but the entire logic that Agent demand needs vast computing power.

Thus, inference-driven demand growth first propagates to the compute layer, benefiting NVIDIA and AMD. Among companies continuously consuming compute, Meta could also become a key demand driver.

4. The True Carrier for Agent Scaling: Cloud Computing

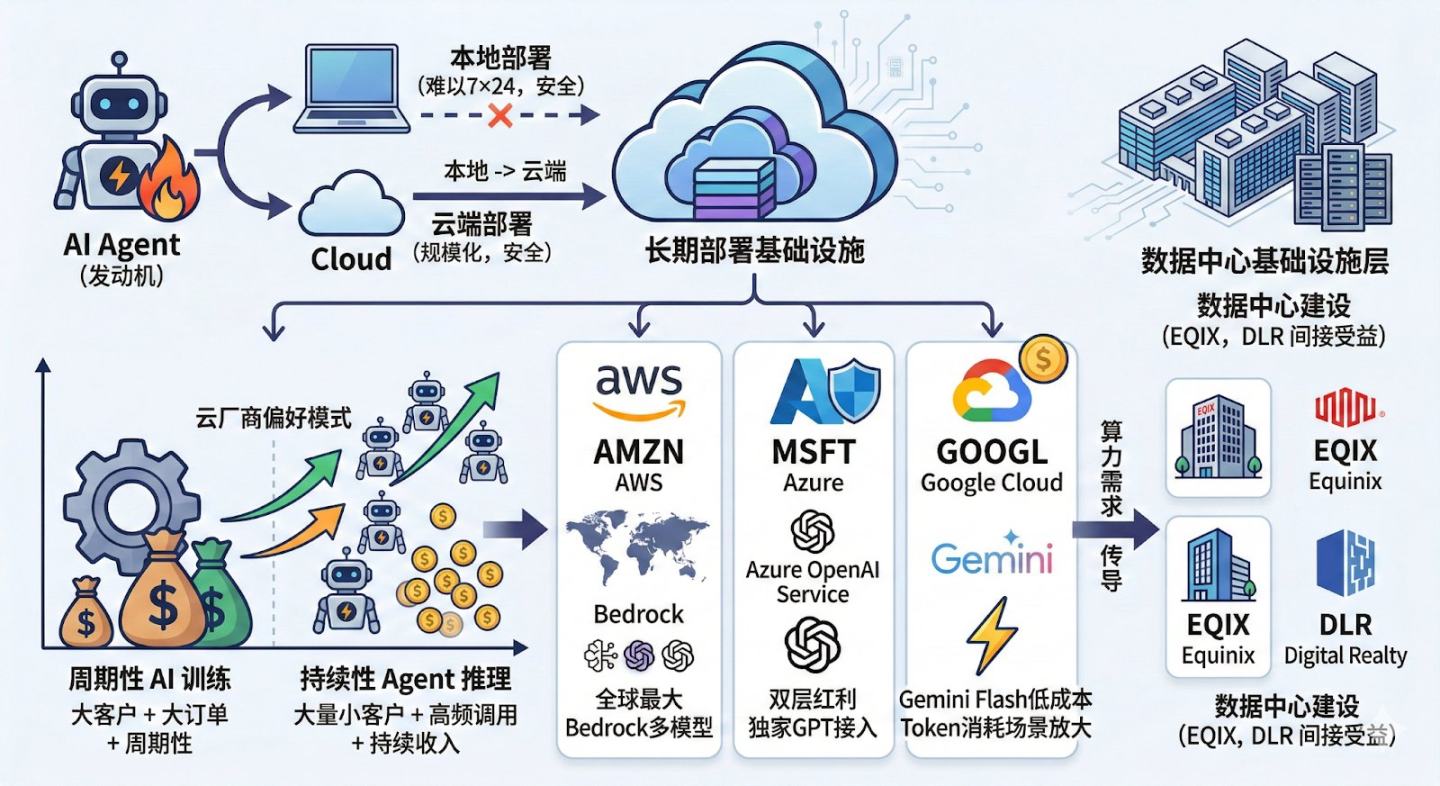

GPU is the engine, but cloud platforms are the infrastructure for long-term Agent operation. From a capital markets perspective, the core stocks are the three major cloud providers: AMZN, MSFT, GOOGL. In upstream data center infrastructure, EQIX and DLR may also benefit indirectly.

Although OpenClaw advocates local deployment, in reality, due to security and permission issues, most users won’t run AI Agents 24/7 on personal laptops. Both individuals and enterprises are likely to deploy on the cloud. Alibaba Cloud and Tencent Cloud already offer one-click deployment services in China, confirming demand’s reality.

An often overlooked detail: the value of cloud for Agents is not just compute, but long-tail inference traffic. AI training orders are “big clients + large orders + cyclical,” while inference is “many small clients + high-frequency calls + recurring revenue”—a business model cloud providers prefer.

Globally, the three cloud giants each have unique advantages. AWS, as the largest cloud platform, supports multiple model APIs via Bedrock and is a common deployment environment for developers. Azure benefits from both model API and cloud infrastructure layers, with its exclusive GPT access via Azure OpenAI Service further amplifying Agent scenarios. Google Cloud’s edge lies in cost structure—models like Gemini Flash have significantly lower inference prices, which will be quickly advantageous in long-running Agent scenarios consuming tokens.

Another logical point: if Agent scaling drives cloud demand, it will eventually lead to data center expansion, benefiting companies like EQIX and DLR.

5. Enterprise Agent Logic to Be Verified, Benefiting Native AI Companies

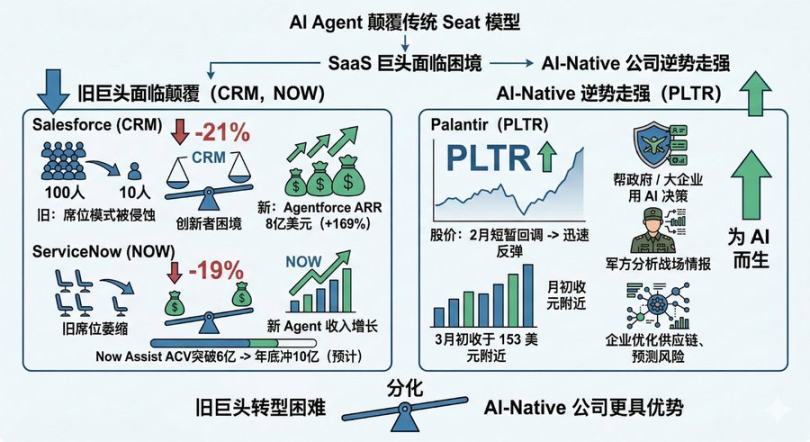

The explosive popularity of OpenClaw confirms a trend: people are willing to let AI do work for them, not just chat. But for traditional enterprise software, this is seen as the beginning of the “SaaSpocalypse.”

Early 2026, SaaS giants faced pressure: Salesforce down 21%, ServiceNow down 19%. The root cause is a structural game between Agents and software. Previously, systems needed software interfaces; now, Agents can call systems directly, diminishing the presence of traditional software. This fundamental change raises two issues:

First, AI impact isn’t limited to “per user fee” models but affects the entire software value chain. For example, Adobe’s stock fell from $699.54 to $264.04—a 62% drop; education software Chegg nearly went to zero, from $115.21 to $0.44; tax and finance giant Intuit dropped 16% in one week in January 2026. The market worries not just about revenue model disruption but about generative AI automating core workflows, reducing dependence on traditional software, and permanently compressing SaaS revenue potential.

Second, stronger Agents threaten traditional business models. Take ServiceNow: Microsoft’s “Agent 365” bundling strategy erodes its pricing power and slows new customer acquisition. A simple thought experiment: if one AI Agent can do the work of 100 employees, is there still a need to buy 100 software seats? OpenClaw’s breakout accelerates this logic.

Major players are not passive. Salesforce’s AgentForce has reached $800 million ARR, up 169%; ServiceNow’s Now Assist exceeds $600 million in annual contract value, aiming for $1 billion by year-end. But the classic innovator’s dilemma applies: new Agent revenues grow, existing seat revenues shrink, and the outcome is uncertain. For CRM and NOW, the core question is whether Agent’s incremental growth can offset seat-based revenue declines. The market has spoken with its feet.

Meanwhile, Palantir tells a different story. Focused on critical decision-making for governments and large enterprises—analyzing battlefield intelligence, optimizing supply chains, predicting risks—Palantir deploys AI in the most complex, sensitive scenarios. After a brief correction in February, PLTR rebounded quickly, stabilizing near $153 in early March.

While SaaS was hit hard by the “SaaS end-times,” Palantir’s resilience suggests that winners in the Agent era may not be the fastest to transform old giants but those born for AI from the start.

6. Hidden Benefits for Security Companies

This is currently the most underestimated thread in the market.

Imagine you set up OpenClaw with access to email, calendar, Slack, Google Drive, GitHub—these keys are needed for it to work. But what if the Agent gets compromised? The OpenClaw community has discussed security risks like credential leaks, privilege abuse, and data theft.

This is why security firms are positioning early. CrowdStrike (CRWD) and Palo Alto Networks (PANW) are the top players.

CrowdStrike is considered a leader in endpoint security. Its Falcon platform manages endpoints, identities, and threat intelligence via cloud-native architecture, with high penetration in large enterprises worldwide. Recently, the company has integrated AI into security operations, e.g., Charlotte AI, which automates threat detection and response.

Palo Alto Networks is a global cybersecurity leader. Starting from next-generation firewalls, it expanded into cloud security, identity security, and automated security operations. In 2025, it acquired CyberArk for $25 billion, focusing on privileged identity security.

While security revenues from OpenClaw’s recent explosion are not yet large, this indicates that security companies could be the biggest “expectation gap” beneficiaries in the Agent narrative. Security spending remains a must.

7. Conclusion: Short-term Sentiment, Mid-term Reasoning, Long-term Ecosystem

Returning to the initial question: which U.S. stocks are truly impacted by OpenClaw? We can analyze along different timelines.

Currently (last month), the direct impact on individual stocks is limited. GOOGL and MSFT have not shown abnormal volatility driven by the Agent narrative since February. The only clear event was AMD’s massive order, which caused a single-day surge. Overall, the AI sector may be undergoing valuation adjustments; OpenClaw’s popularity has not yet translated into immediate stock catalysts.

In the short term (3 months), the market may continue to digest valuation corrections, but the cognitive impact from OpenClaw could reshape investor expectations about the Agent sector. This change in perception may not immediately reflect in stock prices but could alter analyst models.

In the mid-term (6-12 months), key catalysts depend on whether inference demand driven by Agents can be validated in earnings reports. If OpenClaw and subsequent versions like Kimi Claw, MaxClaw, and enterprise Agent solutions show observable growth in API calls and cloud resource consumption, NVIDIA, AMD, and the cloud giants’ inference narratives could be confirmed.

In the long-term (1-3 years), the true winners will be those companies that secure positions in the Agent ecosystem—such as CrowdStrike and Palo Alto Networks—especially in establishing standards for Agent security.

We must also recognize that OpenClaw is not the ultimate product; it has security flaws, high token costs, and uncertain business models. But it has achieved one key thing: demonstrating the world’s potential for AI Agents. This is no longer just product iteration; it’s a profound paradigm shift.

Once a paradigm shift occurs, it won’t stop. We can only prepare ourselves fully for that day.