South Korea’s former augmented reality company Bitmax announced on March 9th a 1-for-4 share consolidation to eliminate accumulated losses. The following day, the stock price dropped more than 10%, trading near $0.63 (909 KRW), approximately 88% below its 52-week high. In comparison, Strategy, which employed the same Bitcoin treasury strategy, declined about 70% during the same period, while Bitcoin itself only fell 12%.

Bitmax’s Structural Dilemma: Off-Exchange Related Party Transactions and Regulatory Concerns

Currently, Bitmax holds 551 Bitcoins: 539 acquired through 13 OTC transactions conducted by the chairman at a total cost of approximately $55 million, with the remaining obtained via Ethereum exchanges. The first transaction’s premium was as high as 17.7%. According to local media reports, the total amount paid for these 13 transactions was about $6 million higher than the prevailing exchange rate at the time.

South Korean regulators plan to open direct trading for listed companies on exchanges by mid-2025. However, nearly 60% of Bitmax’s Bitcoin purchases continue to be made through off-exchange transactions with the chairman after this date, raising market concerns over reliance on related-party transactions.

Key Financial Deterioration Indicators: Threefold Debt Growth in Nine Months

Bitmax’s Q3 2025 financial report reveals rapid deterioration of its balance sheet:

- Total Debt: surged from $4.4 million to $74 million in nine months, almost entirely from convertible bonds issued to purchase Bitcoin.

- Debt-to-Equity Ratio: jumped from 18% to 73%.

- Consolidated Net Loss (first three quarters): $52 million, with $43 million from valuation losses on convertible bond derivatives.

- Original AR Business: cash flow is minimal; R&D expenses were cut by two-thirds in the first half of 2025.

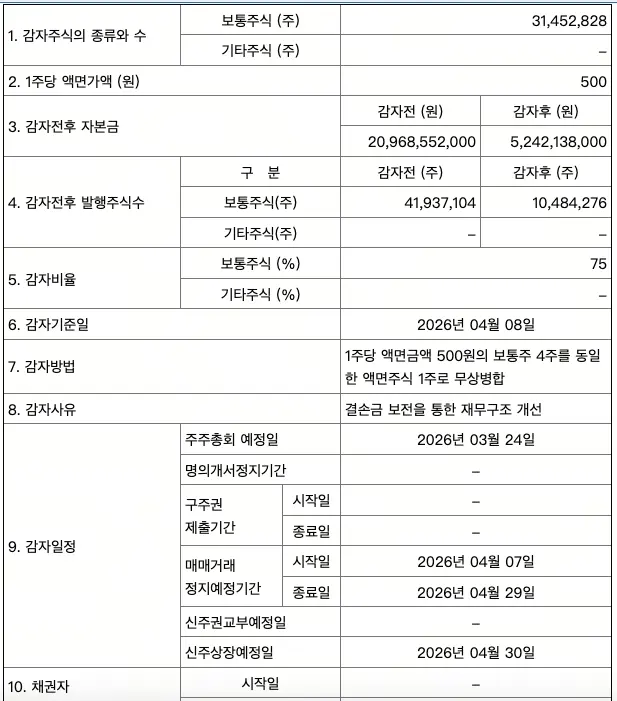

Following the capital reduction, the company’s paid-in capital decreased from $14.5 million to $3.6 million, and outstanding shares from 41.9 million to 10.5 million. In February 2026, management disclosed that in two of the past three fiscal years, pre-tax operating losses exceeded 50% of shareholders’ equity.

Systemic Failures of Korea’s Strategy: The Shared Cost for Four KOSDAQ Companies

Bitmax’s case is not isolated. At least four companies on KOSDAQ—Bitmax, Parataxis Korea, Bitplanet, and Apton—adopted nearly identical strategies in 2025: changing controlling shareholders, renaming, issuing additional shares for fundraising, and purchasing Bitcoin. In February 2026, these four companies’ stock prices declined an average of 29% in that month alone.

Parataxis Korea holds over 200 Bitcoins and carries about $10 million in USDT-backed loans, adding potential risks of margin calls amid existing dilution pressures.

The Strategy model works because it holds 640,000 Bitcoins, is part of the Nasdaq 100 index, can raise hundreds of billions of dollars at once, and benefits from scale, capital market access, and institutional credibility. These small Korean companies lack such advantages and, in the face of falling Bitcoin prices, have little buffer.

Frequently Asked Questions

Why did Korea’s Bitmax Bitcoin treasury strategy fail?

Bitmax lacks three critical conditions that support the Strategy model: large scale, strong capital market fundraising ability, and institutional trust. Additionally, operating at a loss, the company relied on convertible bonds to finance Bitcoin purchases through related-party OTC premiums, leaving it vulnerable to Bitcoin price declines.

Which companies on KOSDAQ have adopted similar Bitcoin strategies?

At least four KOSDAQ-listed companies—Bitmax, Parataxis Korea, Bitplanet, and Apton—used similar approaches in 2025: changing shareholders, renaming, issuing additional shares, and buying Bitcoin. Their stock prices in February 2026 fell an average of 29%, reflecting systemic failure due to lack of scale support.

What does the 1-for-4 reverse split mean for shareholders?

A 1-for-4 reverse split consolidates every four shares into one, reducing the number of outstanding shares from 41.9 million to 10.5 million, and decreasing paid-in capital from $14.5 million to $3.6 million. The purpose is to eliminate accumulated losses and improve financial appearance, but it does not address underlying debt levels or cash flow issues, and does not materially change individual shareholders’ ownership proportions.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.