Author: Kyle Soska, Chief Investment Officer of Ramiel Capital

Translation: Felix, PANews

The crypto market has been in a risk-averse state for several months. Kyle Soska, Chief Investment Officer of Ramiel Capital, has been carefully analyzing various market data to look for signs of a potential market turnaround. This article explores the market structure of perpetual contracts and, combined with data from Ethena’s Transparency Dashboard, analyzes market risk appetite.

For a long time, the crypto market has been characterized by high asset volatility and widespread use of high leverage by traders. Perpetual contracts have become the most traded product in the crypto space, with trading volumes 5 to 20 times that of the spot market. As the central leverage product for retail traders, it is logical to gauge crypto risk appetite through perpetual contracts.

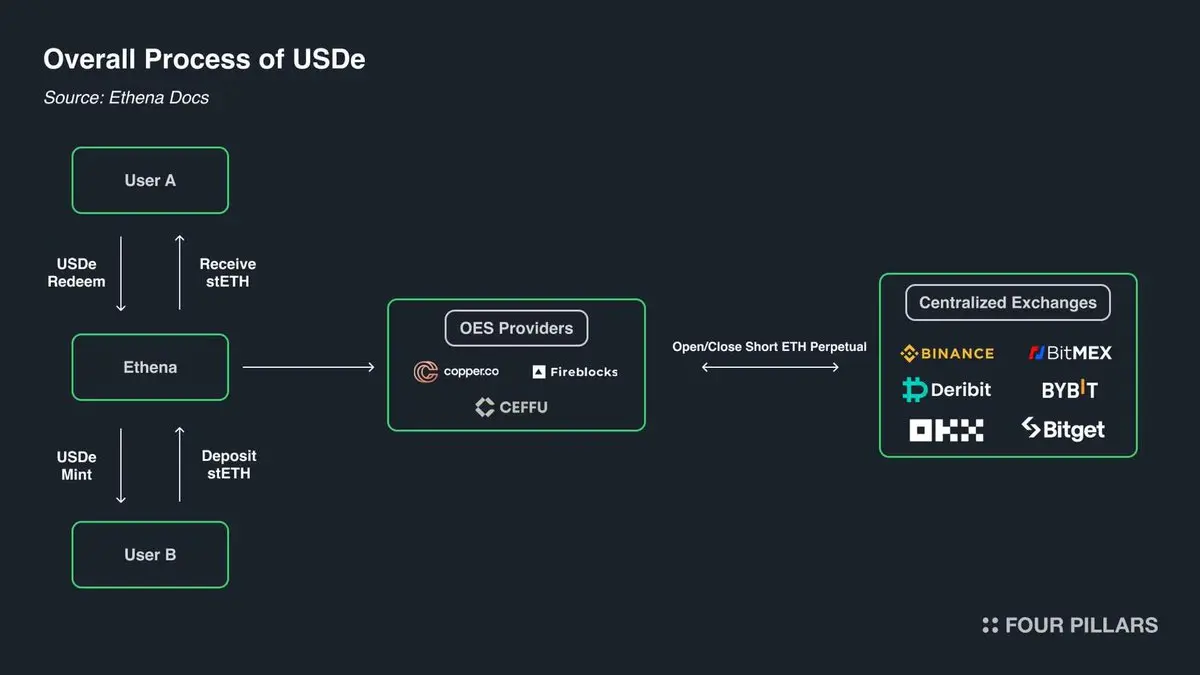

In particular, Ethena provides a unique window into the crypto derivatives market. As shown below, Ethena has implemented “crypto arbitrage trading.” The strategy is simple: when crypto traders go long, Ethena acts as the counterparty to short. Ethena then ensures it holds assets equal in amount to its short positions.

In a sense, Ethena offers “leverage as a service.” Traders seek to profit from rising cryptocurrencies but lack capital, while Ethena has capital but limited risk capacity. Therefore, traders borrow funds from Ethena using perpetual contracts at a cost of “basis + funding rate.”

Source: ethena.fi

According to the structure of perpetual contracts, each long position corresponds to a short position at a 1:1 ratio. Each open contract in a perpetual contract represents an agreement between two parties. The exchange’s role is to facilitate matching these contracts, ensuring that each contract always has sufficient funds with both long and short holders. The table below shows the four possible outcomes of exchange matching.

Perpetual Contract Matching Matrix

Every trade involves a buyer and a seller. When both the buyer and seller are long or both are short, the exchange simply transfers ownership of the contract from one party to another. This transfer does not create or destroy any contracts. When the buyer is long and the seller is short, a new contract must be created, with the buyer holding a long position and the seller a short position, increasing open interest by 1. Conversely, if the seller closes their long and the buyer closes their short, the exchange can directly dissociate the buyer and seller from the contract and delete the newly released contract, decreasing open interest by 1.

So, in a typical market, who actually owns these contracts? I believe they mainly fall into four categories:

-

(Long) directional longs

-

(Short) directional shorts / hedgers

-

(Short) basis traders (Ethena and others)

-

(Mixed) cross-platform perpetual arbitrageurs

Directional longs seek exposure. They pursue risk, with their risk appetite depending on their preferences.

Directional shorts include various participants, such as those seeking downside exposure or those hedging holdings for tax efficiency. Venture capital firms (VCs) and company employees paid in tokens often hedge their unlocking tokens at current prices. For altcoins, many markets are too illiquid for effective direct hedging or lack hedging tools altogether. In such cases, firms like Cumberland, Wintermute, FalconX, Flowdesk, Amber, and others can create dynamically managed synthetic positions, using short positions in highly liquid assets like Bitcoin and Ethereum to hedge exposure in low-liquidity markets like Monad. This also includes projects like Neutrl, which treat such hedging as a yield strategy.

Basis traders are speculative short-sellers. They are not interested in directional exposure but actively fill excess demand for longs during market imbalances. In most market environments, long demand exceeds short demand, and their role is to fill this gap. Their position adjustment capacity is usually very flexible.

Cross-platform perpetual arbitrageurs hold both long and short perpetual positions. Their role is to connect different perpetual instruments and correct small price discrepancies within trading fee ranges. Their longs are always fully matched with their shorts at any given time.

By construction, each perpetual contract is 1:1 and matched long to short, so:

Directional Long + Arbitrage Long = Directional Short + Basis Short + Arbitrage Short

Additionally, the structure of perpetual arbitrage shows:

Arbitrage Long = Arbitrage Short

Eliminating this from the first equation yields:

Directional Long = Directional Short + Basis Short

Ethena provides an aggregated proxy indicator for all basis short positions, helping to deepen understanding of the differences between directional longs and shorts.

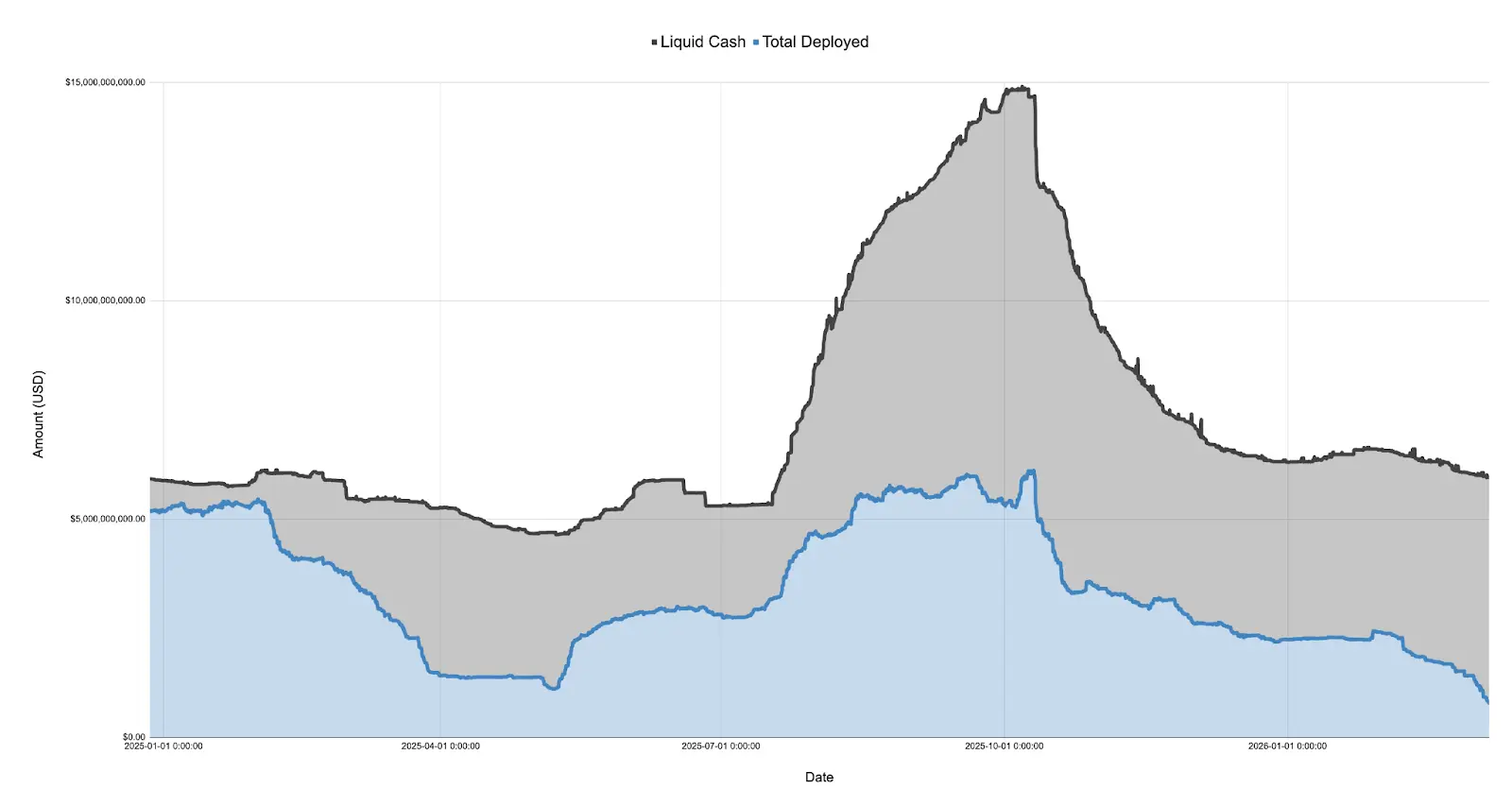

The chart below shows Ethena’s self-reported balance sheet, divided into cash and deployed capital (from December 27, 2024, to March 7, 2026):

In 2025, following the launch of the $TRUMP token in January, market sentiment sharply shifted towards risk aversion, declining through the tariff negotiations in April and culminating in the “Liberation Day.” During this period, Ethena’s deployed capital plummeted from over $5 billion to just $1.108 billion, a drop of over 75%.

It’s important to note that Ethena’s deployed capital is an indicator of excess long demand in the market. While Ethena is not the only entity executing such trades, its large scale (sometimes accounting for about 25% of Binance and Bybit) means that as long as they have surplus cash, they should expand their ledger to meet any unmet long demand. This suggests that, although total long exposure demand may not have decreased by 75% in April 2025, the excess demand unfilled by directional shorts indeed declined.

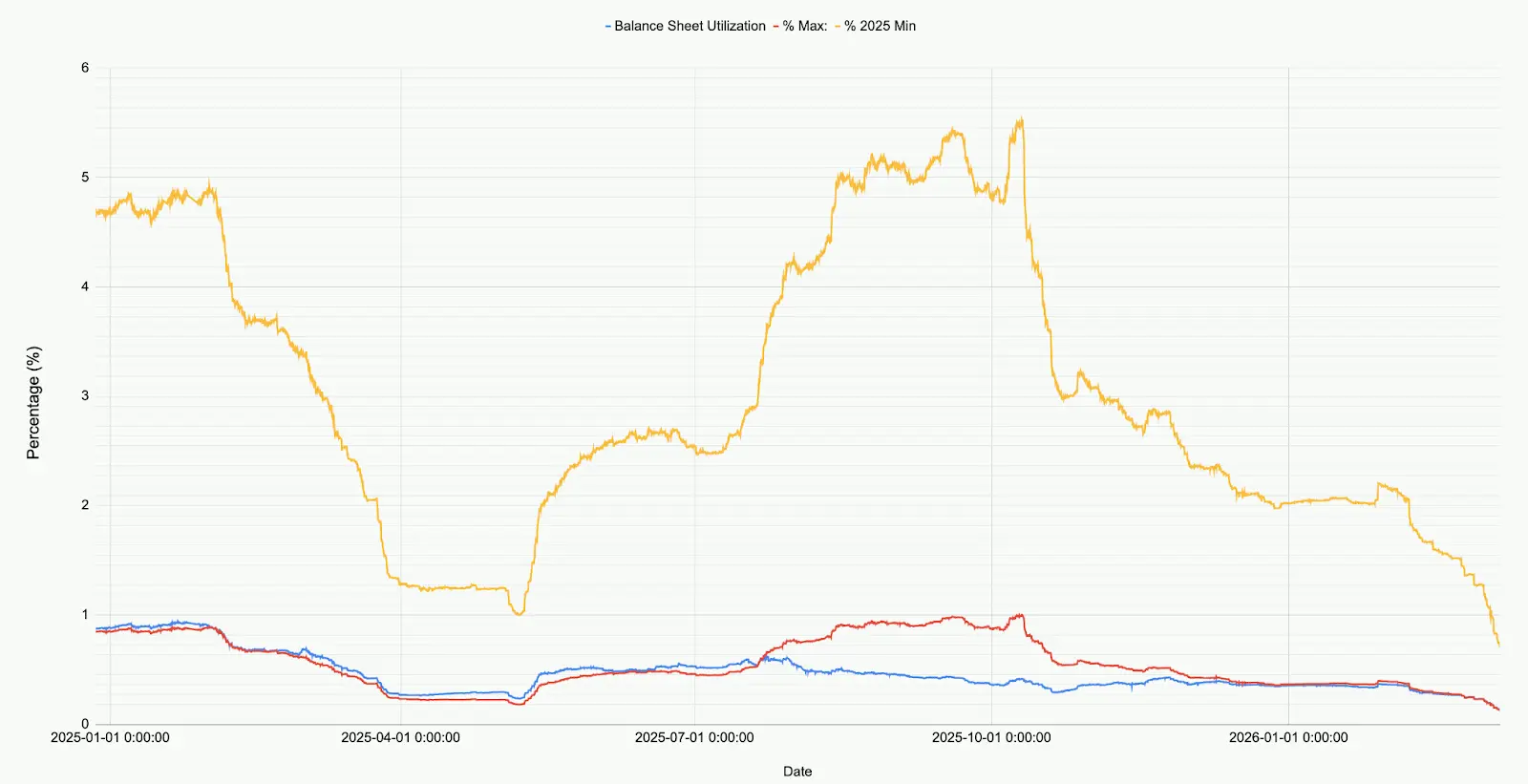

The chart below shows Ethena’s asset deployment relative to its total size, at its 2025 lows and highs.

Looking at today’s market, Ethena’s deployed funds across all markets (BTC, ETH, SOL, BNB, XRP, HYPE) total only $790 million (791,241,545.6 USD). This is 71% of the lowest level in 2025 and only 12.9% of the peak before October 10. This figure does not imply a negative view of Ethena but reflects current market conditions: net long demand is at a historic low.

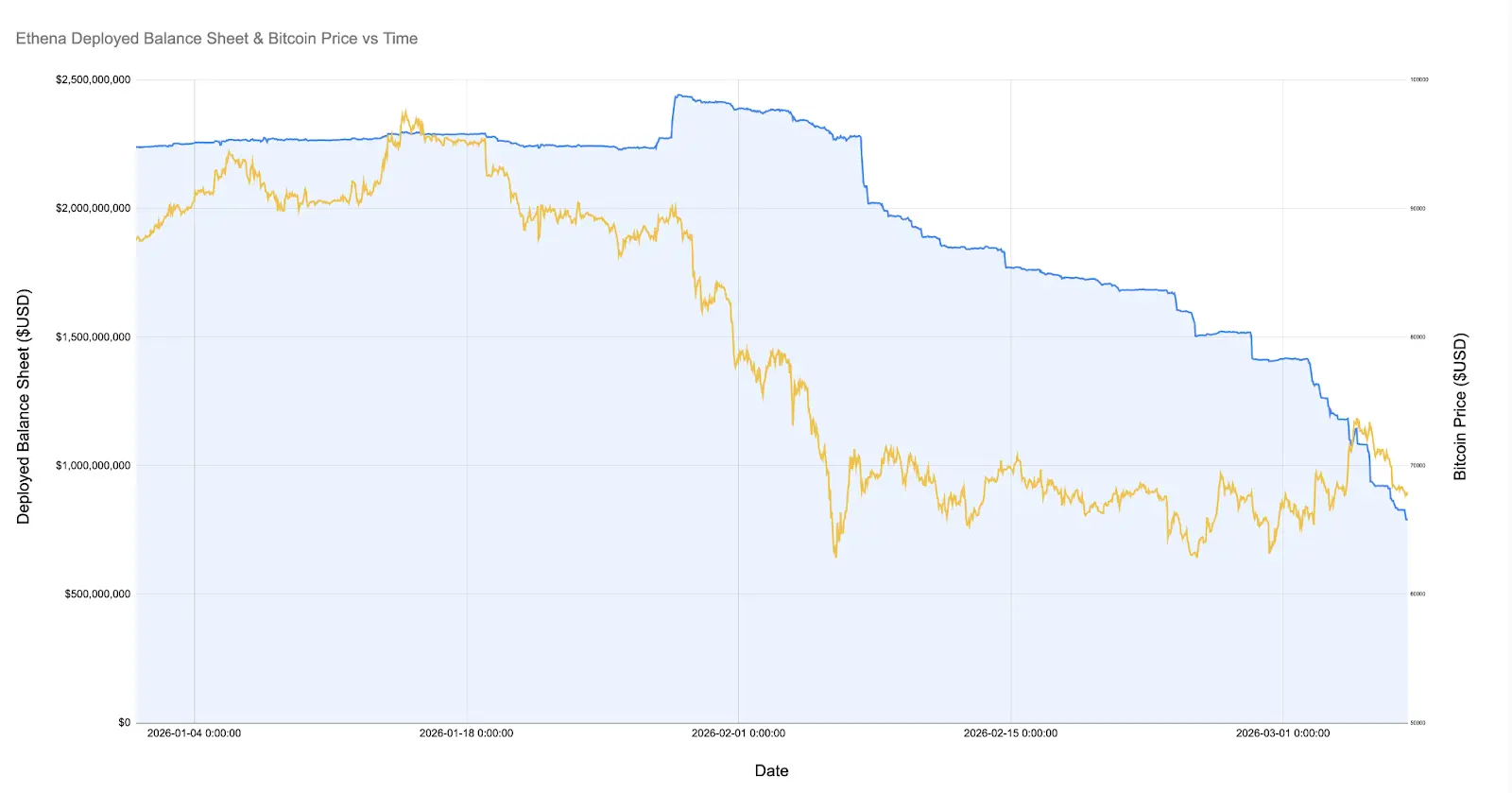

Specifically, during the market crash when Bitcoin price plunged below $60,000, Ethena’s deployed funds exceeded $2 billion. Since February 8, 2026 (a month ago), its deployed capital has fallen by an astonishing 60%.

The chart below zooms in on Ethena’s deployed capital since January this year and Bitcoin’s price.

Since Bitcoin dropped below $60,000, Ethena’s basis positions have shrunk by over 60%, from over $2 billion to less than $800 million. This change is puzzling because the market was relatively stable during this period. Possible explanations include:

-

Gradual unwinding of profitable but unsustainable basis trades created after the February crash (basis moved into favorable negative territory, but funding rates were also negative).

-

Competition from directional shorts and hedging activities by price-insensitive participants, squeezing out speculative basis traders.

-

Lack of long demand seeking leverage exposure.

Source: Coinglass

I believe the reality is largely a combination of factors 1 and 2, with factor 3 playing a smaller role. As shown in the chart, during Ethena’s liquidation period, the overall open interest in Bitcoin (and other major coins) remained relatively stable. Meanwhile, funding rates have been negative for quite some time, with many tokens like SOL showing negative cumulative funding rates across multiple exchanges. This indicates increasing demand for directional shorts or hedging certain risk exposures.

I think small crypto firms and VCs are experiencing a crisis. Consider small-cap projects like Eigen, Grass, Monad—these tokens number in the hundreds, each representing dozens of VCs, a treasury, and staff. VCs need to limit losses and lock in gains to meet investment targets, while companies need to protect cash flow and staff. This creates a scenario where all parties want to extract maximum value from limited resources, resulting in a relatively crowded trading environment: actively managed structured products shorting baskets of related assets.

Evidence of these structured products appeared during the explosive rise of ETH, which triggered short covering rebounds in many small and mid-cap crypto assets. Another sign is the large-scale squeezing out of speculative basis trades like Ethena’s.

Whatever the reason, it’s clear that long and short positions in the crypto market are nearly balanced—an unprecedented occurrence in history. While there’s no reason to believe this can’t become the new normal or that the situation needs to change, such a trend is rare when looking at other asset classes and markets.

Related: Ethena after the de-pegging wave: TVL halved, ecosystem setbacks, how to initiate a second growth curve?