Original Author | Stacy Muur (@stacy_muur)

Compiled | Odaily Planet Daily (@OdailyChina)

Translator | DingDang (@XiaMiPP)

Editor’s note: @BinanceResearch released a research report on the evolution of token models in June 2025, providing an in-depth review of the attempts and lessons learned in token design, incentive mechanisms, and market structure by Web3 projects over the past few years. From the bubble of the ICO era and the brief glory of liquidity mining, to the recent re-examination of issuance methods, governance means, and economic models by projects.

Stacy Muur compiled this report and distilled ten key observations, revealing core issues such as governance failures, low airdrop efficiency, fragmented models, and distorted supply. It also pointed out the market’s gradual return to “real demand” and “income support”. During market downturns, these insights may provide important references for the next phase of token issuance, valuation, and mechanism innovation.

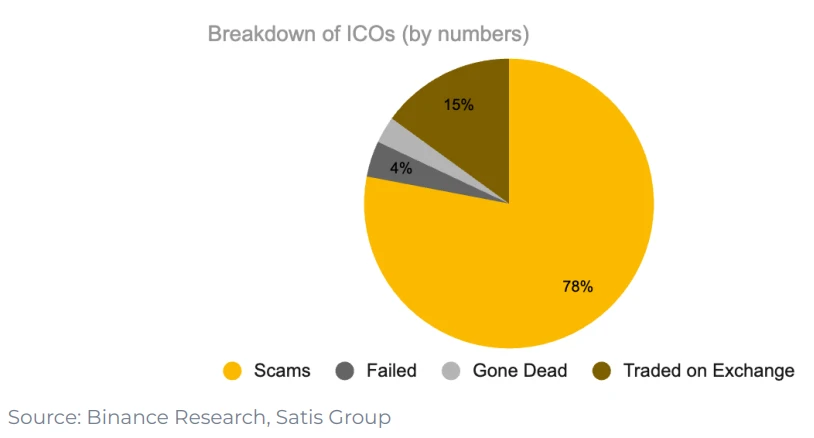

1. In the era of 1CO projects, only 15% ultimately succeed in launching on exchanges.

78% of projects are outright scams, while the rest either fail or gradually fade into obscurity. This indicates that the market at that time was filled with short-termism and lacked genuine sustainable building momentum.

2. The design of “governance” as a token utility has not truly been effective.

After the UNI airdrop, only 1% of wallets chose to increase their holdings, and 98% of wallets had never participated in any governance voting.

Governance sounds good in theory, but in practice, it often just means another way of saying “exit liquidity.”

3. Liquidity mining originated in 2019 with Synthetix, but failed to maintain long-term demand.

However, the “governance rights” did not maintain ongoing attention to the project. Data shows that 98% of airdrop recipients never participated in governance, and most people sold their tokens directly after the airdrop.

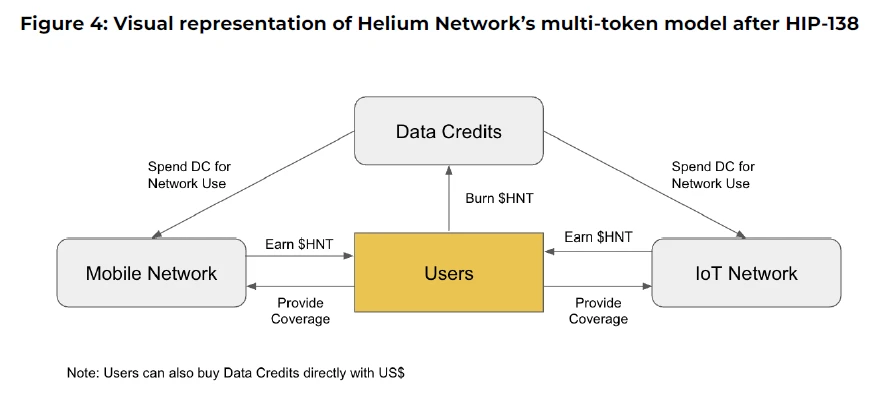

4. The multi-token model attempts of Axie Infinity and Helium failed

Projects like Axie Infinity and Helium have adopted a multi-token model that separates “speculative value” from “functional utility.” One token is used for value capture, while another is used for network usage.

But in reality, this kind of split did not work: speculators flocked to “functional tokens,” the incentive mechanism misaligned, and the value began to fragment. Ultimately, both projects had to revert to a simpler single-token design.

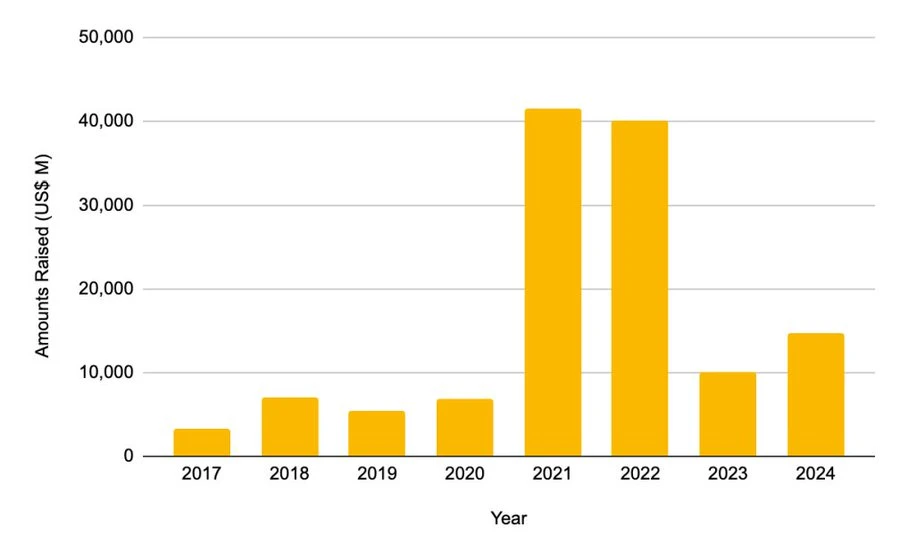

5. Private placement financing peaked in 2021 - 2022.

- The total financing amount in 2021 reached 41.46 billion USD

- 40.12 billion USD in 2022

This scale has already exceeded twice the total financing amount of the entire period from 2017 to 2020. However, this financing boom did not continue thereafter.

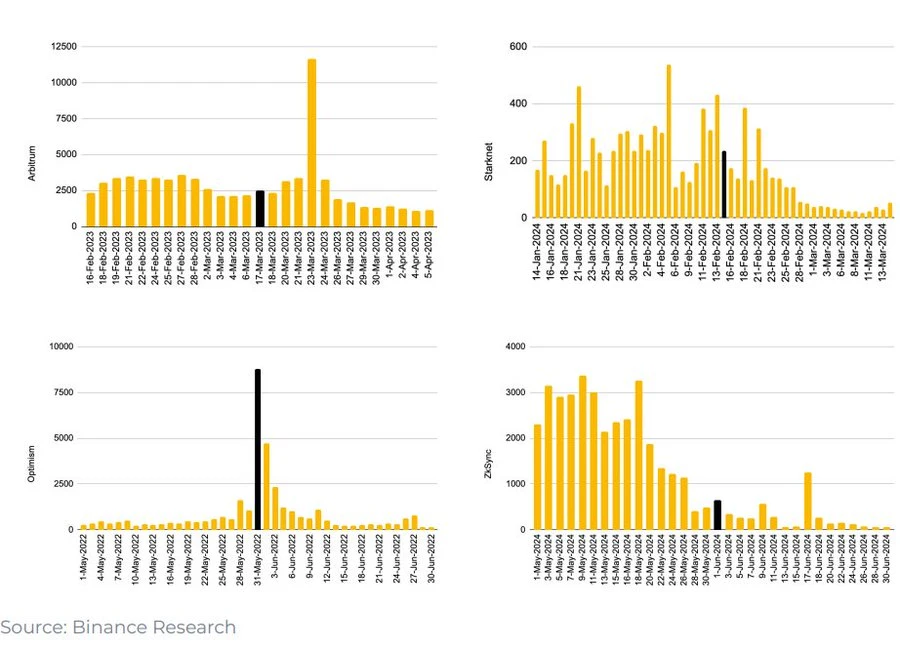

6. After the L2 airdrop snapshot, the usage of the cross-chain bridge plummeted.

Whenever L2 announces an airdrop snapshot, the usage of cross-chain bridges quickly declines. This means that the surge in usage does not stem from real demand, but rather is caused by airdrop hunters manipulating the exchanges.

Most users sell off tokens after an airdrop, while project teams often mistakenly regard this kind of short-term “traffic” as true product-market fit.

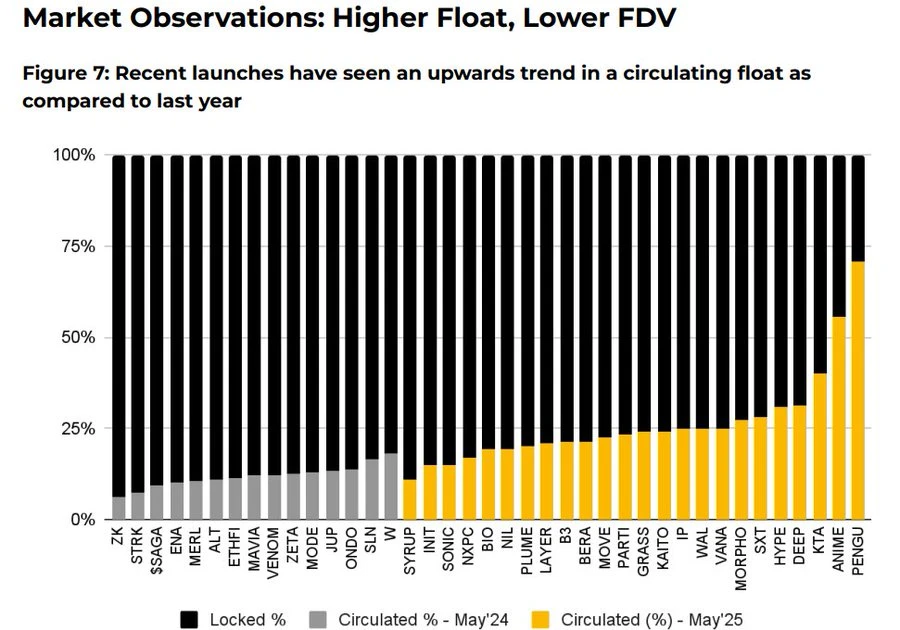

7. In 2025, the method of token issuance will change.

- The initial circulation of the market has significantly increased.

- Average Fully Diluted Valuation (FDV) decreased from $5.5 billion to $1.94 billion

Data shows that tokens with a higher circulation ratio and more reasonable valuation at the time of issuance perform better after being listed. The market is gradually rewarding more authentic and transparent token economic models.

8. Buyback Mechanism Returns

Protocols such as Aave, dYdX, Hyperliquid, and Jupiter have launched structured “redemption and destruction” plans, using protocol revenue to buy back tokens from the market and destroy them. This is both a symbol of financial health and a stopgap measure while the issue of “token lack of utility” has not yet been resolved.

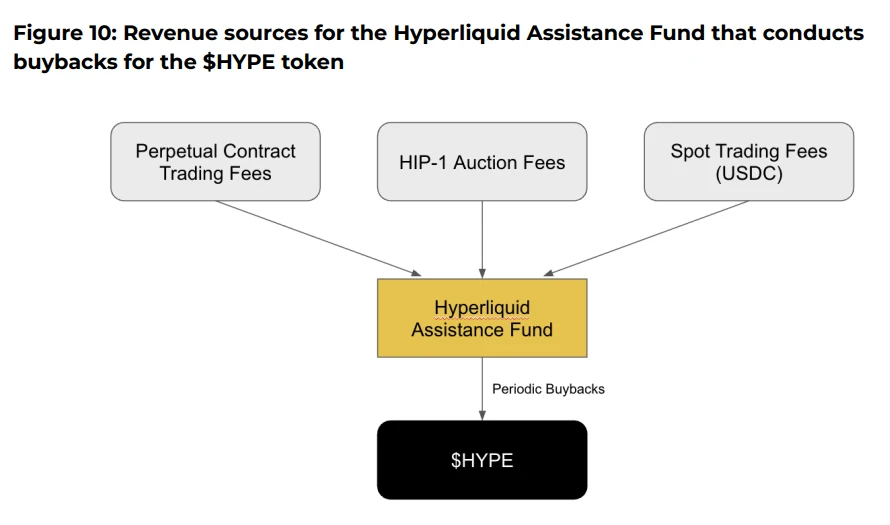

9. The Truth About Hyperliquid’s Buyback

Taking @HyperliquidX as an example, the protocol has repurchased and destroyed HYPE tokens worth over 8 million dollars, with these funds coming from 54% of its trading fee revenue. However, these repurchases did not provide dividends to token holders, but simply supported the token price by creating “scarcity.”

Critics argue that this buyback is a mismatch of capital. It creates artificial deflation instead of returning real profits to token holders. In contrast, token models with profit-sharing attributes may provide better incentive alignment.

10. The Believe App is an emerging player in the current ICM (Instant Create Market) narrative.

This application allows users to easily create tokens on the Solana chain by posting tweets in a specific format on X (formerly Twitter), such as “$TICKER + @launchcoin”, which will trigger price discovery and liquidity deployment through a bonding curve model, enabling the release and trading of community tokens without the need for development.

Final conclusion: Despite the continuous evolution of models, the utility of tokens remains an unresolved issue.

- The governance mechanism has been proven to lack user stickiness.

- The buyback plan is, to some extent, merely a substitute for the lack of intrinsic demand for the tokens.

- The points and airdrop mechanisms are more inclined towards short-term strategies.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.