Author: Daii Source: yzdxs.eth

I have always said: the current crypto market is more like a “wild west.”

The most glaring evidence is the “pinning”. It is not metaphysics, but rather the result of deep thinness + leveraged chain liquidation + the preference for on-site matching: the price is violently smashed to your stop-loss level in critical milliseconds, your position is wiped out, leaving only that long and thin “wick” in the K-line — like a needle suddenly piercing in.

In this environment, what is lacking is not luck, but the bottom line. Traditional finance has long established this bottom line in its systems - the prohibition of trade-through (Trade-Through Rule). Its logic is very simple, yet very powerful:

When there are clearly better public prices in the market, no broker or exchange should turn a blind eye, nor should they execute your order at a worse price.

This is not moral persuasion, but a accountable hard constraint. In 2005, the U.S. Securities and Exchange Commission (SEC) clearly wrote this bottom line into Reg NMS Rule 611: All market participants (where trading centers must not violate protected quotes, and brokers are additionally responsible for best execution under FINRA 5310) must fulfill “order protection,” prioritizing the best available price and leaving a traceable, verifiable, and accountable record of routing and execution. It does not promise “market stability,” but ensures that amidst volatility, your transactions are not arbitrarily “deteriorated”—if better prices are available elsewhere, you cannot be indiscriminately “matched on the spot” in this venue.

Many people will ask: “Can this rule prevent pinning?”

Straightforwardly: It cannot eliminate long needles, but it can cut off the damage chain of “long needles trading with you.”

Imagine a scene that is easy to understand at a glance:

- At the same time, Exchange A experienced a downward spike, instantly crashing BTC to $59,500;

- Exchange B still has $60,050 in valid buy orders hanging.

If your stop-loss market order is executed “on the spot” at A, you exit at the tip price; with order protection, the routing must send your order to the better buy price at B, or refuse to execute at the inferior price at A.

Result: The needle is still on the chart, but it is no longer your execution price. The value of this rule lies in not eliminating the needle, but in preventing the needle from piercing you.

Of course, the triggering of contract liquidation itself also requires supporting governance measures such as marking prices/indices, volatility bands, auction restarts, and anti-MEV to manage the “needle generation.” However, in terms of fair trading, the bottom line of “prohibiting transaction penetration” is almost the only immediate lever that can enhance the experience, is implementable, and can be audited.

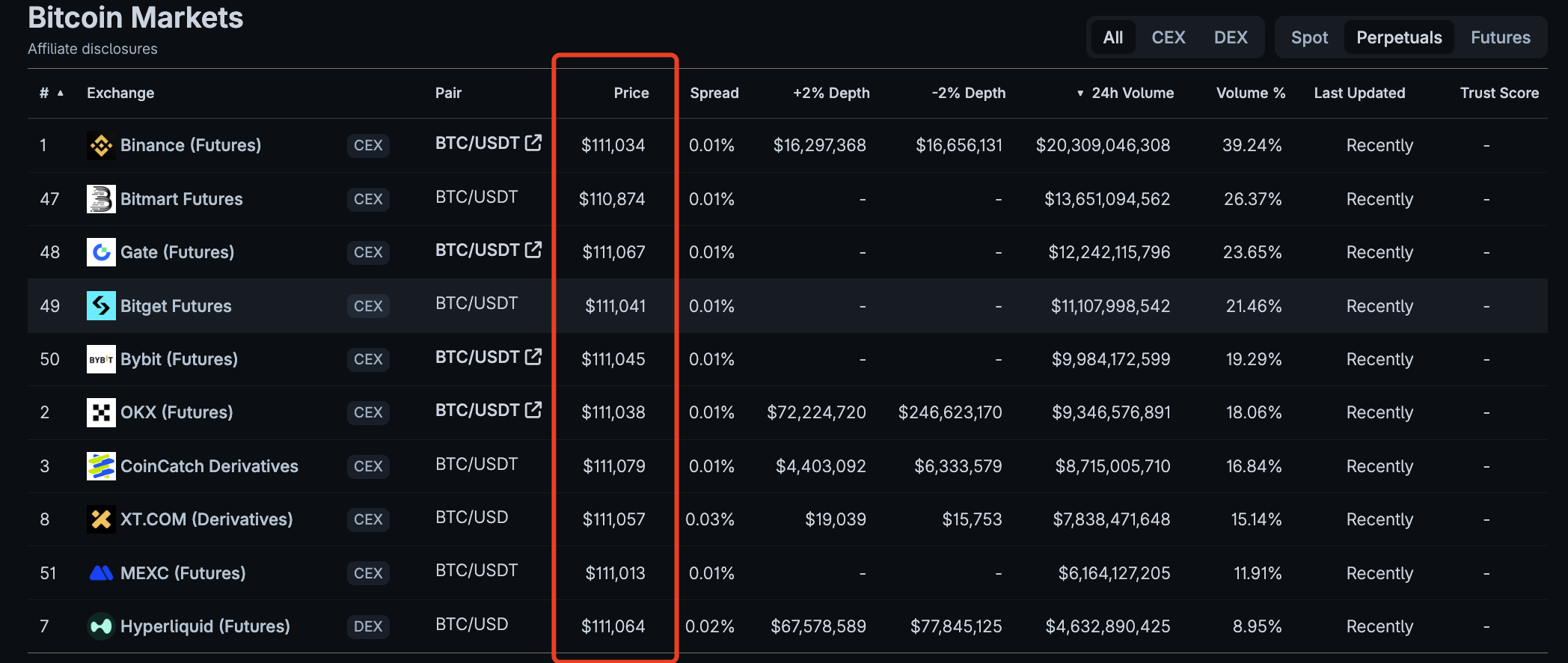

Unfortunately, the crypto market still does not have such a bottom line. A picture is worth a thousand words:

From the above BTC perpetual contract quote table, you will find that none of the quotes from the top ten exchanges by trading volume are the same.

The current landscape of the cryptocurrency market is highly fragmented: hundreds of centralized exchanges, thousands of decentralized protocols, with prices disconnected from one another. Coupled with the dispersion of cross-chain ecosystems and the dominance of leveraged derivatives, it is more difficult for investors to find a transparent and fair trading environment than climbing to the sky.

You might be curious why I am bringing up this question now.

On September 18, the U.S. Securities and Exchange Commission (SEC) will hold a roundtable meeting to discuss the pros and cons of the prohibition on the trade-through rule and its future in the National Market System (NMS).

This matter seems to be related only to traditional securities, but in my opinion, it also serves as a wake-up call for the crypto market: if trading protection mechanisms need to be reconsidered and upgraded in the highly concentrated and mature U.S. stock system, then ordinary users in the more fragmented and complex crypto market need the most basic lines of protection even more:

Cryptocurrency market providers (including CEX and DEX) must never ignore better public prices at any time, and must not allow investors to be executed at worse prices in situations that could have been avoided. Only in this way can the cryptocurrency market transition from the “Wild West” to true maturity and reliability.

This matter now appears to be a fantasy, and it would not be an exaggeration to say it is a delusion. However, once you understand the benefits that the establishment of the prohibition of trading through rules has brought to the US stock market, you will realize that, no matter how difficult it may be, it is worth a try.

1. How is the Trade-Through Rule established?

Looking back, the establishment of this rule has gone through a complete chain: from the legislative authorization in 1975, to the interconnection experiments of the Inter-Exchange Trading System (ITS), then to the comprehensive electronic leap in 2005, and finally phased implementation in 2007. It is not intended to eliminate volatility, but to ensure that investors can still obtain better prices that they deserve amidst the fluctuations.

1.1 From Fragmentation to Unified Market

In the 1960s and 1970s, the biggest problem facing the U.S. stock market was fragmentation. Different exchanges and market-making networks operated independently, and investors had no way of knowing where to get the “current best price” across the entire market.

In 1975, the U.S. Congress passed the Securities Act Amendments, which first explicitly proposed the establishment of a “National Market System (NMS)” and required the SEC to lead the development of a unified framework that could connect various trading venues, aiming to enhance fairness and efficiency [Congress.gov, sechistorical.org].

With legal authorization, regulators and exchanges have launched a transitional “Interconnection Cable” - the Inter-Exchange Trading System (ITS). It functions like a dedicated network cable that connects exchanges, allowing different locations to share quotes and routes, thereby avoiding the situation where better prices next door are ignored when a trade is executed at a worse price in the current location [SEC, Investopedia].

Although ITS has gradually faded with the rise of electronic trading, the concept of “no ignoring better prices” has already been deeply ingrained.

1.2 Regulation NMS and Order Protection

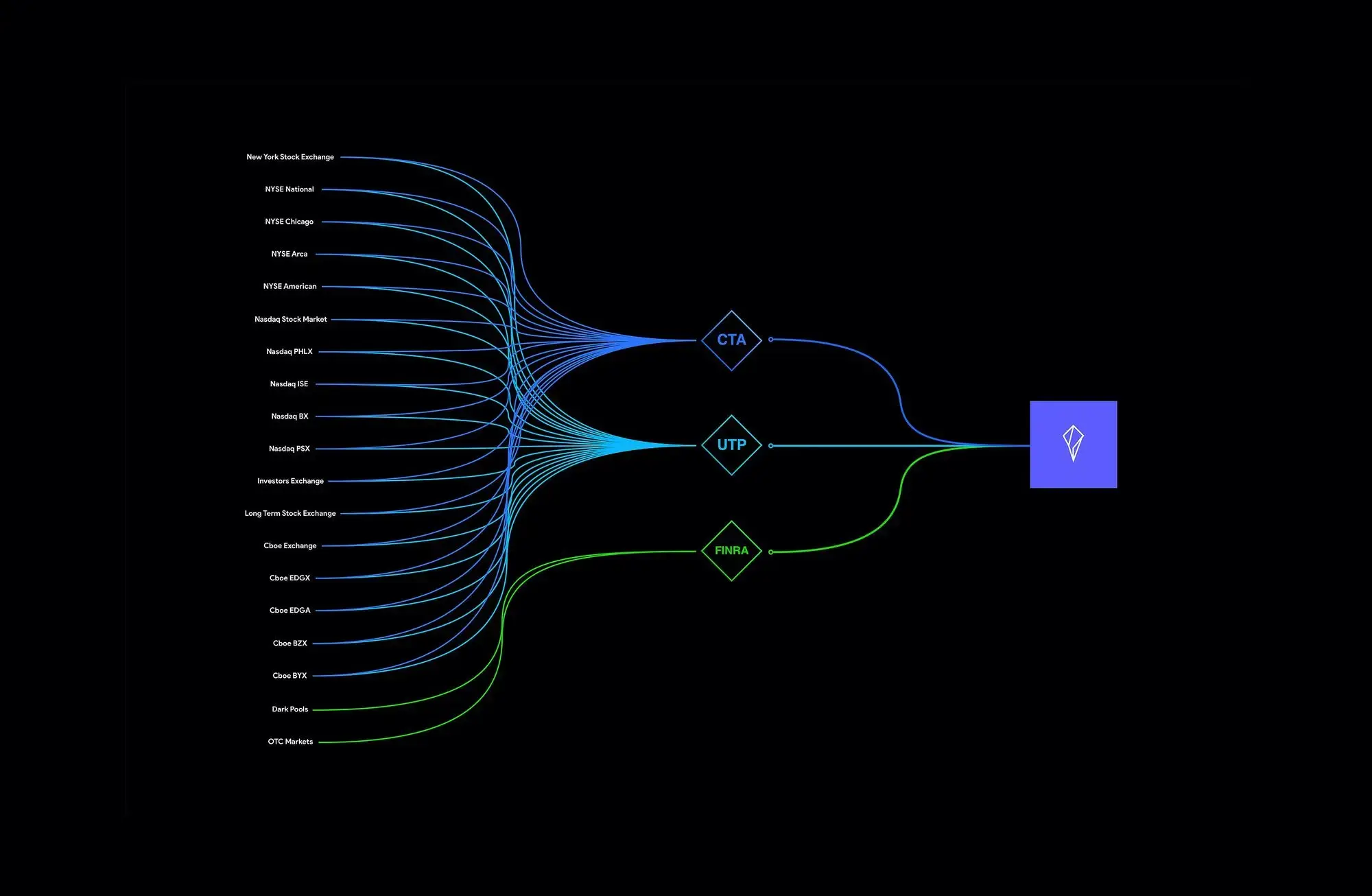

Entering the 1990s, the internet and decimalization made trading faster and more fragmented, and the old semi-manual system could no longer keep up. In 2004-2005, the SEC introduced historic new regulations—Regulation NMS. It includes four core provisions: Fair Access (Rule 610), Prohibition of Trade Through (Rule 611), Minimum Price Increment (Rule 612), and Market Data Rules (Rule 603)【SEC】.

Among them, Rule 611, also known as the “Order Protection Rule,” can be explained in simple terms as follows: when better protected quotes are already available in other venues, you cannot match an order at a worse price here. The so-called “protected quotes” must be quotes that can be executed automatically and instantly, and cannot be slow orders that are processed manually 【SEC Final Rule】.

To make this rule truly implementable, the U.S. market has established two key “foundations”:

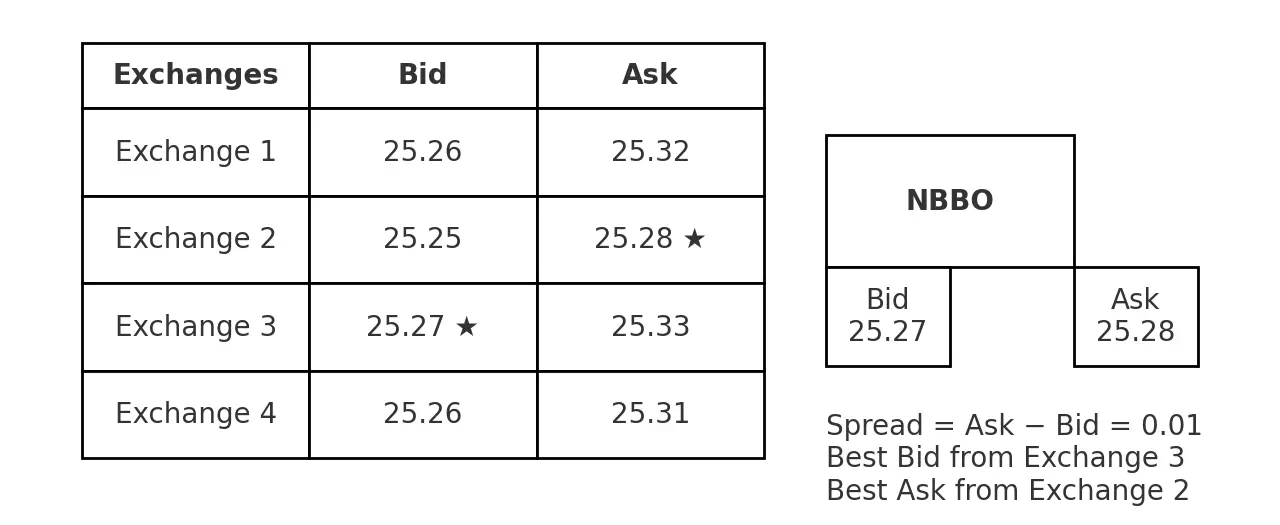

- NBBO (National Best Bid and Offer): Combines the best buy and sell prices from all exchanges to create a unified standard for measuring whether a transaction is “penetrating”. For example, the best buy price of 25.27 from Exchange 3 and the best sell price of 25.28 from Exchange 2.

- SIP (Securities Information Processor): Responsible for real-time aggregation and dissemination of this data, becoming the “single source of truth” for the entire market [Federal Register, SEC].

Reg NMS (Regulation National Market System) came into effect on August 29, 2005, and on May 21, 2007, it was first implemented on 250 stocks under Rule 611. On July 9 of the same year, it was fully extended to all NMS stocks, ultimately forming an industry-wide practice of “no trading through better prices”【SEC】.

1.3 Controversies and Significance

Of course, it hasn't been all smooth sailing. Back then, SEC commissioners Glassman and Atkins raised objections, arguing that focusing solely on displayed prices might overlook the net costs of trading and could even weaken market competition【SEC Dissent】. However, the majority of commissioners still supported this rule, and the reasoning is clear: even with debates about costs and efficiency, “prohibiting trade-through” at least ensures a fundamental baseline —

Investors will not be forced to accept inferior prices when better prices are clearly available.

This is why, to this day, Rule 611 is still considered one of the cornerstones of the “best execution ecosystem” in the U.S. securities market. It transformed the slogan “better prices cannot be ignored” into a reality that can be regulated and audited, allowing for accountability afterwards. And this baseline is precisely what is missing in the crypto market, yet is the most worthy of reference.

2. Why does the crypto market need this “bottom line rule” more?

Let’s put the question plainly: In the crypto market, at the moment you place an order, there may not be anyone “watching the whole scene” for you. Different exchanges, different chains, and different matching mechanisms act like isolated islands, with prices each singing their own tune. The result is that — clearly, there are better prices elsewhere, but you end up being “matched on the spot” at a worse price. This is explicitly prohibited in the US stock market by Rule 611, but there is no unified “safety net” in the crypto world.

The Cost of Fragmentation: Without a “Full Market Perspective”, It is Easier to be Executed at a Worse Price.

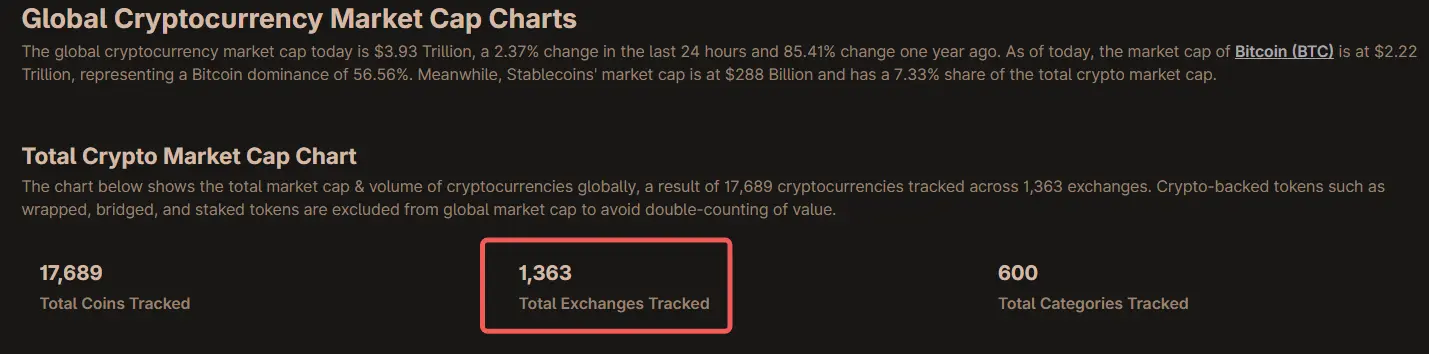

Looking at the present, there are thousands of registered cryptocurrency trading venues globally: CoinGecko's “Global Chart” alone shows that it tracks over 1,300 exchanges (as shown in the figure below); meanwhile, CoinMarketCap's spot rankings have long displayed more than two hundred active reporting exchanges—this does not even include the long tail venues of various derivatives and on-chain DEX. Such a landscape means that no one can naturally see the “best price in the entire market.”

Traditional securities rely on SIP/NBBO to synthesize the “best price range”; however, in crypto, there is no official merged price range, and even data institutions openly state that “crypto has no 'official CBBO'”. This makes the question of “where is it cheaper/more expensive” something that is only known afterward. (CoinGecko, CoinMarketCap, coinroutes.com)

2.2 Derivatives Dominance, Volatility Amplification: Pinning is more likely to occur and has a greater impact.

In cryptocurrency trading, derivatives have long accounted for a large share.

Multiple industry monthly reports indicate that the proportion of derivatives fluctuates annually between ~67% and 72%: for example, the CCData series of reports have reported readings of 72.7% (March 2023), ~68% (January 2025), ~71% (July 2025), etc.

The higher the proportion, the easier it is to experience instantaneous extreme prices (“spikes”) under the influence of high leverage and funding rates; once your platform does not engage in price comparison and does not calculate net prices, it may be subjected to inferior prices “executed on the spot” at the same moment when a better price is available.

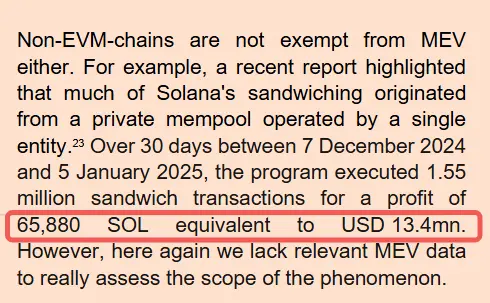

On the chain, MEV (Maximum Extractable Value) adds another layer of “implicit slippage”:.

- According to the European Securities and Markets Authority (ESMA) 2025 report statistics, in just 30 days from 2024/12 to 2025/1, there were 1.55 million sandwich trades with a profit of 65,880 SOL (approximately 13.4 million USD); (esma.europa.eu)

- Academic statistics also show that there are more than 100,000 attacks in a single month, with related Gas costs at the million-dollar level.

For ordinary traders, these are the real “execution losses”. (CoinDesk Data, CryptoCompare, The Defiant, CryptoRank, arXiv)

If you want to understand how MEV attacks occur, you can check out my article “A Complete Analysis of MEV Sandwich Attacks: The Fatal Chain from Ordering to Flash Swaps,” which details how an MEV attack caused a trader to lose $215,000.

2.3 There is technology, but it lacks a “principle safety net”: turning the “best price” into a verifiable commitment.

The good news is that the market has developed some “self-rescue” native technologies.

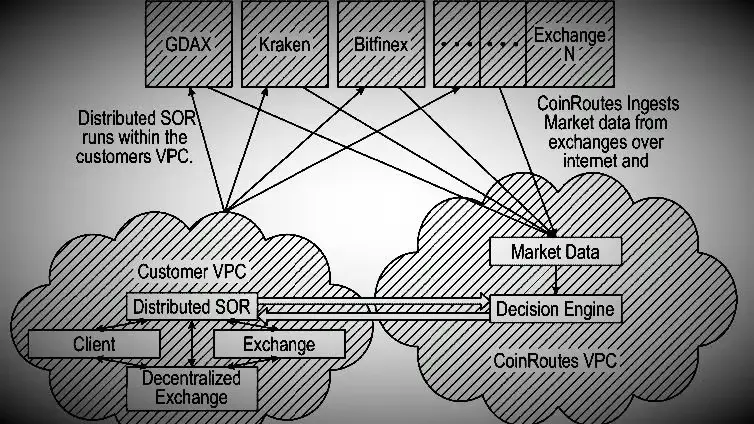

- Aggregators and smart routing (such as 1inch, Odos) will scan multiple pools/chains, split orders, and factor in Gas and slippage into the “real transaction cost” to strive for a better “net price”; (portal.1inch.dev, blog.1inch.io)

- Private “Best Price Aggregation” (like CoinRoutes' RealPrice/CBBO) combines the depth and fees of dozens of venues in real-time into a “tradable, charged reference net price,” which has even been adopted by Cboe for indexes and benchmarks. This demonstrates that “finding better prices” is technically feasible. (Cboe Global Markets, Cboe, coinroutes.com)

But the bad news is: there is no bottom line for “prohibition of penetration”; these tools are merely voluntary choices, and the platform can completely match your order “on the spot” without checking or comparing.

In traditional securities, best execution has long been written as a compliance obligation—considering not only price but also weighing speed, likelihood of execution, costs/rebates, and conducting “regular and rigorous” assessments of execution quality; this is the spirit of FINRA Rule 5310. Introducing this “principle + verifiability” into crypto is the key step that truly turns the slogan “better prices cannot be ignored” into a commitment. (FINRA)

In a word:

The more fragmented, 24/7, and derivative the cryptocurrency market becomes, the more ordinary people need a bottom-line rule of “not to ignore better publicly available prices.”

It does not necessarily have to replicate the technical details of the US stock market; however, at the very least, the obligation of “not penetrating” should be elevated to an explicit duty, requiring the platform to either provide a better net price or give verifiable reasons and evidence. When “better prices” become a verifiable and accountable public commitment, the unjust losses caused by “price manipulation” are more likely to be truly addressed.

3 Can the Trade-Through Rule really be implemented in the cryptocurrency world?

Short answer: Yes, but it cannot be applied rigidly.

Copying the mechanical version of the “NBBO+SIP+mandatory routing” model from the US stock market is almost infeasible in crypto; however, elevating the principle of “not ignoring better publicly available prices” to a mandatory obligation, along with verifiable execution proof and a market-based merger price band, is entirely feasible and there are already “semi-finished products” being used in the community.

Step 1: Look at Reality: Why is the Crypto World Difficult?

There are three main difficulties:

- There is no “Consolidated Tape” (SIP/NBBO). The reason why the US stock market can prevent price penetration is that all exchanges feed data into the Securities Information Processor (SIP), providing the entire market with a nationwide best bid and offer (NBBO) as a “common standard”; however, cryptocurrencies lack an official market price feed, resulting in prices being fragmented into many “information islands.” (The market data and consolidated tape of Reg NMS have been continuously refined from 2004 to 2020. (Federal Register, U.S. Securities and Exchange Commission ))

- The settlement “finality” is different. Bitcoin commonly requires “6 confirmations” to be relatively secure; Ethereum PoS relies on epoch finality, which takes some time to “pin down” the block. When you define “protected quotes that can be executed instantly,” the meaning and delay of “executable/final on-chain” must be clearly rewritten. ( Bitcoin Encyclopedia, ethereum.org )

- Highly fragmented + derivatives dominated. CoinGecko alone tracks over 1,300 exchanges, while the spot rankings on CMC consistently feature around 250; adding DEX and long-tail chains makes the fragmentation even greater. Derivatives usually account for 2/3–3/4 of trading volume, with volatility amplified by leverage, leading to more frequent “flash spikes” and sudden deviations. (CoinGecko, CoinMarketCap, Kaiko, CryptoCompare)

3.2 Step 2: Look for opportunities: The ready-made “parts” are actually already in motion.

Don't be scared by the “no official price range” - a preliminary form of the “merger price range” already exists in the market.

- CoinRoutes RealPrice/CBBO: Synthesizes the depth, fees, and volume constraints of over 40 exchanges in real time to create a tradable merged best price; Cboe signed an exclusive license back in 2020 for digital asset indices and benchmarks. In other words, “routing decentralized prices to a better net price” is technically mature. (Cboe Global Markets, PR Newswire)

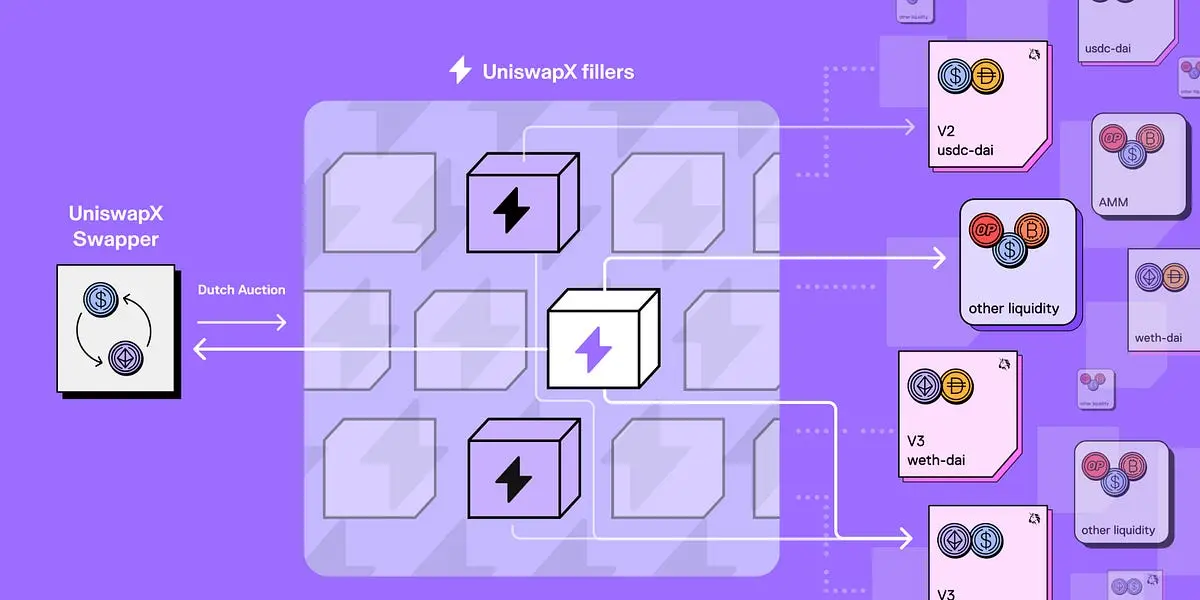

- Aggregators and Smart Routing (as shown in the figure above): They will break down orders, find paths across pools/chains, and include Gas and slippage in the real transaction cost; UniswapX further uses auction/intention aggregation on-chain + off-chain liquidity, bringing zero-cost failure, MEV protection, scalable cross-chain capabilities, essentially pursuing “verifiable better net prices.” (blog.1inch.io, portal.1inch.dev, Uniswap documentation)

Step 3 Look at the rules: Don't force a “single bus”, establish the “bottom line principle”.

Unlike the US stock market, we do not forcefully create a global SIP, but instead advance in three layers:

- Principle of Prioritization (Same Compliance Circle): Establish a clear obligation of “not to penetrate better public prices/net prices” among compliant platforms/brokers/aggregators within a single jurisdiction. What is meant by “net price”? It not only looks at the nominal price on the screen but also takes into account fees, rebates, slippage, Gas, and costs of failed retries. Article 78 of the EU MiCA has already written “best result” into a statutory list (price, cost, speed, execution and settlement possibilities, scale, custody conditions, etc.); this principled stance can fully become an anchor for the “crypto version of anti-penetration.” (esma.europa.eu, wyden.io)

- Market-based merged price band + random sampling verification: Regulatory approval recognizes multiple private “merged price bands/reference net prices” as one of the compliance baselines, such as the aforementioned RealPrice/CBBO; the key is not to designate a “unique data source,” but to require methodological transparency, coverage disclosure, conflict explanation, and conduct random comparisons/external sampling. This avoids “monopoly” and provides practitioners with a clear verifiable benchmark. (Cboe Global Markets)

- “Best Execution Evidence” and Periodic Reconciliation: The platform and broker must keep records: which venues/routes were searched at the time, why a potentially better nominal price was abandoned (e.g., settlement uncertainty, high gas fees), and the final transaction net price versus the estimated difference. Referring to traditional securities, FINRA Rule 5310 requires a “per-order or 'periodic and rigorous'” execution quality assessment (at least quarterly, by category), and the crypto sector should adopt the same level of self-certification and disclosure. (FINRA)

3.4 Step Four: Look at the Boundaries: Innovation should not be “stifled.”

The principle is “not to ignore better public prices”, but the implementation path must be technology-neutral. This is also the insight from the U.S. reopening of Rule 611 roundtable: even in the highly concentrated U.S. stock market, order protection is being reconsidered for upgrades, and there can be no “one-size-fits-all” approach in cryptocurrency. ( U.S. Securities and Exchange Commission, Sidley )

So, what will the landing look like? Here’s a very “hands-on” picture for you to imagine:

- You place an order on a compliant CEX/aggregator. The system first queries multiple venues/multiple chains/multiple pools, references private merged pricing, and accounts for fees, slippage, Gas, and expected final time for each candidate path; if a certain path has a better nominal price but does not meet finality/cost standards, the system clearly states the reasons and retains evidence.

- The system selects a route with a better comprehensive net price that can be executed in a timely manner (splitting orders if necessary). If it does not route you to a better net price at that time, the subsequent report will highlight this in red, becoming a compliance risk point that must be explained or even compensated if audited.

- You can see a concise execution report: optimal obtainable net price vs actual net price, path comparison, estimated vs actual slippage/fees, transaction time and on-chain finality. Even the most sensitive novices to “pinning” can determine: Am I being “priced down” here?

Finally, let's clarify the “worry point”:

- “Is it impossible without a global NBBO?” Not necessary. MiCA has already applied the principle of “best execution” to crypto asset service providers (CASP), emphasizing multiple dimensions such as price, cost, speed, execution/settlement possibilities; the self-certification + random inspection tradition of U.S. stocks can also be utilized. By using the merged price bands of multiple companies + auditing reconciliation, a “consensus price band” can be established, rather than forcing a “central price band”. (esma.europa.eu, FINRA)

- “Will there still be slippage if there is MEV on-chain?” This is precisely the issue that protocols like UniswapX (as shown in the image above) aim to solve: MEV protection, zero-cost failure, cross-source bidding, and returning the margins originally taken by “miners/ordering” as price improvement as much as possible. You can think of it as a “technical version of order protection.” (Uniswap documentation, Uniswap)

In conclusion, in one sentence:

In the cryptocurrency space, implementing “anti-piercing” is not about copying the mechanical rules of the U.S. stock market, but rather anchoring to principles and obligations at the level of MiCA/FINRA. This should combine private merger pricing and on-chain verifiable “best execution proof,” starting from the same regulatory fence and gradually expanding outward. As long as we turn the commitment that “better publicly available prices cannot be ignored” into an auditable and accountable promise, even without a “global bus,” we can mitigate the harm of “pinning” and try to recover every cent that retail investors are entitled to from the system.

Conclusion | Turning “Best Price” from a Slogan into a System

The cryptocurrency market is not lacking in smart codes; what is lacking is a bottom line that everyone must abide by.

Prohibiting trading penetration is not about tying up the market, but about clarifying responsibilities and rights: the platform should either send you to a better net price or provide verifiable reasons and evidence. This is not “restricting innovation”; rather, it paves the way for innovation—when price discovery is fairer and execution is more transparent, truly efficient technologies and products will be amplified.

Stop treating “pinning” as the fate of the market. What we need is a technically neutral, verifiable results, and layered approach to a crypto version of “order protection.” Turn “better prices” from a possibility into an auditable commitment.

Only better prices “must not be ignored” for the crypto market to be considered mature.