Compiled and organized by: @sanqing_rx

Copyright and Data Source: Dune × RWA.xyz “RWA REPORT 2025”. This article is a secondary arrangement in Chinese, and the data and charts are based on the original report.

TL;DR

- Scaling national debt → Diversifying credit / stocks / commodities: RWA has extended from the “risk-free rate” to a higher risk-return curve, becoming the collateral and yield layer of DeFi.

- Composability is the key breakthrough: the combination of collateral, yields, and secondary liquidity is transforming RWA from “holding” to programmable capital markets.

- Dual-driven by institutions and retail: Institutional products like BUIDL / JTRSY / OUSG serve as the foundation, while xStocks / GM / XAUm enhance retail accessibility; RealtyX brings real cash flow (real estate) into the DeFi space.

1) Key Conclusions

- U.S. Treasuries serve as the base, extending to higher-yield asset types: Treasury bonds lead in scaling up, becoming the “base liquidity” and a reliable anchor; funds extend along the yield curve to long-duration bonds / private credit / equities / commodities / alternative assets.

- Composability is the core breakthrough: combining collateral (Aave / Morpho), yield (Pendle), secondary and derivatives (Ostium / xStocks / Ondo Global Markets) to transform “holding assets” into programmable capital market components.

- Institutional + Retail Dual-Drive: Institutional Base (BUIDL / JTRSY / OUSG / WTGXX / USYC) provides compliant supply and settlement; Retail Entrance (xStocks / GM / XAUm) expands the reachable users and secondary activity; RealtyX brings real estate cash flow into the DeFi scenario.

- Accessibility has been greatly enhanced: lower entry barriers, multi-chain distribution, and the popularization of near-instant redemption are driving the migration of funds from off-chain notes to on-chain collateral.

- Scope Definition: Stablecoins focused on payment/settlement and significantly larger than yield-bearing RWAs are not included in this report.

The Significance of Tokenization 2)

- Ownership and settlement: Paper / Custody → Digitalization / T+1 → On-chain T+0, real-time NAV, atomic settlement.

- Collateral and Earnings: Customized Margin / Repurchase → Securities Lending / Money Market Fund → Universal On-chain Collateral + Programmable Earnings (Auto Reinvestment, Earnings Tiering).

- Cross-border and Interconnectivity: Local Market → Cross-border Standardization → 7×24 Global Interconnection, with cross-chain and account abstraction enhancing accessibility.

- Product Form: Direct Holding → Structured Pool → Programmable Asset Pool + Repackaging / Layering (deJAAA, USDY, etc.).

3) Market Overview (as of 2025-09)

- US Treasuries: ≈ $7.3B (up 85% year-to-date) — led by BlackRock, WisdomTree, Ondo, Centrifuge, etc.; Aave / Morpho and other collateral integrations enhance its “underlying currency” status.

- Global Bonds: ≈ $0.6B (up 171% year-to-date) — Spiko's EUR money market fund and sovereign assets serve as a breakthrough, primarily supported by Arbitrum / Polygon and others.

- Private Credit: ≈ $15.9B (up 61% year-to-date) - Driven by Figure / Tradable / Maple, moving from “risk-free rates” to “credit spreads.”

- Product: ≈ $2.4B (up 127% year-to-date) — Gold dominant, diversification into agricultural products / energy initiated.

- Institutional Funds: ≈ $1.7B (up +387% this year) — Tokenization acceleration of multi-strategy funds like Centrifuge's JAAA, Superstate's USCC, and Securitize's MI4.

- Stocks: ≈ $0.3B (after excluding the noise from EXOD and tokenized private placement stocks, +560% year-to-date) - retail-oriented, with secondary and cross-chain liquidity starting to gain traction.

4) Eight Major Sectors and Representative Projects

4.1 Government Bonds (U.S. Treasuries)

- BlackRock BUIDL (Securitize Distribution): Since its launch in March 2024, it has grown to $2.2B, making it the largest single tokenized asset, significantly driving the expansion of the government bond sector. Features: $1 NAV, daily distribution, multi-link integration (including ETH / Solana / Avalanche / L2 / Aptos) and direct USDC withdrawal.

- Ondo OUSG / USDY: OUSG is aimed at qualified investors in the U.S. and indirectly holds BUIDL; USDY is aimed at non-U.S. investors, with cumulative returns, natively programmable, supporting multi-chain and on-chain P2P transfers, with active liquidity and minting/redemption.

- Janus Henderson Anemoy — JTRSY: TVL ~$337M; NAV ~$1.08; management fee 0.25%. It is one of the first government bond tokens accepted as collateral by Aave Horizon, with a total supply exceeding $28M, reflecting the composability of RWA.

- WisdomTree WTGXX: A registered money market fund with AUM ~$830M; Features: stable $1 NAV, 7-day SEC yield ~4.1%; has been launched on ETH, Arbitrum, Base, Optimism, Avalanche, Stellar, supporting USD / USDC / PYUSD subscriptions and redemptions.

- Franklin Templeton BENJI (FOBXX): Multi-chain issuance, low entry threshold (starting at $20), T+1 redemption, real-time NAV; cumulative dividends ~$51M (monthly high of $2.7M in July 2025), with significant distribution across chains such as Stellar, Ethereum, and Arbitrum.

- Circle USYC: Tokenized currency fund, interoperate natively with USDC, near-instant redemption. Market cap ~$669M, 73% on BNB Chain (2025-09-04), and $492M held by three addresses, indicating a preference for institutional/treasury management use cases.

- Nest Protocol — nTBILL (Plume): A treasury bond-like underlying asset on Plume, with yields directly incorporated into the token price; the underlying assets are diversified (including Janus Henderson, Superstate USTB, etc.), and support usage in DEX/ lending/ collateral within the Plume ecosystem.

4.2 Global Bonds

- Spiko — EUTBL (Euro T-Bill Money Market Fund): TVL ~€300M, Arbitrum accounts for ~50%, followed by Polygon (~38%) and Starknet (~9%, with 8× growth over the year); total dividends accumulated over the year >€3M; active minting and redemption, with considerable single-transaction scale, suitable for cash management in the Eurozone and low-cost L2 use cases.

- Spiko — USTBL (US Dollar T-Bill Money Market Fund): The proportion of active minting and redemption days is 59%, with an average single minting of ~$0.75M and an average single redemption of ~$0.27M, which is more in line with the vault-type demand for “low-frequency rebalancing after allocation.”

- Etherfuse Stablebonds (Mexico CETES / US USTRY / Brazil Tesouros, etc.): Inclusive access and flow distribution centered around localized sovereign debt yields, active addresses (trust lines) >1,200, with CETES performing leading.

4.3 Private Credit

- Overall: Tokenized private credit ~$15.9B; “Risk-free rate → Credit spread” becomes the upward main line for 2025.

- Maple Finance: AUM ~$3.5B (YoY 12×); syrupUSDC ~$2.5B (Spark $400M+ allocated and expanded to Solana); permissioned high-yield pool ~$550M. DeFi deployment ~$833M (>30% supply), among which Spark ~$571M (70%) leads, with Jupiter Lend, Pendle, Morpho, Kamino, etc. forming a cross-chain composable yield network.

- Tradable (zkSync Era): 38 tokenized private credit transactions, active loans ~$2.1B; tokenized distribution and secondary paths aimed at institutional-level assets, emphasizing full-process compliance and composability.

- Pact (Aptos): An on-chain credit factory covering issuance / services / tiered securitization, focusing on low-cost compliant credit in emerging markets and global capital connectivity.

4.4 Commodities

- Matrixdock — XAUm (Gold): Supply increased to ~$45M; multi-chain distribution, with significant trading activity in DEX over the past year (BNB ecosystem dominates).

- Mineral Vault (Oil and Gas Mineral Rights): Targeting divisible U.S. oil and gas revenue rights, emphasizing “low friction, investable” securitization path, with the on-chain valuation and activity of the token MNRL rising.

- Spice (Plume): Building liquidity and data layers for commodity financing, with TVL continuously growing, providing lending/market-making and dashboard capabilities for the DeFi nativeization of commodity RWA.

- (Industry Context): Gold remains dominant, with agricultural products / energy / precious metals starting in multiple points, and the combinable links of commodity RWA → derivatives / market making are taking shape.

4.5 Institutional Funds

- Centrifuge — JAAA (Janus Henderson AAA CLO Fund): Surpassed ~$750M TVL in just two months; primarily ETH, Avalanche >$250M; reflecting the trend of funds shifting from government bonds to higher-yielding RWA.

- deJAAA (Transferable Packaging): Launched on 2025-08-08, with a trading volume of ~$1M in early September at Aerodrome; on 2025-09-12, it will expand to Solana and integrate with Raydium / Kamino / Lulo, etc. It will be tradable on Coinbase DEX / OKX Wallet / Bitget Wallet, with rapid enhancement of secondary composability.

- Market size: Tokenized institutional funds ~$1.7B (as of 2025-09), in collaboration with leading managers such as Centrifuge / Securitize / Superstate for scaling.

4.6 Stocks

- Ondo Global Markets (GM): Launched on 2025-09-03; First week mint and redemption >$141M, secondary trading ~$40M; The scale of tokenized stocks and ETFs on the platform >$150M, rapidly approaching $200M TVL; Supports 24/5 instant mint and redemption at NAV, cross-chain expansion to Solana / BNB, etc.

- Backed Finance — xStocks (Solana): AUM >$60M (two months); Tesla $15.3M (25%) leads, followed by SPY (11%)/NVIDIA (9%)/Circle (8%)/Strategy (8%); primarily driven by retail, with overlapping liquidity from CEX and DEX.

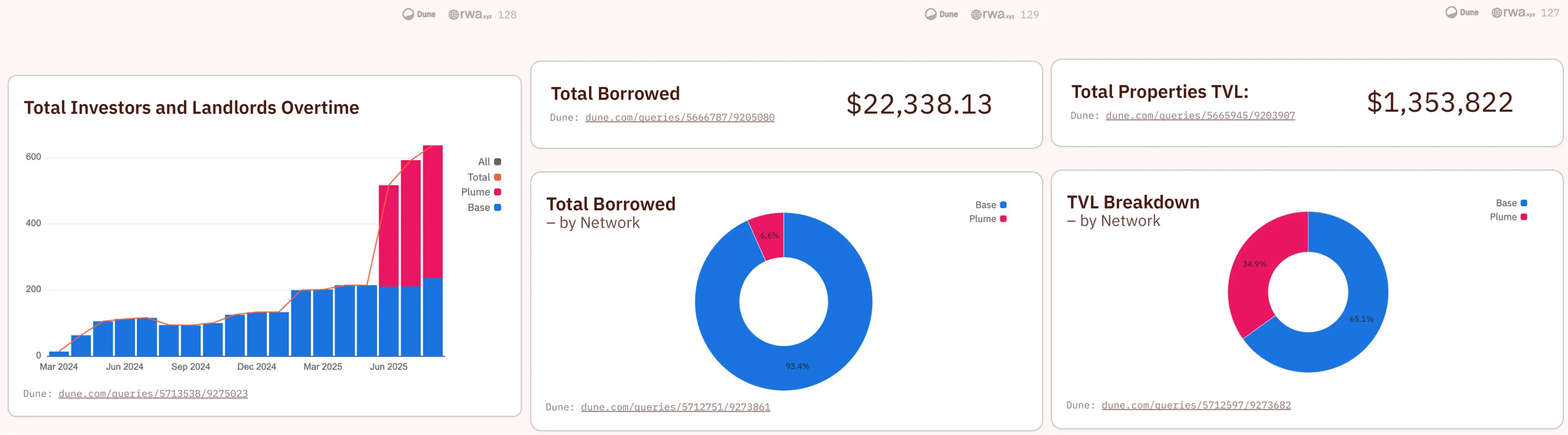

4.7 Real Estate

- RealtyX: RWA Launchpad (Asset On-chain / Issuance) + Utility Vault (Staking / Liquidity / Yield Tools) + DAO Governance (Listing and Platform Evolution).

- Scale and Network: TVL ~$1.35M (2025-09-10); Base 65% / Plume 35%.

- User structure: Total ~638 (Plume 62% / Base 38%).

- Cash flow and lending: average rental yield ~6.9%, cumulative dividends ~$15K+; already mortgaged and lent out ~$22K+ in the Base/Plume lending pool.

4.8 Platform / Infrastructure (Perps & Aggregators)

- Ostium (Arbitrum): RWA perpetual contract platform, cumulative transaction volume ~$17.8B, open interest >$140M; provides synthetic exposure to forex / commodities / indices / stocks, bringing RWA into high-frequency trading layer, significantly amplifying user reach and liquidity.

- VOOI: Cross-chain perpetual aggregator, covering EVM + non-EVM, account abstraction and non-custodial experience, aggregating RWA-related derivative liquidity.

5) Summary: Four Key Points for the Next Phase

- Composable scalability: an integrated path for collateral / yield / derivatives.

- Improvement of multi-currency / multi-region sovereignty and currency funds: Expanding deposit and risk hedging tools.

- Real cash flow assets (such as real estate) DeFi transformation: bidirectional connectivity between the funding side and the scenario side.

- Compliance and Multi-Chain Distribution Collaboration: KYC, taxation, secondary market mechanisms, and cross-chain settlement.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.