The payment industry in 2025 is at a turning point. The once universal pursuit of efficiency has now evolved into competition among various market systems, each with its unique concepts, capabilities, and limitations. Some systems focus on achieving control and interoperability through central infrastructure, while others prioritize Decentralization, Programmability, and private tracks. There are also systems that embed payment functionalities into platforms, devices, and networks that are traditionally unrelated to finance.

The flow of funds is becoming as critical as the amount of funds. Whether it's salary payments in Southeast Asia, inter-company settlements in Europe, or retail checkouts in Latin America, the design choices made today are shaping the payment landscape for the next decade and will determine who will lead, who will follow, and who will lag behind.

The global financial system is influenced by non-financial factors such as tariffs, data governance rules, energy constraints, and national security priorities. The increasing fragmentation in the payment sector reflects that the entire financial system is evolving into a regional puzzle composed of different standards, timelines, currencies, and trust anchors.

In this context, the payment industry remains the most valuable part of financial services, generating $2.5 trillion in revenue from a value flow of $20 trillion (0.125% take rate), supporting a global transaction volume of 3.6 trillion transactions.

Thus, we will integrate the payment and finance of stablecoins/tokenized currencies into the entire global payment landscape. From the perspective of Fintech, who will integrate and how to integrate these fragmented systems caused by geopolitical factors, as well as how to adapt to the next payment era's development based on one's own advantages, is a question that all market players need to consider at present.

The “2025 McKinsey Global Payments Report” provides an in-depth analysis of the rise of diverse payment tracks, the impact of digital assets, and the transformative power of artificial intelligence, offering a roadmap for success in the rapidly evolving global payment ecosystem. The report highlights the key elements necessary to remain competitive in a fast-changing environment. This report is based on McKinsey's “Global Payments Map,” which covers data from 50 countries and over twenty payment methods, accounting for 95% of global GDP. The report is divided into three main sections:

- A detailed analysis of the fundamental predictions for industry growth before 2029, examining how economic fluctuations and policy changes lead to significant differentiation in profit margins and revenue structures. The focus is on whether new revenue points can emerge from the integration of multiple payment tracks, which is an important driving factor for the development of payments.

- The main forces reshaping the payment landscape include the monetization of AI-native operations and AI agents, emerging models of Programmability payment liquidity, and regulated digital currencies. Focus on what changes these emerging forces will bring to the original models.

- Payment operators should focus on agility, architecture, and trust in the transformation system. The key consideration is how to capture value.

1. Payment Income in the New Economic Era

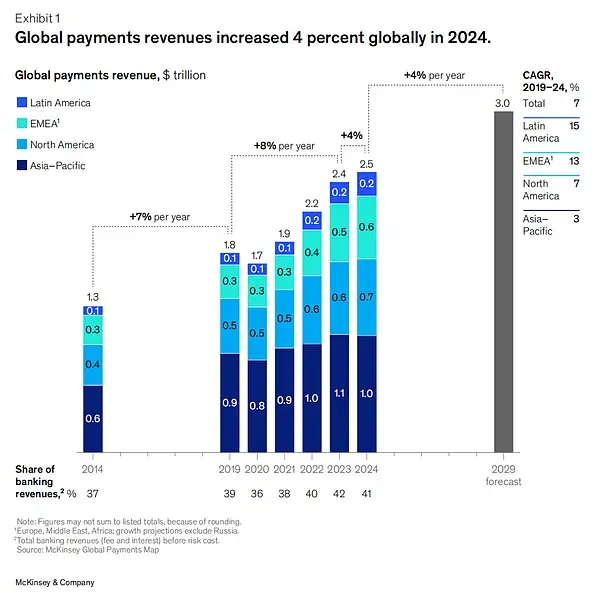

From 2019 to 2024, global payment revenue is expected to grow at an average annual rate of 7%. Driven by rising interest rates, interest income is projected to account for 46% of total revenue in 2024. The growth rate for that year is expected to drop to 4%, significantly lower than the 12% in 2023. Reasons for the slowdown include: peak interest rates, weakening macroeconomic conditions, structural expansion of low-yield payment methods, and ongoing fee compression.

By region, Latin America grew by 11%, EMEA and North America increased by 8% and 5% respectively, while Asia-Pacific (APAC) declined by 1%. Nevertheless, payments remain the most valuable sub-industry in the financial sector, with an average return on equity of 18.9% in 2024, and some institutions exceeding 100%.

However, as interest rates peak and decline in multiple countries, and changes in deposit behavior occur, net interest income is expected to grow at an annual average of only about 2% (by 2029), barring any significant shocks. At the same time, consumers are increasingly inclined towards low-cost methods such as account direct transfers and digital wallets, causing the growth of transaction-based income to also slow down. Ongoing pricing pressure (especially in the card-based ecosystem), tightening regulations, and the rise of platform-based payment experiences are squeezing the fee model. Therefore, we predict that the industry's revenue growth rate will maintain an annual average of 4% before 2029; if global disturbances occur, it may drop to as low as 3%, but if productivity improvements accelerate, it could reach 6%. Based on a 4% growth rate, the total market size is expected to reach 3.0 trillion USD by 2029.

1.1 Global Payment Trends

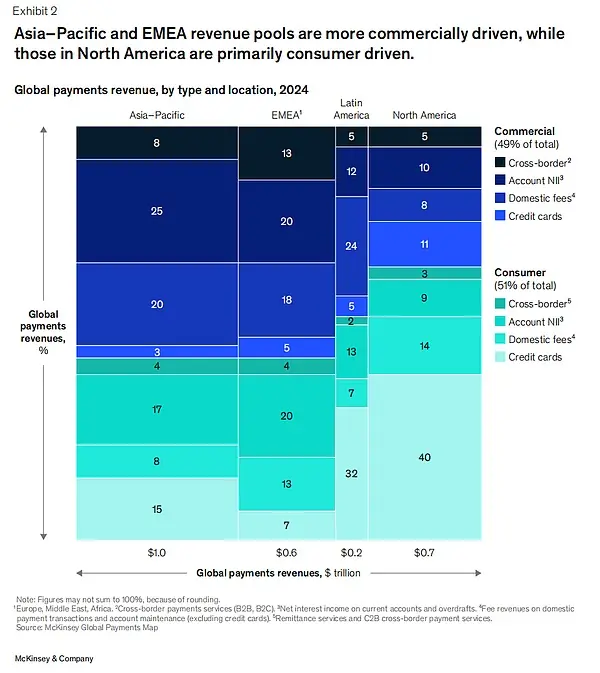

Overall, global payment revenue is almost evenly split between the consumer and business sectors, but there are significant differences in composition across regions.

- North America tends to favor consumer payments, as credit cards are both the primary payment tool and a means of borrowing, reflecting the maturity of the consumer credit market and the strength of card loyalty programs.

- The Asia-Pacific region tends to focus on business, with 25% of revenue coming from net interest income (NII) from commercial accounts, highlighting the company's strong banking relationships and the dependence of rapidly growing economies on deposit interest.

- The EMEA structure is the most diverse: 20% of revenue comes from commercial account NII related to trade and treasury activities, and 20% comes from consumer account NII, benefiting from a higher savings base in Europe.

- Similar to North America, Latin America also leans towards consumers, with consumer credit card income accounting for 32% of total income, reflecting the importance of revolving credit and consumers' reliance on installment payments.

1.2 Payment Development Trends under Income Structure

The global cash usage rate continues to decline, with its share of total payments dropping from 50% in 2023 to 46%. Account-to-account (A2A) payments are becoming increasingly popular, especially transactions completed through digital wallets, which currently account for about 30% of total global point of sale (POS) transactions, with markets like India, Brazil, and Nigeria leading the way.

As transaction volumes shift towards low-yield avenues such as instant payments, the difficulty of monetization increases; this issue is particularly prominent in markets with strict regulations on interchange fees and processing fees. We expect that new economic and charging models will gradually emerge in the A2A sector, possibly following India's approach—where banks have started charging unified payment interface (UPI) merchant transaction fees to payment aggregators.

In business-to-business (B2B) payments, digitization has been fully rolled out, but it mainly focuses on low-profit channels such as bank transfers and instant payments. To capture value, companies (especially those centered around software) are investing in value-added services, including invoice automation, reconciliation, and working capital tools; these services are particularly important for small and medium-sized enterprises and industries like healthcare that still rely on manual processes.

Finally, new technologies continue to bring opportunities and threats. From tokenized currencies and digital currencies to AI-based anti-fraud and liquidity management, innovations have enhanced security, efficiency, and reach. However, the level of adoption varies. Regulatory uncertainty, infrastructure gaps, and inconsistent technical standards have led to progress occurring only in isolated areas.

2. The Three Forces Reshaping Global Payments

There are three structural forces that could fundamentally change the way funds flow between individuals, businesses, and intermediaries:

- The payment system is becoming increasingly fragmented and regionalized;

- The large-scale application of digital assets in payment scenarios;

- The transformative potential brought by artificial intelligence.

2.1 Fragmentation and Regionalization of Payment Patterns

The global payment ecosystem is entering an unprecedentedly complex phase, set against the backdrop of the high interconnection of goods, services, and people. Over the past 30 years, globalization has ensured the smooth flow of cross-border funds. However, geopolitical events have prompted some countries and regions to reduce their reliance on global standards and systems. For example, sanctions against Russia have excluded it from international card organizations, leading it to rely on the Mir card for domestic transactions and to partner with China UnionPay to meet international demand. Some countries and regions are promoting “payment sovereignty” to reduce dependence on global intermediaries; the European Central Bank is vigorously promoting a large-scale system centered on Europe.

At the same time, technological advancements have accelerated the growth of localized and regional payment systems. The construction of instant payment infrastructure is particularly crucial, as it fosters an excellent user experience (typical examples include Brazil's Pix, Spain's Bizum, and India's UPI). The increasing interoperability among domestic instant payment systems provides new pathways for cross-border payments, beyond traditional standards. Notably, Pix's internationalization in Latin America and the expansion of India's National Payments Corporation (NPCI) into the Middle East and Southeast Asia are prominent and rapidly developing cases. Meanwhile, the rapid adoption of stablecoins is also creating a new channel distinct from traditional payment rails.

These geopolitical and technological changes are reshaping the payment landscape, bringing about stronger regionalization and diversification. It is increasingly unlikely to return to a completely globalized payment system as it was five years ago, as the forces driving fragmentation have already been set in motion. However, many alternative payment systems encounter obstacles in their expansion process: poor user experience, unclear value proposition, governance flaws, and the lack of supporting legislation in key markets are issues that continue to arise; in certain scenarios, traditional legacy systems demonstrate sufficient resilience, even circumventing or defeating new solutions.

Therefore, the payment landscape is evolving towards two outcomes that are even more fragmented than now: one is a diversified ecosystem of 'multi-track + global passkeys'; the other is a divided world of 'increased localization + declining global standards'.

Scenario A: Multitrack Ecology with “Global Access Key”

In a more optimistic scenario, geopolitical tensions stabilize or ease, payment standards remain strong, and serve various payment scenarios and customer types like a “global universal key.” The service scope can be broad or narrow—from online shopping to a range of value-added services; the service depth can be deep or shallow—from cross-border financial solutions targeting a specific industry to simple remittances aimed at the general public.

In this environment, all parties involved must face multiple challenges: not only to monitor and regulate the flow of funds traversing various tracks but also to confront the significant differences in economic benefits between different use cases and systems, and to complete the technical integration between systems. This may give rise to a batch of “integrators” and “aggregators” that can seamlessly stitch together multiple payment systems. In this scenario, although payment systems are more fragmented than they are now, they can foster innovation and specialization, allowing for diverse solutions to coexist and meet the needs of niche markets.

Scenario B: Fragmented Upgrades, Global Standards Eroded

If global trade and commerce continue to face significant challenges, with escalating geopolitical tensions, countries may increasingly rely on local and regional alliances, gradually distancing themselves from the global flow of goods, services, and people. The backdrop for this scenario is the failure to construct a framework that allows for the coexistence of the “global system” and the “local system.” At that time, payment systems will inevitably trend towards regionalization.

Countries and regions will prioritize resilience and self-sufficiency, leading to the emergence of more bilateral agreements, intermediary currencies, and alternative payment systems, gradually distancing themselves from global standards. Over time, regional systems and payment tools will dominate in various use cases, fundamentally reshaping the financial landscape. International connectivity will become more challenging, profoundly impacting payment technology stacks, especially for institutions with multinational and globalized layouts. This may accelerate the adoption of stablecoins and tokenized currencies.

Although the international connectivity in the first scenario is smoother, both scenarios imply that the previously unified global payment landscape will become further fragmented and complex, with solutions becoming more localized. For businesses and financial institutions, adapting to this new reality requires flexibility, innovation, and a deep understanding of the forces driving the flow of funds.

2.2 The Accelerated Adoption of Stablecoins and Tokenized Money

Stablecoins and tokenized currencies are increasingly becoming an important part of the financial system, although they have yet to cross the critical threshold of widespread adoption. The industry scale is expanding rapidly—stablecoin issuance has doubled since the beginning of 2024—but their share remains limited in the total daily payment volume amounting to trillions of dollars globally: the current average daily trading volume is around 30 billion dollars.

Multiple signals indicate that stablecoins are approaching a “breakthrough” moment. The primary factor is the increasingly clear regulatory rules: the United States (recently passed the GENIUS Act), the European Union, the United Kingdom, Hong Kong, and Japan have all introduced or improved regulatory frameworks, clearly defining key requirements such as licensing, reserve management, anti-money laundering, and customer due diligence. Whether the cross-regional framework can align will determine whether cross-border stablecoin business can proceed; the clarification of rules itself will lower the entry threshold, especially benefiting traditional financial institutions and enhancing market confidence in stablecoins.

The technical infrastructure is also rapidly upgrading: by migrating transaction processing from the mainnet to more scalable Layer 2 solutions and adopting more efficient consensus protocols, throughput continues to improve; user-facing digital wallets and bank-grade custody solutions are becoming increasingly reliable and accessible; advanced on-chain analytics tools enhance security and compliance capabilities.

The more persuasive driving force comes from the demand in real scenarios. Although stablecoins initially gained popularity only in niche areas such as cryptocurrency asset trading settlements, their potential has been recognized in broader use cases: tokenized deposits allow customers to earn interest within the day and be available at any time; stablecoins can provide “7×24” real-time settlements, becoming an alternative to traditional agency networks; in regions with significant local currency fluctuations, stablecoins anchored to major global currencies can help consumers hedge against inflation. Institutional-level applications are also beginning to emerge, such as B2B treasury management, supply chain financing, repurchase agreements, and so on. Moreover, the “Programmability” feature of stablecoins can give rise to new scenarios, including solving custody challenges and restricting government benefits to specific categories of consumption.

In the past 18 months, multiple high-profile announcements, collaborations, and mergers have indicated that the industry is making every effort to capture the value of tokenized assets. However, widespread adoption also brings risks that must be managed prudently. Although major market regulations are becoming clearer, there is still a lack of a unified and coherent regulatory framework globally, which could lead to uncertainty and even market disruptions. If a certain issuer has insufficient reserves, stablecoins may lose their peg, leading to a collapse of trust; if a leading stablecoin fails, the shockwaves could spread to the broader financial system.

Moreover, to truly popularize stablecoins, end users need to change their temporary mindset of “just being a bridge for fiat currency exchange” and be willing to hold them long-term. Once the majority of customers retain their funds in stablecoins, the funding sources and income models of traditional banks will be disrupted.

The rise of stablecoins is also in sync with the trend of “multi-track payments”—for example, merchant acquiring institutions simultaneously support card swiping, A2A transfers, and stablecoins in a unified solution. Leading companies have taken important steps: PayPal now accepts multiple digital asset payments; Coinbase has launched a debit card linked to stablecoins, and a credit card product is also forthcoming. Other service providers that wish to meet customer demands related to stablecoins must make a choice: to build capabilities in-house or to collaborate with aggregators and integrators.

III. The Path Forward for Payment Participants

As the global payment landscape is reshaped into a mosaic interwoven with diverse tracks, digital assets, and intelligent AI agents, various possible paths will emerge for industry participants.

This chapter breaks down the key choices faced by payment institutions, merchants, platform providers, and solution experts, exploring how each segment positions itself, continues to innovate, and captures value in an increasingly “Decentralization, Programmability, Real-time” environment.

3.1 Payment Providers: Competing for Brand and Trust

As AI agents begin to dominate more consumer journeys, traditional competitive strategies relying on “product differentiation + user experience” may become ineffective. Convenience and personalization will become the basic thresholds, and the main battleground will shift to “brand trust and relationships” – whoever can control the interaction interface (whether direct or embedded) will be able to influence consumer decisions in a highly sticky and irreplaceable way.

At the same time, new rails, stablecoins, and programmable currencies will rewrite the economic model of consumer payments. Smart agents will optimize “when and how to pay” for consumers, potentially squeezing the revenue from exchange fees and interest rate spreads, putting pressure on local/regional players' growth, and impacting the dominance of global giants. Large institutions and solution experts that have long relied on “settlement, credit, and liquidity inefficiencies” for profit need to reshape their value propositions to avoid being “disintermediated” by smaller players and clients.

The ultimate winners will be those players who create smart, embedded, secure, and emotionally resonant experiences around the “agent-based journey”: not only able to anticipate needs and “translate” complex technologies into intuitive experiences but also possessing explainability and deeply aligning with brand trust commitments.

The emphasis placed by various countries on “payment sovereignty” and local solutions will benefit local/regional players while limiting global players. Local institutions can become the “trust anchors” of the local ecosystem (instant payment, identity layer, central bank digital currency platform), promoting interoperability, connecting networks, and complying with local policies; regional players (such as Europe’s Wero and Brazil’s Pix) can lead economic blocks by establishing cross-border payment, digital identity, and data governance rules. Global players may turn to more flexible and open architectures to accommodate legal differences; in some markets, partnerships with emerging regional companies may also be considered to bridge brand recognition and trust gaps.

3.2 Merchant: Retain customers with payment methods

Consumers expect rising tides to lift all boats, and merchants need to provide a seamless, scalable experience that covers diverse payment methods, channels, and compliance requirements. AI agents are increasingly taking control of the demand side, forcing merchants to acquire customers in new ways and achieve new standards in “payment orchestration, smart checkout, and personalized offers.”

Merchant payment service providers must upgrade from “support acquiring” to “providing autonomous payment infrastructure”: features such as smart routing, real-time settlement, automatic compliance, and dynamic currency optimization will become the default configuration. The greatest opportunity lies in creating an “empowering business layer”, helping merchants acquire, convert, and retain customers across multiple channels and regions. This layer includes acquiring services and also promotes further integration of merchant SaaS and payments. First movers can turn the complexity of “regional tracks + tokenized currency” into a competitive advantage, achieved through programmable APIs and embedded services.

3.3 platform provider: be an ecosystem enabler

A “large multi-product” platform that spans the value chain and multiple payment rails, equipped with the natural advantages of AI and Programmability, can help traditional clients like banks accelerate innovation. Its business breadth allows it to orchestrate the complete end-customer journey and act as the “control layer” for AI agents and programmable finance. Abundant data resources further fuel large-scale decision-making and personalization.

However, many platforms, while having a large user base, are lacking in specific functionalities when compared to experts. Blindly adding comprehensive new features may further widen the gap with professional players, prompting customers to seek the “best variety” solutions externally.

Therefore, the platform needs to clarify strategic priorities, determine resource allocation, and effectively implement new technologies for different customer groups (banks, merchants, enterprises, individuals). With research and development and a developer ecosystem, large platforms can continuously maintain innovation leadership in specific service areas.

3.4 Solution Expert: Unlocking Subdivided Value

Professional participants—such as cross-border payment experts, single-track acquiring service providers, and payable/receivable automation vendors—face both opportunities and risks. The fragmentation of payment systems has given rise to numerous edge cases and segmented niches, which are well-suited for “point solutions” to cultivate; however, the rise of agency-style workflows and Programmability of currency may also commoditize those lacking unique intelligence, depth, or leverage.

Therefore, the key to victory for experts will lie in: targeting complex use cases rich in intellectual added value and deeply embedding their capabilities into the platform and agency ecosystem; at the same time, they need to adapt to regional differences while retaining the ability to orchestrate larger workflows across tracks and links.

Specific path example:

- Transform the cross-border payment system into an “embedded engine” that allows platforms or agents to dynamically choose routes based on real-time rates, foreign exchange fluctuations, and arrival time efficiency, while deeply integrating with Programmability wallets to achieve optimal cash movement across multiple currencies and channels.

- Upgrade the KYC/KYB rule engine to a “Programmable Trust Layer,” allowing the agent system to adjust the access process in real-time based on transaction type, jurisdiction, and customer profile, achieving intelligent and differentiated onboarding.

4. Six Major Strategies to Thrive in the Next Payment Era

In the face of the new era of “intelligent, programmable, and interconnected” payments, participants can adopt the following six core strategies to seize new value.

- With “smart simplicity” as the design purpose

As consumers and businesses increasingly rely on agents and automation, the key to trust and widespread adoption lies in “keeping the complexity to ourselves and handing the simplicity to the customers.” It is essential to embed simplicity, transparency, and personalization within the core of the product, allowing users to maintain complete control over their funds through effortless interactions.

- Treat interoperability as infrastructure

Cross-border and multi-track trading will become the norm for the foreseeable future. The ability to bridge different asset types, jurisdictions, and compliance systems in real-time is no longer a differentiating selling point but rather an “entry ticket.” Participants need to build resilient infrastructure that natively supports these demands.

- Push Intelligence to the Edge

Decisions must be made at the moment a transaction occurs, within the agent, and in the programmable contract. Routing logic, fraud detection, and liquidity management should be directly embedded in software agents, APIs, and workflows, rather than relying on centralized batch processing or manual approval.

- Make Compliance Programmable

In the face of increasingly fragmented regulations, only players who can write “local compliance” into their code can scale up. A modular policy engine and regional logic will replace manual processes and hard-coded rulebooks, achieving “one-click adaptation” for global compliance.

- Integrate into the ecosystem, rather than confront the ecosystem

In a modular, programmable world, victory belongs to the layers that are “viewed as the cornerstone by others”: whether it be intelligence, trust, liquidity, or connectivity. Independent moats will be eroded, and roles embedded in a larger ecosystem will endure.

- Build trust “upstream”

When AI and automation become the initiators of transactions, businesses need to incorporate transparency, explainability, and error tracing into the system, so that both users and regulators can know at any time “what happened and why it happened,” thereby winning trust “before the transaction”.

5. Summary

The payment industry is not only adapting to new technologies or market changes but is fundamentally reshaping its infrastructure in response to geopolitical forces, emerging digital paradigms, and the accelerating pace of artificial intelligence. In this fragmented yet interconnected future, the key to success lies in the commitment to achieving seamless interoperability between diverse payment rails and proactively embracing complexity.

In the coming years, players who can turn challenges into opportunities and carve out new paths in a world where agility, innovation, and trust become the most valuable assets will reap substantial rewards.