Author: Nancy, PANews

After the implementation of the U.S. “GENIUS Act” in July, Circle, known as the “first stock of stablecoins”, recently released its first financial report following the new policy. Although revenue slightly exceeded expectations, stock prices still fell due to a single profit structure, low profit quality, combined with downward pressure on interest rates and the impending unlocking of a large number of shares, raising short-term concerns in the market. However, Circle is actively creating a second growth curve through new business layouts such as the Arc public chain and the USYC tokenized currency fund, exploring diversified income sources to reduce dependence on interest rates.

USDC supports the revenue banner, and distribution costs further erode profit margins.

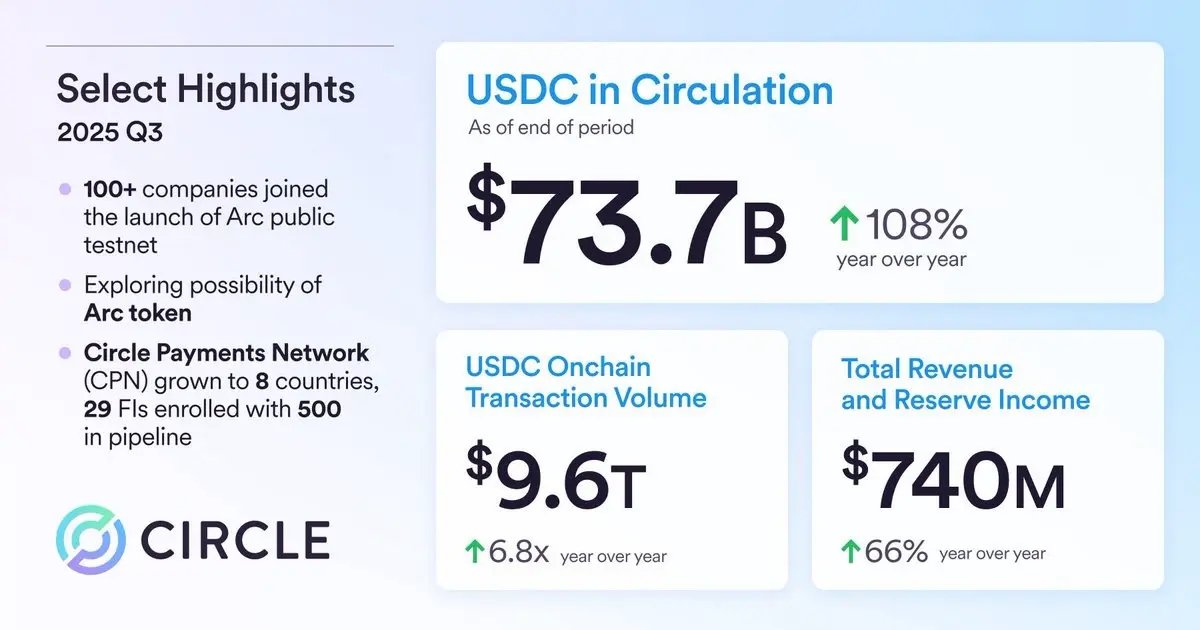

Circle's latest financial report shows that total revenue for the quarter is close to $740 million, of which USDC reserve revenue reached $711 million, a year-on-year increase of 60%, accounting for 96.1% of total revenue (slightly down from the same period last year), making it Circle's absolute core revenue source. The growth in this revenue is mainly attributed to the market growth of USDC, with a circulation volume reaching $73.7 billion and an average circulation volume year-on-year increase of 97%, while market share rose from about 22.6% to 29%. The official forecast for USDC's long-term compound growth rate is 40%, indicating a certain sustainability of revenue growth.

In contrast, the contribution of other income remains less than 4% (approximately $28.51 million), mainly from subscriptions, APIs, payment networks, and other businesses, but has increased more than 52 times year-on-year. Circle has also raised its full-year expectations to between $9 million and $100 million. However, in the short term, this type of income still has limited impact on overall revenue, indicating that Circle's revenue structure remains highly singular and is very sensitive to interest rate changes. The market generally expects the Federal Reserve to cut interest rates by another 25 basis points at its December meeting, while Circle's reserve return rate has already fallen by 96 basis points to 4.15% this quarter. This means that if interest rates continue to decline, Circle's interest income may be further compressed, exerting significant pressure on overall profitability.

In terms of profit, Circle achieved a net profit of $214 million this quarter, successfully reversing the substantial loss from the second quarter caused by IPO-related expenses, with a year-on-year increase of 202%. However, if we exclude the $56.21 million gain from the decrease in the fair value of convertible debt and the $61.29 million income tax benefit (from stock compensation, R&D tax credits, and the impact of new tax laws), the actual operating profit is about $96.5 million. In other words, the profit generated from Circle's main business only accounted for approximately 45.1% of the total net profit, significantly reducing its profitability.

It is worth noting that the rapid growth of USDC is inseparable from Circle's “money-sprinkling” distribution cooperation model, which has also become a “stumbling block” to its performance. In this quarter, the amount Circle spent on distribution and trading costs reached 447 million USD, accounting for about 62.8% of reserve income, compared to 42% in the same period of 2024; the official explanation states that the increase in distribution costs is mainly due to the increase in USDC circulation balance and the average holdings of Coinbase, as well as other strategic partnerships. Circle's retained income in the third quarter accounted for 37% of reserve income, down from 42% in the same period last year. This indicates that the growth rate of Circle's distribution costs is higher than that of its income. In response to the decline in RLDC (revenue minus distribution costs), the official stated in the earnings call that its priority partner distribution incentives and market reward dynamics have led to increased costs, but economies of scale will improve leverage, with an expected RLDC gross margin of approximately 38% for the year.

On the other hand, Circle's operating expenses for the third quarter were $211 million, a year-on-year increase of 70%, mainly due to increased compensation (including $59.08 million in stock-based compensation) and rising IT, management, and R&D expenses. Circle also raised its annual adjusted operating expense expectation to between $495 million and $510 million, citing increased investment in platform capability development and global partner expansion.

Overall, Circle continues to maintain rapid growth in its USDC reserve business, but profit margins are constrained, and diversified income has yet to form a strong support. This has raised market concerns, leading to CRCL dropping to $86.3, currently down approximately 12.2%, and a decline of about 64.1% from its historical high. Meanwhile, as Circle is set to face a large-scale unlock on November 14, the locked shares disclosed in the prospectus will be available for sale after 180 days or on the second trading day after the public disclosure of the third-quarter financial report (whichever comes first), potentially increasing selling pressure and further exacerbating stock price volatility.

Exploring the Second Growth Curve: Circle's Three New Moves

As more and more new stablecoin players enter the market, competition in the field is becoming increasingly intense. In this trend, the market's distribution capability and ecological expansion capacity have become new core competitive dimensions, no longer relying solely on first-mover advantage or compliance. To this end, Circle is continuously expanding its cooperative ecosystem around its core business, USDC.

According to the financial report, since the second quarter, Circle has announced several key partnerships and collaborations related to USDC, including Brex, Deutsche Börse Group, Finastra, Fireblocks, Hyperliquid, Kraken, Itaú Unibanco, and Visa, covering areas such as corporate payments, traditional finance, custody, DeFi, and cross-border payments, accelerating the deep penetration from crypto-native to mainstream financial infrastructure.

At the same time, in order to quickly get rid of the risk of being too dependent on the issuance of USDC for its profit model, Circle is accelerating the diversification of its revenue structure.

On one hand, Circle is venturing into the foundational infrastructure sector. In August this year, the company announced the launch of its self-developed layer one blockchain, Arc. On October 28th, the Arc test network officially went live, attracting over a hundred institutions to participate in the testing, covering various industries such as capital markets, banking, asset management, insurance, payments, and technology. Circle aims to provide programmable financial infrastructure for developers and enterprises, facilitating the scaling of on-chain economic activities. At the same time, Circle plans to explore the issuance of Arc's native tokens to incentivize network participation, promote the implementation of ecological applications, and build a long-term sustainable network economic model.

On the other hand, Circle continues to deepen its layout in the payment and settlement field. In May of this year, the company launched the cross-border payment network Circle Payments Network (CPN), which currently covers 8 countries, with 29 financial institutions officially connected, another 55 in the review stage, and 500 still waiting to connect. As of November 7, 2025, the annualized transaction volume of CPN in the past 30 days has reached approximately $3.4 billion.

In addition, asset tokenization has also become a key area of exploration. Circle launched the tokenized money market fund USYC in the middle of the year, aimed at providing liquid, tradable, and stable-yield digital asset tools for institutions and high-net-worth investors. From June 30 to November 8, 2025, the scale of USYC grew by over 200%, reaching approximately $1 billion.

Overall, although Circle's business continues to show steady growth, short-term profitability is under pressure. The company is actively expanding its business boundaries beyond stablecoins, accelerating its transformation from a stablecoin issuer to a provider of on-chain financial infrastructure. However, this transformation is not easy in the highly competitive stablecoin space.