Author: Azuma, Odaily

The market is sluggish, and investors are on high alert.

In the past week, the frequent large transfers of BTC and ETH from BlackRock to Coinbase have attracted the attention of many investors. When many see the transfer activity, they immediately interpret it as a signal for a market crash and try to analyze the short-term market based on that signal. But is this methodology really reliable?

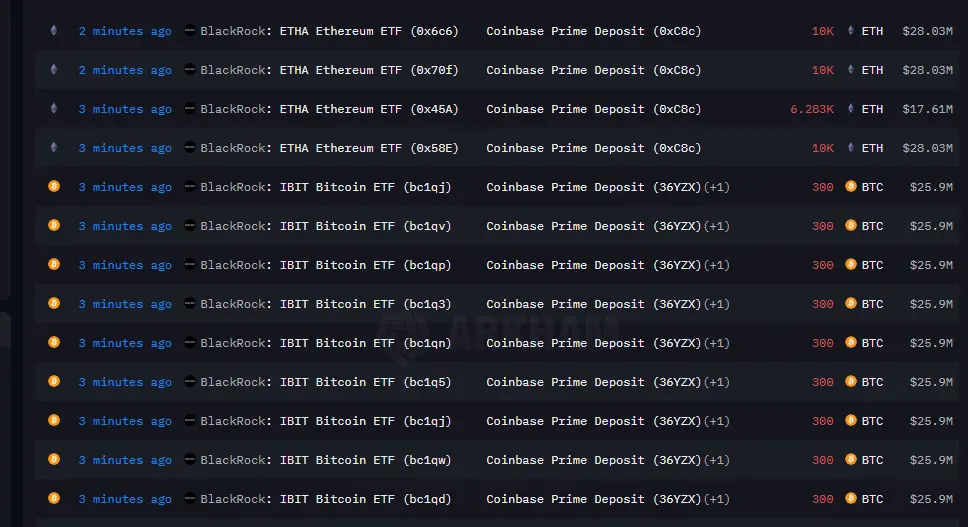

Odaily Note: BlackRock transferred a large amount of BTC and ETH to Coinbase again last night.

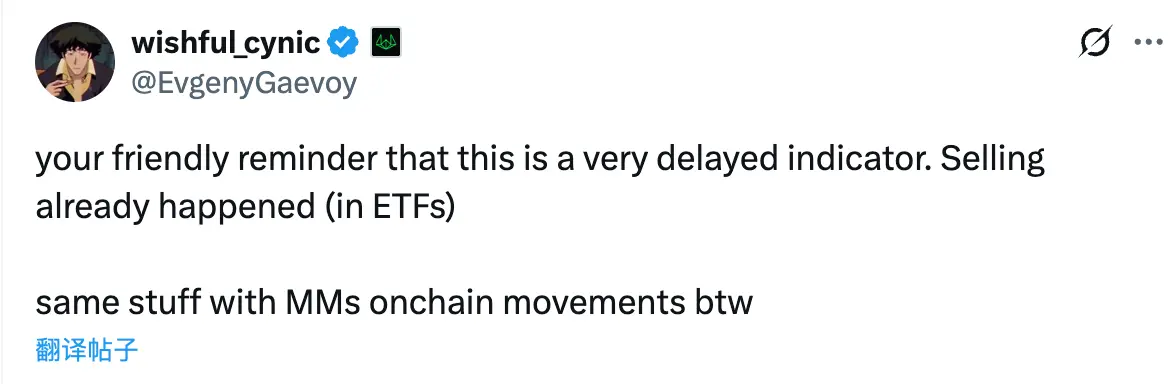

In the early morning of November 25, Wintermute founder Evgeny Gaevoy commented on this matter on X, stating: “This (the large transfer by BlackRock) is actually a very lagging indicator. The sell-off has already occurred in the ETF. The on-chain transfers by market makers are often the same situation.”

How should we interpret Evgeny's words? If there is a delay in the transfer, then when exactly does the real sell-off occur?

First of all, it is important to clarify that the so-called BlackRock large transfers refer to the cryptocurrency transfers from the reserve addresses of BlackRock's spot Bitcoin ETF (IBIT) and spot Ethereum ETF (ETHA) to the Coinbase Prime custody address.

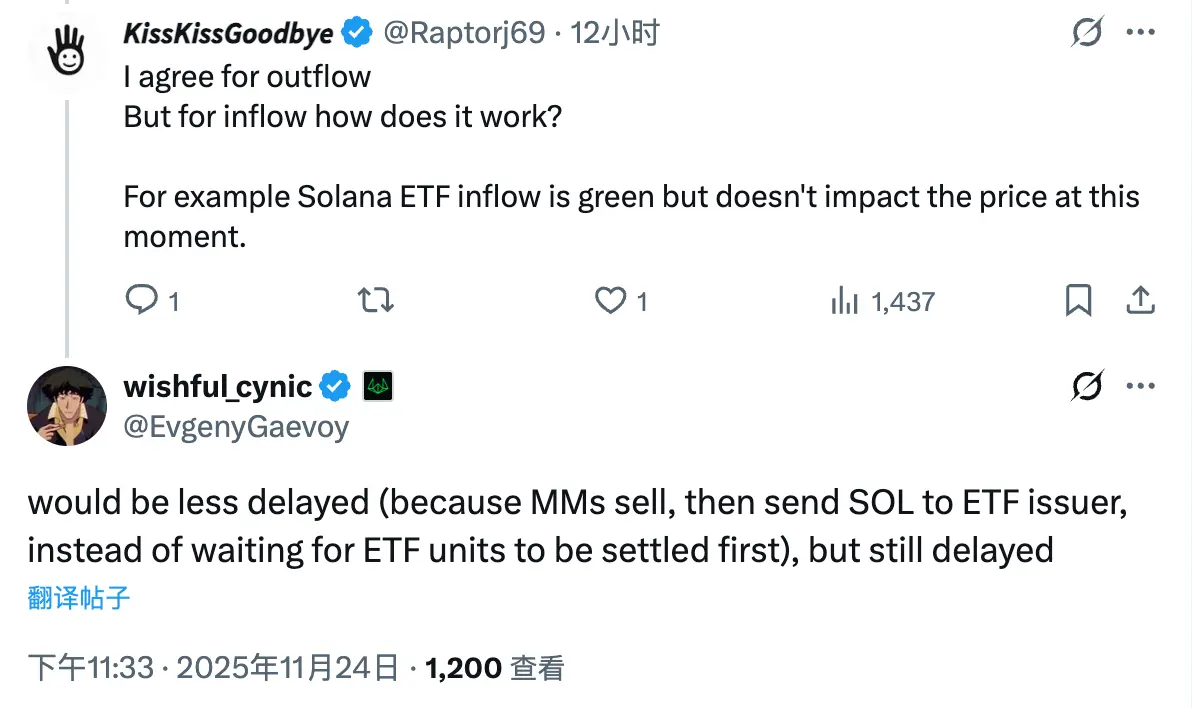

According to Evgeny's supplementary introduction when answering netizens' questions, this actually occurs at a time when the ETF experiences net outflows, and large market makers engage in market making and hedging around the ETF.

Specifically, market makers will buy shares from ETF sellers, then submit a redemption request to BlackRock to exchange the ETF shares for BTC (which usually has a 1-day delay). There is no selling pressure in the subsequent stages because market makers have already completed the hedging (selling) operation simultaneously when purchasing the ETF.

In other words, the real selling pressure does not occur when retail investors see on-chain transfers, but rather when market makers are taking on ETF sell orders (which is a buy for market makers) while simultaneously selling in the external market for hedging. Since redemption circulation typically has a 1-day delay, the actual selling pressure may occur 1 day earlier.

To add a point, the above describes the market making process when the ETF experiences net outflows. Conversely, when the ETF experiences net inflows, market makers will sell the ETF to buyers while buying cryptocurrencies (such as SOL, which is currently experiencing net inflows) and sending them to the ETF issuer. Since there is no redemption time limit in this case, the lag time will be shortened, but there will still be some degree of delay.

In summary, the so-called “BlackRock large transfer” is actually just a settlement phase in the standard ETF operation process, and the selling pressure it represents generally appears before the transfer, not after. Relevant data will be presented more clearly and comprehensively in the daily monitoring of ETF inflows and outflows, and there is no need to reinterpret it as an additional bearish signal, which could lead to unnecessary panic.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

STRC Stock Surge: How Much Bitcoin Can Saylor Buy?

Michael Saylor’s Strategy, linked to MSTR (EXCHANGE: MSTR), continues to funnel capital into Bitcoin (CRYPTO: BTC) via its STRC (EXCHANGE: STRC) stock program, with the potential for further purchases in the coming weeks. The publicly traded vehicle has built a BTC position that some estimates

CryptoBreaking12m ago

Bitcoin Correction Halts Institutional Demand as ETFs Witness $348.83 Million Withdrawals - U.Today

Bitcoin ETFs experienced a significant withdrawal of $348 million amid declining institutional demand, reflecting a bearish sentiment in the market. Despite these outflows, BlackRock's ETF maintained its dominance.

UToday1h ago

XRP Price Prediction: Ripple Trades Below Key Moving Averages as the 20 Millionth Bitcoin Approaches and Pepeto Targets 267x Returns

Grayscale confirmed the 20 millionth Bitcoin will be mined in March 2026, leaving only 1 million BTC left to ever exist, and when 95% of a finite asset is already circulating, the scarcity narrative reshapes how every trader thinks about value.

The xrp price prediction shows Ripple at $1.37 b

CaptainAltcoin2h ago

The Origin Story of Sunny Lu: From a 100 BTC Scam to Building VeChain

VeChain’s Sunny Lu got into crypto after losing $300 on an unsuccessful 100 BTC purchase on Taobao, which led him to research Bitcoin.

Later, Lu used blockchain to track supply chains and launched VeChain in 2015 to target verification and enterprise applications.

The crypto journey of Sunny

CryptoNewsFlash3h ago