“Trump Account”: A National Bet Reshaping American Wealth and the Future

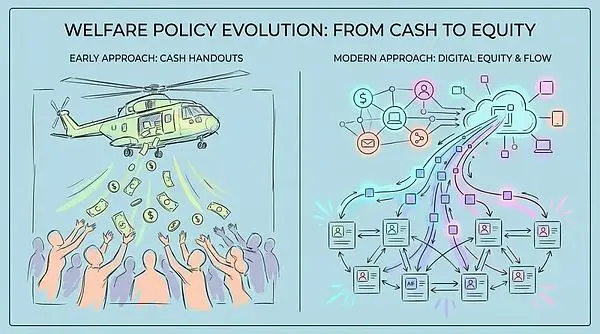

In the ever-changing global economic landscape, a program called the “Trump Account” is quietly emerging. It’s more than just a welfare policy; it’s a grand social experiment that deeply alters our understanding of wealth, inequality, and even the future of the nation. It represents a shift from traditional “helicopter money” to disruptive “helicopter equity,” closely tying the economic fate of the next generation to the performance of capital markets.

If this policy is effectively implemented, it will continuously provide liquidity to the U.S. stock market from now until 18 years later. In the near term, it’s a definite positive for the market.

From “Helicopter Money” to “Helicopter Equity”

Over the past half-century, government intervention in the economy has been commonplace. From Keynesian demand-side management to quantitative easing during financial crises, the federal government has often stimulated consumption and boosted aggregate demand by directly handing out cash to the public. The 2008 tax rebate checks and the 2020 pandemic relief payments both followed this logic. However, the emergence of the “Trump Account” breaks this traditional thinking, introducing the entirely new concept of “helicopter equity.”

The “Trump Account” is no longer content with solving immediate crises—its ambitions are bigger. It seeks, through mandatory asset lock-in and long-term compounding effects, to directly anchor the economic fate of our next generation to the performance of the capital markets.

Imagine every newborn U.S. citizen receiving a $1,000 “seed fund” from the federal government. This money isn’t for immediate consumption; it’s forcibly invested in the stock market and can’t be accessed by anyone until the beneficiary reaches adulthood. In addition, the Dell family has generously donated $625 million to provide equity-form “seed funds” for children born before this program. This marks the transformation of the “ownership society” concept from a political slogan into a concrete financial infrastructure.

Policy Structure and Operational Mechanism of the “Trump Account”

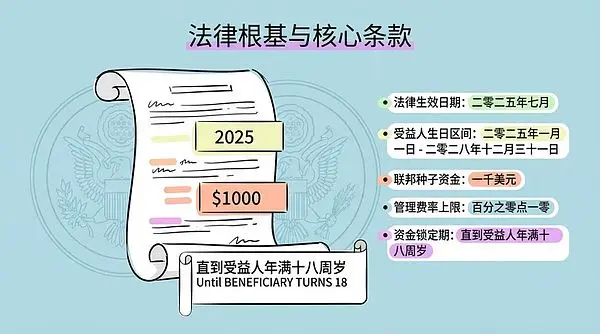

The “Trump Account” is legally based on a tax and spending bill effective July 2025. The bill designs a tax-advantaged investment tool, similar to a Roth IRA, but with stricter restrictions on beneficiary age and fund withdrawal.

Key provisions include:

- Beneficiary Scope: Every U.S. newborn with a Social Security number born between January 1, 2025, and December 31, 2028.

- Federal Seed Funding: A one-time deposit of $1,000 by the U.S. Treasury.

- Management and Fees: Funds managed by the Treasury, operations handled by private financial institutions, with an annual management fee cap of 0.10%.

- Lock-in Period: Funds are mandatorily locked until the beneficiary turns 18, unless the beneficiary dies or suffers severe disability. This 18-year lock-in is designed to maximize compounding and ensure the funds’ “capital” nature isn’t diluted.

However, the bill has an obvious generational gap, covering only newborns after 2025 and lacking federal funding for children born before then. This may lead to children of different ages within one family facing different national treatment. It was at this point that Michael and Susan Dell’s massive donation filled the gap, setting a precedent for private capital directly intervening in national welfare distribution.

Algorithmic Allocation and Challenges of the Dell Plan

The Dell donation is not universal but targeted through precise geographic and economic algorithms. To receive the $250 “Dell seed fund,” children must:

- Be 10 years old or younger (i.e., born before January 1, 2025).

- Reside in a ZIP code area where the median household income is below $150,000.

- Have not received the federal $1,000 grant.

This forms a three-tiered “helicopter equity” system:

- Tier 1: Newborns from 2025–2028, $1,000 from the U.S. Treasury, universal.

- Tier 2: Existing children under 10, $250 from the Dell Foundation, with household income restrictions based on ZIP code.

- Tier 3: Children over 10 or in high-income areas, no funding.

Dell’s involvement marks a major shift in welfare policy logic—from tax adjustment to reliance on the “philanthropic capital” of super-rich individuals. While this ZIP-code-based algorithmic allocation aims for precision, it also brings new fairness issues, such as “gentrification misjudgments” and “high-cost traps,” potentially excluding some low-income families.

Ongoing Contributions and the Super IRA

The long-term power of the “Trump Account” lies in its ability to accept ongoing contributions. It allows up to $5,000 in additional annual contributions, adjusted for inflation after 2027. Funding sources are diversified:

- Families can contribute post-tax income, with investment gains enjoying tax deferral.

- Employers can contribute up to $2,500 per year to employees’ children’s accounts, not counted as employee taxable income, creating a new tax-free compensation benefit.

- Local governments and other charities can also contribute, not counting toward the annual cap.

This structure is essentially a “super IRA” for minors. When the beneficiary turns 18, the account converts to a traditional IRA, with funds available for higher education, first-time home purchases, or entrepreneurship. Withdrawals for non-qualified purposes are subject to income tax and possibly penalties. The dual mechanism of “lock-in” and “tax incentives” enforces long-term capital accumulation.

Mandatory Investment and Market Impact: A Bet on Asset Inflation

The most striking feature of the “Trump Account” is its mandatory investment directive: the bill requires funds to be invested in index funds tracking the U.S. stock market, such as the S&P 500. This ties the future wealth of millions of American children to Wall Street’s performance and introduces a massive, price-insensitive passive bid into the market.

The “inelastic market hypothesis” suggests that stock market demand elasticity is much lower than traditionally assumed. Every dollar flowing into the market may boost total market cap by five dollars or more.

Estimates suggest that with about 3.5 million U.S. newborns each year, federal seed funding will inject $3.5 billion into the market annually. Adding in Dell’s donations and millions of families’ contributions, this creates a sustained, massive capital flow. These funds are indifferent to valuations and are driven by law and birth rates—regardless of booms or busts, money will keep buying S&P 500 stocks.

This mechanism may intensify the “head effect” in the market, channeling disproportionate new money into giants like Apple, Microsoft, and Nvidia. Academic studies confirm that passive investing significantly inflates large-cap stock prices, often decoupled from fundamentals. Thus, the “Trump Account” may inadvertently become a booster for giant stock prices, strengthening market concentration.

The “Trump Account” is also a bet on asset inflation. “Helicopter money” triggers consumer inflation, while “helicopter equity” acts directly on asset prices. Critics argue the policy essentially subsidizes asset holders, artificially boosting stock demand and raising prices when supply is constant or even shrinking.

This creates a self-reinforcing feedback loop: federal and family savings are forced to buy stocks, lifting prices; corporate executives, seeing rising stock prices, prefer buybacks over dividends to reward shareholders; buybacks reduce float, and paired with ongoing account demand, push prices even higher.

This is essentially a national wager: it bets that this financial engineering can keep creating paper wealth and won’t suffer a disastrous valuation reset at some future point.

Beneficiary Sequence Risk and New Challenges in Philanthropic Governance

For beneficiaries, the greatest risk in this bet is “sequence risk”. Unlike Singapore’s CPF, which provides a guaranteed rate, the “Trump Account” transfers all market risk to individuals. Imagine the “2043 Problem”: a child born in 2025 comes of age in 2043, only to face a market crash that instantly shrinks their “national dowry.” The current bill does not specify any automatic glide-path mechanism like a target-date fund, exposing beneficiaries to extreme tail risks.

The Dell family’s involvement is not just a donation, but a new model of “philanthropic governance”. By setting a $150,000 median income ZIP-code threshold, the Dell Foundation is effectively performing quasi-governmental functions, deciding who qualifies for welfare. While big data governance is precise, it also faces issues like “gentrification misjudgment” and “high-cost traps.”

When national welfare policy relies on private philanthropists to fill gaps, the nature of the social contract changes. Welfare is no longer a statutory right based on citizenship but becomes a handout dependent on the goodwill of the wealthy. This may solve funding issues in the short term, but could weaken the stability and predictability of public welfare systems in the long run.

Lessons from International Experience: UK, Singapore, and “Baby Bonds”

To better understand the pros and cons of the “Trump Account,” we can compare it to global asset-based welfare policies.

- UK Children’s Trust Fund Lessons: From 2002-2011, the UK ran a Children’s Trust Fund program that automatically opened accounts, yet over 758,000 accounts were “unclaimed” when children turned 18, involving £1.4 billion. This warns that the “Trump Account’s” opt-in mechanism, combined with an 18-year “forgetting period,” may leave millions of the neediest children unable to access this wealth.

- Singapore CPF’s Mandatory Integration: Singapore requires up to 37% of wages to be contributed and tightly links funds to housing, healthcare, and other basic needs, offering a 2.5%-4% risk-free minimum rate. In contrast, the “Trump Account” lacks such lifecycle integration and risk protection, resembling an isolated piggy bank rather than a social security system.

- “Baby Bond” Ideological Opposition: The “baby bond” proposal from Democrats like Cory Booker advocates for means-tested funding to narrow the wealth gap. The “Trump Account” provides equal federal seed funding but allows affluent families to contribute an extra $5,000 tax-free each year. Critics argue this essentially uses public funds to create a tax shelter for the rich, potentially widening rather than closing the wealth gap.

Mathematical modeling shows: at an annualized return of 7%, a low-income child with only $1,250 in seed funds and no ability to contribute may have just $4,200 after 18 years. A high-income child, with the federal $1,000 and maxing out $5,000 annual contributions, could have nearly $200,000 after 18 years—a staggering 46-fold difference.

Welfare Cutbacks and Future Scenario Modeling

Critics worry that the creation of the “Trump Account” is not purely additive, but a prelude to future welfare “subtraction.” Policymakers may use “everyone has a stock account” as an excuse to cut Social Security or other welfare spending. Reports indicate the related legislation includes clauses to cut Medicaid and food stamps. This means trading “future pie” for “present bread,” an extremely risky swap for families living on the edge.

Based on current data and historical experience, we can wargame three possible futures for the “Trump Account”:

- Scenario C: Bureaucratic Quagmire and Dormant Assets (UK Scenario):

- Premise: Complicated paperwork blocks low-income families from opening accounts; private managers lack incentive to serve small accounts.

- Result: Millions of accounts go dormant; Wall Street firms erode “ownerless assets” through fees.

- Political Impact: Policy is seen as a regressive fiscal subsidy, sparking criticism of bureaucracy and financial predation.

Conclusion: Locking in the Future—A Bet on Equity and Opportunity

The “Trump Account” and the “helicopter equity” philosophy behind it represent a profound reconstruction of American national governance logic. It attempts to use the power of financial compounding to turn every citizen into a stakeholder in the capital markets.

This bet hinges on three assumptions:

- Market Assumption: The U.S. stock market will always be an efficient wealth creator, not a casino.

- Behavioral Assumption: All families, rich or poor, will have the knowledge and patience to manage long-term assets.

- Social Assumption: Asset ownership can replace income redistribution as the ultimate solution to inequality.

Dell’s donation fuels the plan but also exposes its fragility in relying on private capital to patch public systems. If it succeeds, it could create a generation of asset-owning middle class; if it fails, it could bury an entire generation’s economic security in the volatility of the candlestick chart.

This is no longer simple “money dropping”—this is “equity dropping”. It not only redefines welfare but also seeks to redefine the relationship between citizens and capitalism. In this 18-year lockup, it’s not just funds that are locked in, but all of American society’s imagination of the word “opportunity.”