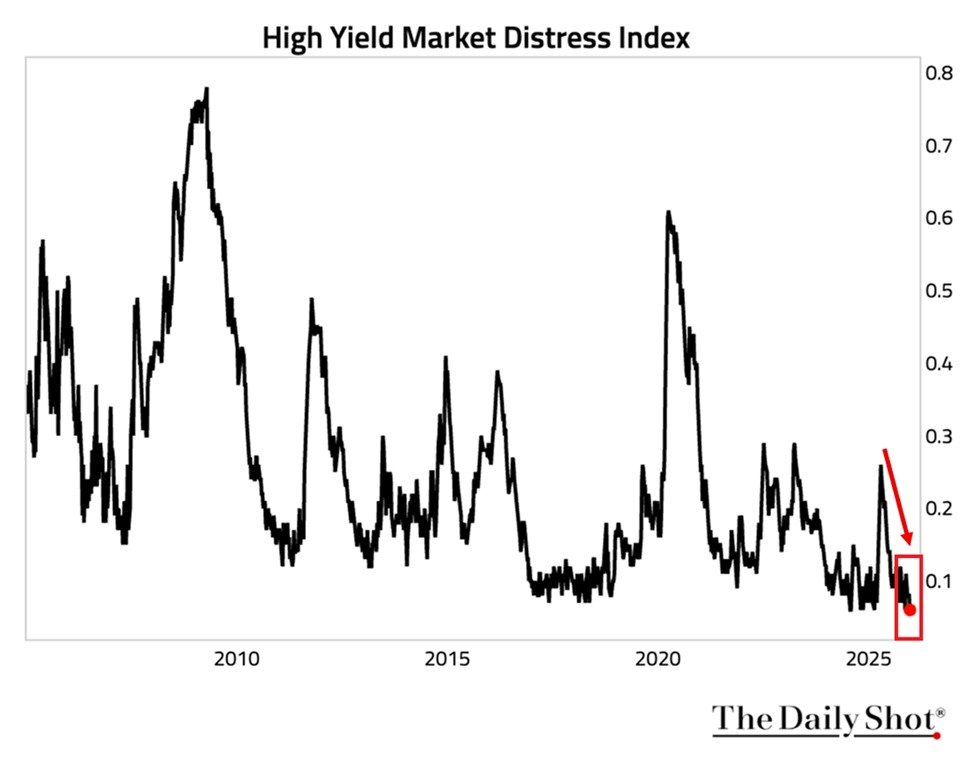

US credit market health has reached unprecedented strength, with the New York Fed high-yield distress index plunging to an all-time low of 0.06, signaling the most benign corporate borrowing conditions and junk bond market liquidity in history.

(Sources: DailyShot News)

Yet this abundance of risk appetite macro has failed to flow into cryptocurrency, leaving Bitcoin in extended consolidation near $91,000. This analyst insight examines the paradox of credit markets at record health amid stagnant crypto inflows, on-chain signals, institutional holder behavior, and potential catalysts for change as of January 8, 2026.

Measuring US Credit Market Health: The New York Fed High-Yield Distress Index

The New York Fed high-yield distress index tracks stress in the junk bond segment through liquidity, market functioning, and borrowing ease. Its drop to 0.06—far below 0.60 (2020 pandemic) and 0.80 (2008 crisis)—confirms exceptional junk bond market liquidity and corporate borrowing conditions.

High-yield ETF HYG delivered ~9% returns in 2025, marking a third consecutive strong year and underscoring broad risk appetite macro.

- All-Time Low: 0.06 on the distress index.

- Historical Comparison: Well below prior crisis peaks.

- ETF Performance: HYG reflecting sustained investor confidence.

- Macro Implication: Abundant systemic liquidity with minimal perceived default risk.

Liquidity Abundance vs. Crypto Starvation: The Paradox in Risk Appetite Macro

Despite credit markets at record health, capital has rotated preferentially to equities and gold rather than digital assets. CryptoQuant data shows Bitcoin inflows “dried up,” with risk appetite macro favoring traditional risk-on plays like AI-driven Big Tech stocks near all-time highs.

This hierarchy places crypto downstream in allocation decisions, creating a disconnect where healthy corporate borrowing conditions and junk bond market liquidity fail to spill over.

- Capital Rotation: Equities and precious metals absorbing flows.

- Crypto Inflows: Notably absent despite macro tailwinds.

- Institutional Preference: Risk-adjusted returns favoring non-crypto assets.

- Paradox Core: Liquidity plentiful, but not reaching Bitcoin.

On-Chain and Derivatives Signals Amid Credit Markets at Record Health

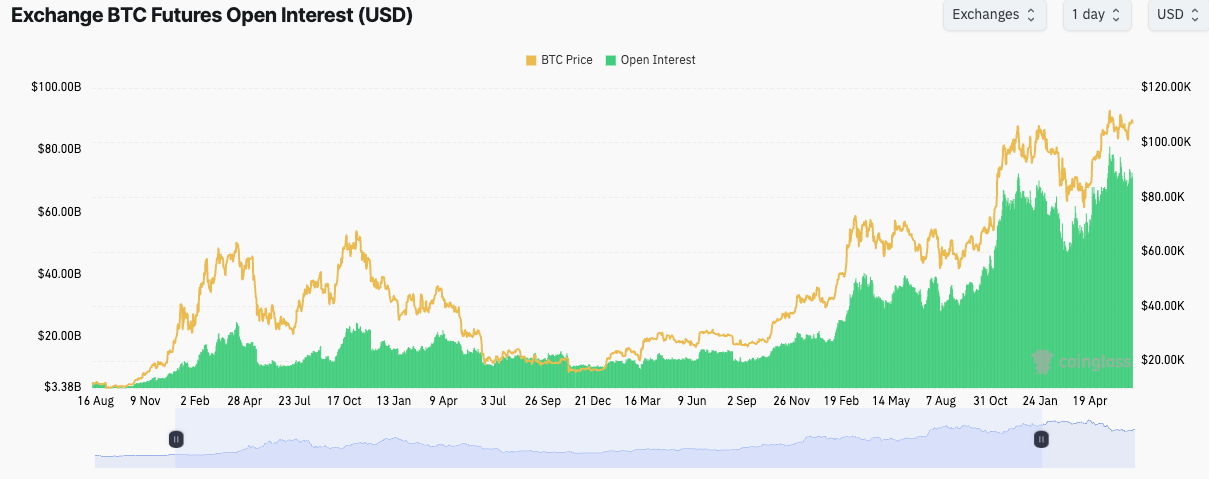

Bitcoin futures open interest stands at $61.76 billion across 679,120 BTC (+3.04% daily), led by Binance ($11.88B), CME ($10.32B), and Bybit ($5.90B). Price remains range-bound near $91,000 with $89,000 support, reflecting hedging rather than directional bets.

(Sources: coinglass)

Institutional long-term holders like MicroStrategy (673,000 BTC) exhibit minimal selling, compressing volatility and reducing crash probability.

- OI Stability: Steady positioning without aggressive longs/shorts.

- Holder Behavior: Patient capital via ETFs and corporates.

- Volatility Outlook: Sideways consolidation over sharp moves.

- Crash Likelihood: Low due to absent panic selling pressure.

Potential Catalysts to Resolve the Liquidity Paradox

Several triggers could redirect risk appetite macro toward crypto:

- Equity overvaluation prompting rotation to alternatives.

- More aggressive Fed easing amplifying broad risk-taking.

- Regulatory advancements lowering institutional barriers.

- Bitcoin-specific developments (post-halving supply, ETF options).

Absent these, extended sideways action remains the base case.

- Bull Triggers: Valuation extremes or policy shifts.

- Current State: Healthy but stagnant crypto market.

- Consensus View: Boring consolidation likely near-term.

In summary, US credit market health and credit markets at record health—evidenced by the New York Fed high-yield distress index at historic lows—highlight abundant junk bond market liquidity and favorable corporate borrowing conditions, yet fail to propel Bitcoin amid preferential flows to equities and gold. Strong risk appetite macro exists systemically, but crypto remains sidelined, supported by institutional restraint that limits downside while capping upside momentum. This liquidity paradox suggests consolidation persists until clearer rotation catalysts emerge. Monitor equity valuations, Fed signals, and on-chain inflows for potential shifts—always reference primary macro data and regulated sources when assessing cross-asset dynamics.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.