Due to waning investor demand, traders are shifting their focus to concerning U.S. macroeconomic data, with Bitcoin open interest dropping to $34 billion. Some of this decline is also attributed to forced liquidations, totaling $5.2 billion over the past two weeks. Bitcoin has fallen 28% over the past month, gold has retaken the $5,000 psychological level, and the S&P 500 is only 1% away from its all-time high.

Bitcoin Futures Open Interest Plummets, Forced Liquidations as Catalyst

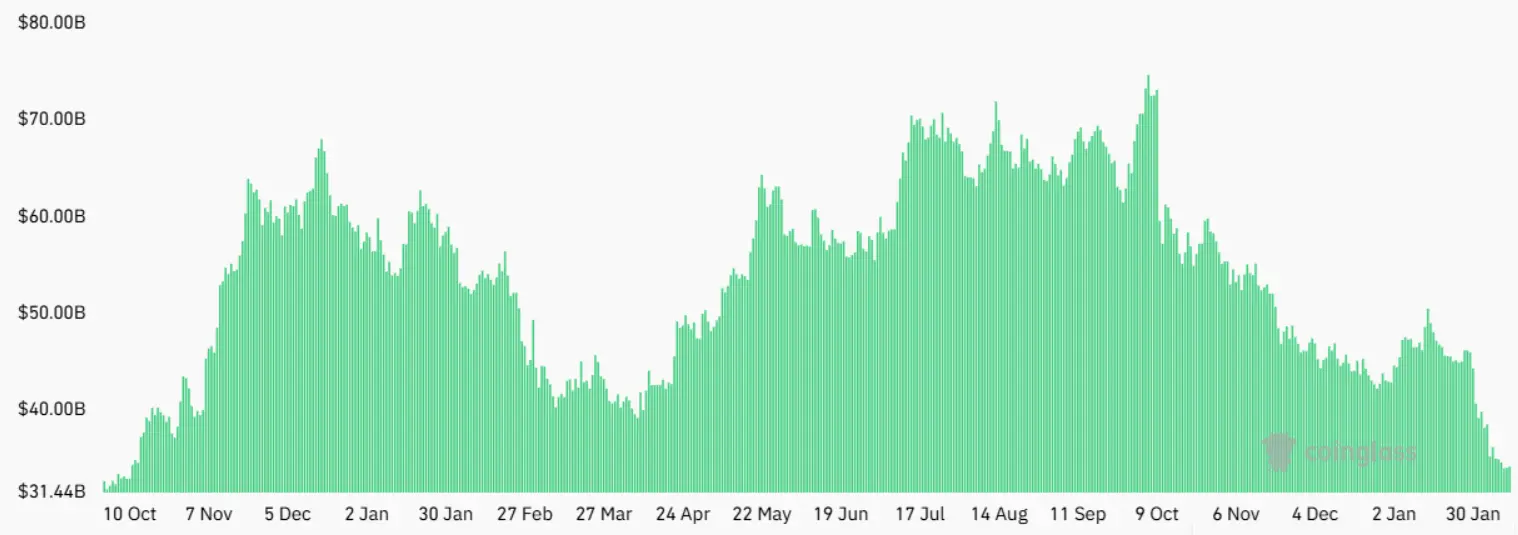

(Source: Coinglass)

On Thursday, total Bitcoin futures open interest reached $34 billion, down 28% from 30 days prior. However, in Bitcoin terms, this indicator is essentially flat at 502,450 BTC, indicating that leverage demand has not actually decreased. Part of the decline is also due to forced liquidations, with total liquidations amounting to $5.2 billion over the past two weeks. This contradictory phenomenon—dollar-denominated collapse while Bitcoin-denominated open interest remains stable—reveals the true reason behind the drop in open interest.

From an absolute figure of $34 billion, this is the lowest level since November 2024, when Bitcoin was trading around $40,000–$50,000 and the market was relatively subdued. Currently, Bitcoin is around $66,000, well above the November 2024 levels, yet open interest has fallen to the same level, indicating that even at higher prices, market participation and leverage usage have significantly shrunk.

A 28% monthly decline is a dramatic change in the derivatives market. Normally, open interest adjusts slowly with price movements, with monthly changes usually within 10%. The current 28% plunge suggests some form of “liquidation event,” where large leveraged positions were forcibly liquidated or actively closed. The $5.2 billion in liquidations over the past two weeks is direct evidence of such a cleansing process.

Dual Interpretations of the Open Interest Collapse

Pessimistic: Institutional and professional traders are retreating, losing confidence in Bitcoin

Neutral: Dollar-denominated decline but Bitcoin-denominated stable, merely an accounting effect of price drop

Optimistic: Deleveraging makes the market healthier and sets the stage for future gains

The Bitcoin-denominated open interest of 502,450 BTC is crucial. It indicates that the actual amount of leveraged positions (measured in BTC) has not significantly decreased. The decline in dollar value of open interest is mainly due to Bitcoin’s price dropping from about $90,000 (a month ago) to $66,000 now, reducing the USD value per BTC by approximately 27%, and thus lowering total USD value accordingly. This explanation mitigates the pessimistic view of a “leverage demand collapse.”

$5.2 Billion Liquidations and Funding Rate Panic Signals

(Source: Laevitas)

Part of the decline is also due to forced liquidations, with total liquidations reaching $5.2 billion over the past two weeks. This $5.2 billion in liquidations occurred within two weeks, indicating a period of intense deleveraging. These liquidated positions were mainly longs (betting on price increases), and when Bitcoin’s price fell below their liquidation levels, exchanges forcibly sold their positions to repay loans. This forced selling added further downward pressure, potentially triggering more liquidations and creating a “liquidation spiral.”

Over the past month, Bitcoin has fallen 28%, and investors are increasingly frustrated due to the lack of clear catalysts, especially as gold has retaken the $5,000 psychological level and the S&P 500 is only 1% below its all-time high. Some analysts believe this risk-averse sentiment stems from signs of a weakening U.S. labor market. Data released by the U.S. Department of Labor on Wednesday projects only 181,000 new jobs in 2025, below previous estimates.

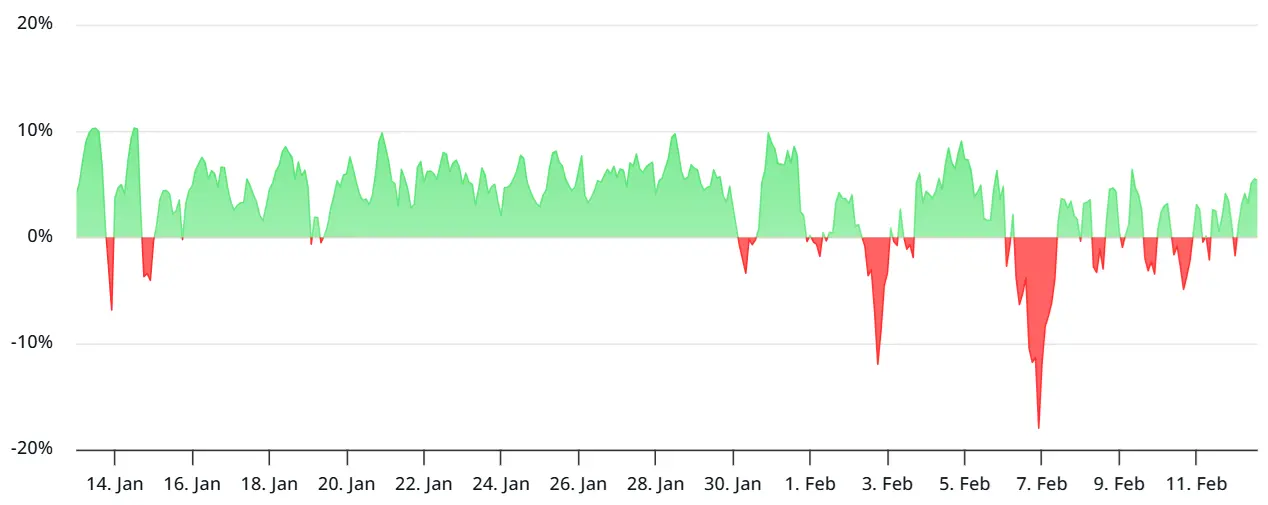

Over the past four months, the annualized funding rate for Bitcoin futures has remained below the neutral threshold of 12%, indicating persistent market panic. The funding rate is the fee paid between longs and shorts in perpetual contracts to keep the contract price aligned with the spot price. Normally, the rate is slightly positive (longs pay shorts), reflecting a mildly optimistic market. When the funding rate remains below neutral or turns negative for an extended period, it signals that shorts dominate and the market is overall pessimistic.

(Source: Laevitas)

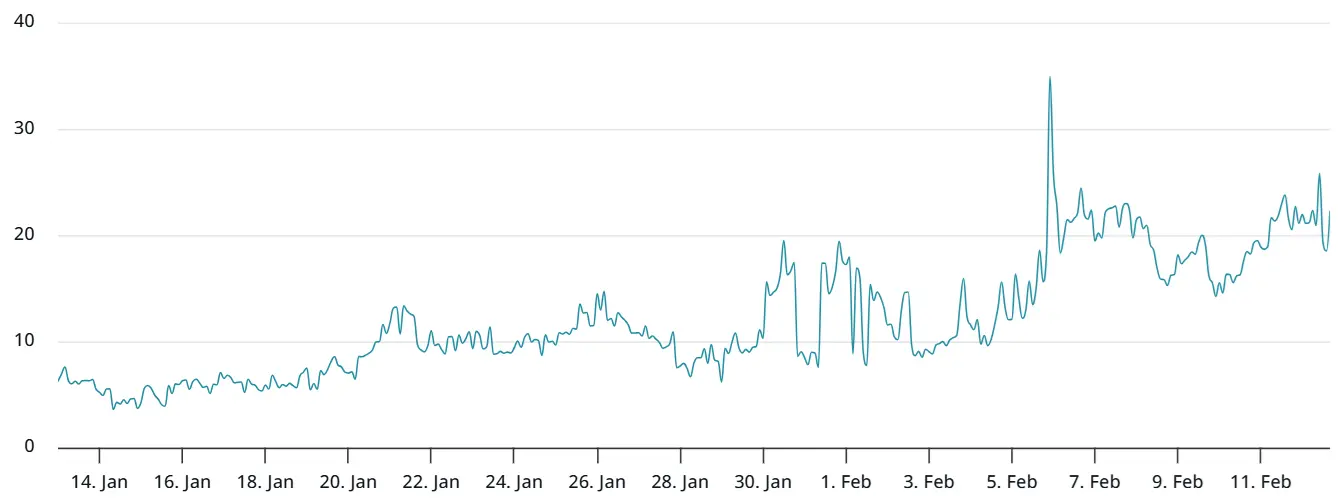

Therefore, even though the indicator has rebounded from its lows last week, shorts still dominate. According to data from the Bitcoin options market, professional traders are still reluctant to take on downside risk. On Thursday, due to a premium in put options, the Delta skew of Bitcoin options on Deribit soared to 22%. Under normal conditions, this indicator fluctuates between -6% and +6%, reflecting a balanced risk appetite for upside and downside.

A 22% Delta skew is an extreme defensive signal. It indicates that demand for put options far exceeds that for call options, with traders willing to pay high premiums for downside protection. This behavior typically occurs when the market anticipates a major negative event. The last time the skew turned bullish was in May 2025, when Bitcoin retested $75,000 and then surged back to $93,000.

Contradictory Signals from ETF Daily Trading Volume of $5.4 Billion

Despite the weakness reflected in derivatives indicators, the average daily trading volume of $5.4 billion in U.S.-listed Bitcoin ETFs contradicts the notion of waning institutional demand. While it’s impossible to predict what factors might motivate strong buying, Bitcoin’s recovery may depend on the clarity of the U.S. employment situation.

The $5.4 billion daily volume is a relatively healthy figure. It shows that, even in the current subdued environment, substantial funds are flowing through the ETF market. However, high trading volume does not necessarily mean net inflows. It could result from two-way flows of redemptions and creations, market maker hedging, or rotation among different ETFs. The current situation is more likely the latter two, as net inflow data shows continued outflows.

This divergence—shrinking derivatives and sustained ETF trading volume—may reflect different investor behaviors. The derivatives market is mainly driven by professional traders and hedge funds, who are highly sensitive to market sentiment and quickly adjust leverage and positions. When the market turns bearish, these professionals rapidly retreat, causing open interest to plummet. Conversely, ETF participants tend to be long-term institutional investors (such as pension funds and wealth managers), whose decision cycles are longer, and they may continue holding even during short-term losses.

Over the past week, Bitcoin’s price has struggled to stay above $72,000, raising questions about whether institutional demand has already vanished. Bitcoin futures open interest has fallen to its lowest since November 2024, intensifying concerns that Bitcoin’s price could test the $60,000 support again amid increasing uncertainty. A break below $60,000 could trigger another wave of panic selling and liquidations, further depressing open interest and price.