The U.S. strategic Bitcoin reserve could lose nearly 30% of its holdings after a legal decision, even if the government does not sell any BTC.

Last year, President Donald Trump signed an executive order establishing the Strategic Bitcoin Reserve (SBR). The order requires the U.S. Treasury to consolidate all government-controlled BTC into a reserve account and commits not to sell these assets.

However, headline figures about the size of the reserve may be exaggerating the amount of BTC that the government can truly consider a long-term strategic asset.

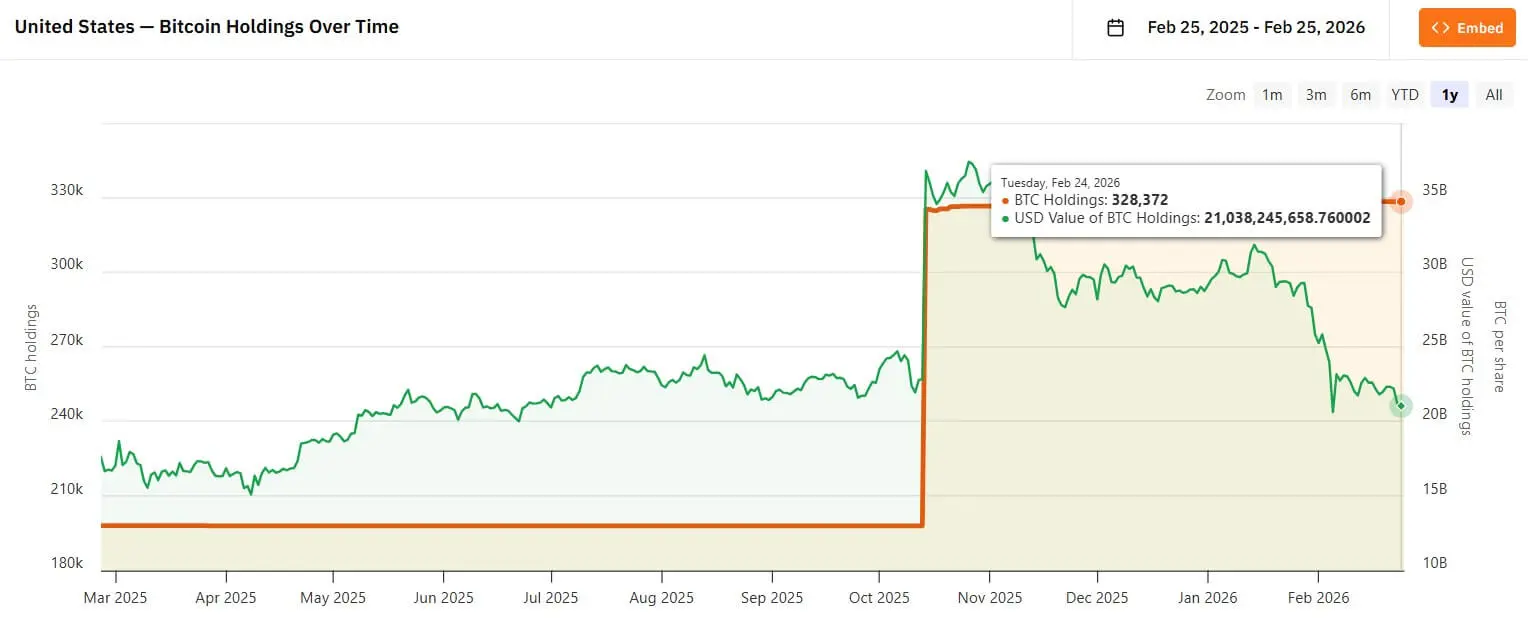

According to data from Bitcoin Treasuries, the U.S. government controls approximately 328,372 BTC, making it the largest national BTC holder in the world. At around $65,842 per BTC, this amounts to about $21.6 billion.

But the issue is: a significant portion of these are seized BTC, not necessarily “clean” assets fully owned as strategic holdings by the government.

The executive order allows assets to be handled according to court rulings and explicitly states exceptions for assets that need to be returned to verified victims in criminal cases.

This exception is especially important because about 94,643 BTC—nearly 30% of the government’s holdings—are related to the 2016 Bitfinex hack.

If these BTC are returned through compensation mechanisms, the reserve size would automatically decrease to around 234,000 BTC.

U.S. Bitcoin Treasury (Source: Bitcoin Treasury)## The reserve figure is real, but ownership remains uncertain

U.S. Bitcoin Treasury (Source: Bitcoin Treasury)## The reserve figure is real, but ownership remains uncertain

The Strategic Bitcoin Reserve is often viewed as a “clean” national asset balance sheet. In reality, it’s a structure blending legal and accounting considerations.

Some BTC have completed seizure processes and are clearly under U.S. control. However, others are entangled in criminal cases, claims for compensation, or lengthy legal procedures.

The case of 94,643 BTC related to Bitfinex is the clearest example. These BTC are held under government custody and are counted in the total reserve by the market.

But if a court rules that these assets must be returned to victims, they are not truly long-term strategic assets.

This suggests both sides may be missing the core issue.

Optimists might overestimate the sustainability of the reserve if they assume all BTC controlled by the government are permanent strategic assets. Conversely, pessimists might overstate market impact by viewing potential returns as “sales” by the government.

This legal distinction significantly influences prices, market sentiment, and how investors interpret the role of the SBR.

Why are Bitfinex’s BTC still “frozen”

The Bitfinex hack in August 2016 resulted in 119,754 BTC stolen, one of the largest crypto thefts in history.

In February 2022, U.S. authorities recovered about 94,643 BTC related to this case, a move notable for both scale and timing.

The next issue is the compensation mechanism.

By January 2025, prosecutors propose to a federal court to allow restitution to Bitfinex in “in-kind” form—that is, returning BTC directly rather than selling and converting to USD.

This difference is significant for market structure.

If the government sells or auctions the BTC, the market will see a clear supply event with specific scale and timing. Conversely, restitution in BTC shifts the decision to the recipient—possibly Bitfinex, former users, or both—depending on the final ruling.

Under U.S. asset seizure procedures, third parties can file claims in auxiliary proceedings. In the Bitfinex case, this is the central dispute.

Some claimants argue the stolen assets are their personal property. Meanwhile, Bitfinex contends they are the ultimate economic victims after allocating losses and compensating users through internal mechanisms.

The outcome could set a precedent for future handling of exchange hacks.

Until courts rule or parties reach an agreement, these BTC remain “frozen” in practice, even if on the blockchain they appear stable.

LEO becomes a “pricing tool” for court rulings

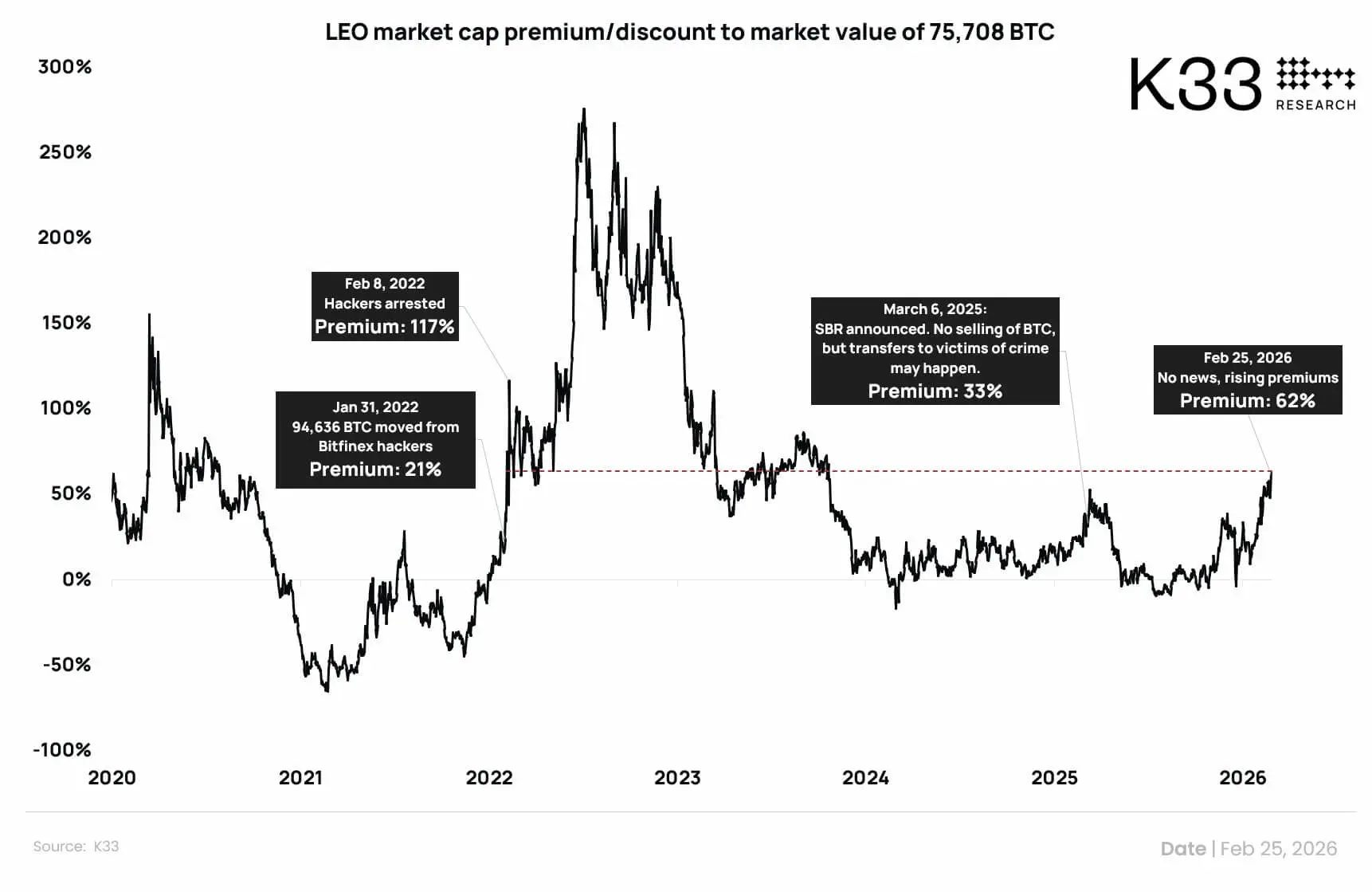

While legal proceedings are slow, the market is trying to price the outcome via the UNUS SED LEO (LEO) token—Bitfinex and iFinex’s exchange token.

Bitfinex states that if recovered BTC are received, 80% of the net value will be used to buy back and burn LEO over 18 months, including OTC trades like direct BTC-to-LEO swaps.

LEO Premium (Source: Vetle Lunde) This turns a federal court decision into a large-scale buyback mechanism, allowing market speculation on the timeline before an official ruling.

LEO Premium (Source: Vetle Lunde) This turns a federal court decision into a large-scale buyback mechanism, allowing market speculation on the timeline before an official ruling.

According to Vetle Lunde, Head of Research at K33 Research, LEO’s two main price drivers are: buyback programs from trading revenue and expectations of token burns from recovered BTC.

Assuming about 95,000 BTC are returned, 80% equals roughly 75,000 BTC, worth nearly $5 billion at current prices. Meanwhile, buyback from trading revenue is only about $125 million in reasonable value.

Data from CoinMarketCap shows LEO has a market cap of around $8 billion but a 24-hour trading volume of only about $7.1 million—low liquidity, amplifying price volatility.

LEO is currently trading at a premium of about 60% over its estimated fair value, the highest since the strong rally after the 2022 seizure announcement. Low liquidity and concentrated ownership mean a small group of investors could significantly influence the price.

Therefore, the market may be “front-running” asset transfers or simply riding momentum amid declining intrinsic value.

Headlines may be more shocking than actual BTC supply flow

Macro context in early 2026 shows Bitcoin trading in a risk-off environment. Spot Bitcoin ETFs have experienced over $4.5 billion in net outflows over five consecutive weeks.

In such a sensitive supply environment, a headline like “U.S. transfers 95,000 BTC” would surely cause shock.

However, if assets leave government custody, it’s an act of restitution, not a sale. And if Bitfinex executes its buyback and burn plan, BTC will be gradually allocated over time rather than dumped all at once.

Preliminary estimates suggest that 75,000 BTC over 18 months equals about 139 BTC per day—insignificant compared to the long-term holding pressure from institutional investors and ETF withdrawals over the past five months.

Thus, the biggest impact may come from media interpretation rather than actual supply movements.

The SBR is not just a digital asset reserve; it’s also a political and market signal. Framing it as “U.S. losing 30% of Bitcoin reserves” could trigger volatility due to emotional reactions and short headlines.

Legally, if Bitfinex’s BTC leave government control, the U.S. is not abandoning its reserve policy. On the contrary, it’s executing within the rule of law—aligned with the principles established when the Strategic Bitcoin Reserve framework was created.