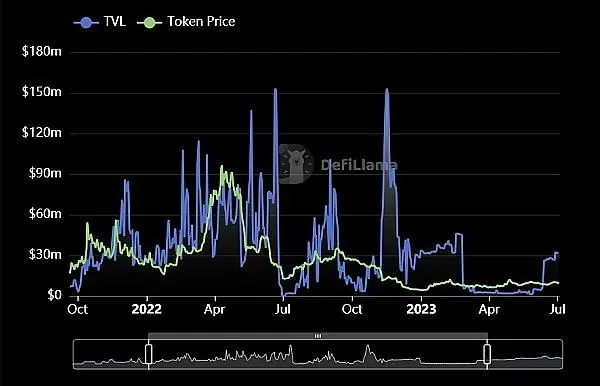

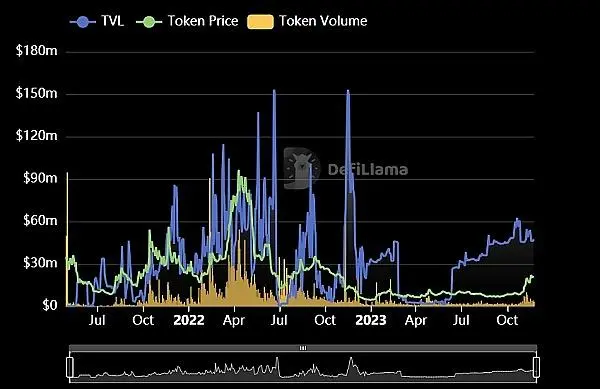

As of Q2 2023, Maple Finance’s (MPL) total value locked (TVL) has grown significantly, quadrupling. This growth reflects Maple Finance’s active presence in the crypto lending market, particularly in the lending and tokenization of real-world assets (RWA).

This year, Maple Finance launched three new products that partly drove its TVL to $100 million. Below, we will introduce this project and its related products.

Three new products have been recognized by the market, and Maple Finance is actively entering the RWA track

First, Maple Finance provides a robust investment channel for the market by launching a pool of cash management funds collateralized by U.S. Treasuries. This strategy not only increases the security of funds, but also ensures stable returns for investors.

Subsequently, the company launched Maple Direct, a platform that provides lending solutions for BTC and ETH funds, effectively filling the void left by the collapse of the centralized finance (CeFi) lending market.

Eventually, Maple Finance launched a lending service for RWA assets, a move that caused a strong response among high-net-worth individuals (HNWIs) as it capitalized on the scarce non-correlated yield opportunities in the private credit market.

Commenting on the company’s growth trajectory, CEO Sid Powell said: "Our success is largely due to our aggressive expansion into the Asian market and our expansion into the on-chain private credit space. There has been a lot of attention about the earning potential that RWA brings, and Maple’s pools are the best response to this demand. We are committed to continuous innovation to provide our customers with a safer and more reliable loan option. ”

Maple Finance (MPL) has demonstrated its potential in the combination of traditional finance concepts and the decentralized finance (DeFi) space. The company’s efforts to ensure product safety, diversification, and exploration of new markets bode well for continued growth in the future. To better understand this phenomenon, let’s take a closer look at Maple Finance’s core products and strategies.

From the operation mechanism of Maple Finance, look at the specific gameplay and operation process of the project

Maple Finance, an institutional-grade crypto capital network based on Ethereum and Solana, aims to revolutionize the way traditional capital markets operate through the use of digital assets. The platform’s core focus is to drive the expansion of the digital economy by providing unsecured loans to institutional borrowers while creating revenue opportunities for lenders.

Maple Finance’s recently launched U.S. Treasuries-based cash management product and its V2 upgrade explore how to effectively integrate crypto assets with real-world assets (RWAs) to improve the liquidity and stability of its lending platform. What distinguishes Maple Finance from other DeFi projects is its low-collateral lending model, which aims to revolutionize the global digital finance and lending market. At present, the total amount of loans on the platform has exceeded $290 million.

Maple Finance operates in several key roles: borrowers, depositors, and pool delegates. Borrowers are typically institutions deep in the crypto space, including market makers and market-neutral funds. In order to become borrowers, they need to submit an application to Maple, which is already joined by institutions such as AQRU Receivables, M11 Credit, Icebreaker Finance, and more. Depositors will need to meet Maple’s eligibility criteria and borrower-specific requirements, such as completing anti-money laundering checks, accepting Maple’s terms and conditions, and submitting an application to an approved borrower. Pool Delegates is made up of funds and industry experts with extensive credit experience. Their responsibilities include negotiating loan terms with borrowers, conducting financial due diligence, and, if necessary, liquidating defaulted collateral. They also take the risk of losing their money in the first place.

At Maple Finance, the borrowing process includes the borrower’s account creation, the approval process, financial due diligence, and on-chain loan application and funding provision. For users, the deposit process covers preparing enough gas fees, anti-money laundering scanning of wallet addresses, accepting Maple’s terms and conditions, and choosing the investment amount and term.

Maple Finance’s model puts pool representatives at the heart of risk management, and although their funds may not be able to provide timely compensation in the event of a lender’s default, they play a key role in risk control.

The platform operates on a foundation of decentralization, smart contracts, and trust mechanisms. The project uses blockchain technology to remove intermediaries from transactions, thereby reducing costs, improving efficiency, and providing users with a secure and transparent lending environment. In addition, Maple Finance’s cross-chain functionality and token economy model provide users with the opportunity to participate in the development of the platform and revenue sharing.

To sum up, Maple Finance has brought new vitality to the digital lending market through its innovative operating mechanism and core features, solved the trust and efficiency problems existing in the traditional financial system, and injected innovation momentum into the digital finance field.

Constantly adapting the product line to new changes in the market, Maple Finance has a certain spirit of innovation

Following Maple Finance’s crypto capital network building on Ethereum and Solana, its product line has also undergone significant evolution. Initially, Maple Finance focused on unsecured lending projects based on real world assets (RWA). However, this unsecured lending model was too risky, resulting in a huge amount of bad debt of more than $50 million for Maple. In response to this challenge, Maple made a strategic shift in April 2023 with the launch of a new cash management pool that allows non-US accredited investors and entities to participate directly in U.S. Treasury investments through USDC.

This strategy adjustment appears to be a direct response to previous losses. Maple Finance is starting to focus more on RWA-based lending and has made new attempts at product diversification. Its pool representatives are exploring the use of real-world assets as collateral instead of relying on cryptocurrency collateral to issue loans.

Take, for example, Maple Finance’s cash management pool, which is managed by the cryptocurrency hedge fund Room 40 Capital. They set up an independent Special Purpose Vehicle (SPV) that acts as the main borrower of the pool. The pool attracts USDC deposits from non-U.S. accredited investors and institutions, which are used to purchase and hold short-term U.S. Treasury bills and reverse repo agreements backed entirely by U.S. Treasury bills. Currently, the pool’s 30-day average interest rate reaches 4.58%.

In addition, Maple further expanded its product offering by launching a liquidity pool backed by tax receivables in January this year.

Notably, in July this year, Maple launched its own direct lending arm, Maple Direc. This new division will focus on underwriting and lending services for Web3 businesses, with the aim of filling the gap left by the collapse of centralized lenders such as BlockFi and Genesis. Maple Direct features a transparent blockchain infrastructure that bypasses traditional banks and intermediaries and directly leverages a transparent blockchain infrastructure to provide capital to borrowers. This not only provides professionally managed lending opportunities for investors such as funds, DAOs, and high-net-worth individuals, but also effectively reduces credit and counterparty risk.

What’s special about Maple Direct’s first lending product, launched in July, is that it uses BTC, ETH, and staked ETH as excess collateral and is executed on the blockchain via smart contracts, while its terms and loan history are transparently displayed on Maple’s public lending dashboard.

These changes and innovations not only demonstrate Maple Finance’s adaptability in meeting challenges, but also demonstrate its innovative spirit and ability to diversify in the field of digital lending. With these new strategies, Maple Finance is not only on the path to returning to growth, but also provides its customers and investors with a wider range of options and more optimized investment opportunities.

Understand the MPL token model: 36% of assets are currently circulating in the market

The MPL token is a key component of Maple Finance’s ecosystem, which performs multiple functions. The total issuance of MPL is set at 10 million, and there are currently about 3.659 million tokens in circulation. The distribution of these tokens follows a clear structure: 30% is allocated to liquidity farming, 25% is owned by seed rounds and advisors, 26% is used by seed investors, 5% is issued through a public sale, and 14% is set aside for fiscal purposes.

The value capture of MPL tokens is mainly achieved in two ways: one is through the distribution of protocol revenue, and the other is through stake rewards. MPL holders can stake it into Maple’s smart contract in exchange for xMPL, and the revenue from the Maple protocol will be accumulated in these xMPL. According to the terms of the agreement, half of the initial monthly agreement revenue will be used to buy back MPL in the market. These repurchased MPLs are then distributed to xMPL holders, forming a dividend system.

MPL’s source of revenue is primarily the set-up fees for each loan on the Maple Finance platform, which are charged at an annualized rate of 0.99%. Two-thirds of this revenue goes to the Maple Finance treasury, and the remaining one-third is paid to representatives of the loan pool. This simple business model ensures that as the volume of loans increases, so does Maple Finance’s revenue, increasing the funds to buy back MPL.

The main demand for MPL tokens comes from the following:

-

MPL stakers, who obtain xMPL by staking MPL, and then earn income from the protocol income.

-

Borrowers, the loan set-up fees they pay become part of the agreement revenue, increasing the value of MPL.

-

MPL holders who participate in governance, they can participate in the decentralized governance of Maple Finance through voting, and influence the direction and decision-making of the project.

Maple Finance has built a participatory, self-reinforcing economic model with the MPL token, designed to motivate the active participation of community members and ensure the continued development of the platform. With the launch of xMPL, MPL holders will enjoy additional income earned through staking, as well as the opportunity to participate in governance and provide other utility features.

As the token of Maple Finance, MPL is not only a financial tool, but also a source of power to promote the development of the platform and community participation. Through MPL, Maple Finance has built an ecosystem that is both conducive to long-term growth and incentivizes community participation.

It will take time to verify whether Maple Finance can maintain a stable growth trend in the future

As Maple Finance continues to grow in the token economy, product innovation, and go-to-market strategy, the platform is at a critical juncture in the crypto lending space.

Through the diversified application of the MPL token and the reinvestment of protocol revenue, Maple Finance has demonstrated its ability to adapt to market changes and challenges. At the same time, Maple Finance’s product line, from its initial unsecured lending to its current diversified asset pool, reflects the flexibility of its strategy and the sensitivity of market demand.

In the future, whether Maple Finance can continue to maintain its market position and attract more users will depend on its performance in maintaining the stability of the platform, developing innovative products, and improving the token economic model. As one of the participants in the crypto lending market, the future development of Maple Finance is worth observing and looking forward to.

Source: Golden Finance