Author: Peng Xingyun, Deputy Director of the National Institute of Financial and Development

Following the Central Political Bureau meeting on December 9, 2024, which proposed to implement a ‘moderately loose monetary policy,’ the Central Economic Work Conference held on December 11-12, 2024, once again emphasized this direction of monetary policy. This is the first time in more than a decade that China has shifted its expression of monetary policy direction from ‘prudent monetary policy’ to ‘moderately loose monetary policy,’ attracting high market attention. This article analyzes the orientation of a moderately loose monetary policy, involving several important issues: why implement a moderately loose monetary policy? What policy measures might the central bank take? What impact might a moderately loose monetary policy have?

Monetary Policy Analysis- From “Prudent” to “Moderately Loose”

0****1 Why implement a moderately loose monetary policy

Maintaining currency stability and promoting economic growth are the ultimate goals of our country’s monetary policy by law. As an important tool and means of total demand management, monetary policy aims to smooth out economic fluctuations, and the stance of monetary policy depends on the performance of the macroeconomy. When the economy is overheated and there is significant inflationary pressure, the central bank will adopt a contractionary monetary policy; conversely, when economic growth is weak and there is significant employment pressure, the central bank will implement a relatively loose monetary policy. This is the basic principle of central banks in various economies in their monetary policy operations, and it is no exception for the socialist market economy with Chinese characteristics.

In the 24 years since the new millennium, except for the explicit mention of ‘moderately loose monetary policy’ in 2009 and 2010, China’s monetary policy in other years has been defined as ‘prudent monetary policy.’ When China first proposed ‘proactive fiscal policy’ and ‘prudent monetary policy,’ it was during the impact of the Asian financial crisis, requiring the government to take strong measures to stabilize the macroeconomy. Therefore, ‘prudent monetary policy’ actually refers to loose monetary policy. However, after the new millennium, ‘prudent monetary policy’ has actually become a basic principle of China’s monetary policy operations, no longer corresponding to loose or contractionary monetary policy. In fact, in the ‘prudent monetary policy’ implemented since the new millennium, in some years, the central bank has continuously raised the statutory deposit reserve ratio or the benchmark interest rate for deposits and loans, while in other years, it has consistently lowered the deposit reserve ratio and increased the central bank’s re-lending to financial institutions. Regardless of the direction of monetary policy operations taken by the central bank, it is all aimed at ‘maintaining reasonable and ample liquidity.’

The Central Economic Work Conference clearly put forward the “need to implement a moderately loose monetary policy”, and conveyed a clear direction of monetary policy operation to the economic system, that is, through more abundant liquidity supply, reduce market interest rates, boost market confidence, and improve expectations. However, this does not mean that China’s monetary policy has abandoned the principle of “prudence”, because the “loose monetary policy” must be “moderate”, not excessively loose or flooded, and still requires that “the scale of social financing and the growth of money supply match the expected targets of economic growth and overall price level”.

It is important to note that the Central Economic Work Conference has proposed to “implement a moderately loose monetary policy”, which is not a fundamental change in the monetary policy stance. In fact, in the past few years, the People’s Bank of China has been adopting a relatively loose monetary policy to maintain reasonable and adequate liquidity. Firstly, since 2015, the central bank has successively lowered the statutory deposit reserve ratio more than 20 times, with the statutory deposit reserve ratio of large commercial banks dropping from the original high of 21.5% to the current 9.5%, and the deposit reserve ratio of small and medium-sized commercial banks dropping from the original high of 19.5% to the current 6.5%. This alone has released over 10 trillion yuan of originally frozen liquidity. Secondly, the central bank has provided liquidity to the market through various re-lending tools, as reflected in the central bank’s balance sheet. The central bank’s claims on deposit-taking financial institutions have increased from less than 2.5 trillion yuan at the end of 2014 to over 17.4 trillion yuan at the end of September 2024, an increase of nearly 15 trillion yuan in less than 10 years. Thirdly, although the central bank has not adjusted the benchmark deposit and lending rates since 2015, it has directly driven down market interest rates through continuous reduction of the central bank’s policy rates in its monetary policy operations. For example, the loan prime rate (LPR) has decreased from 5.76% in 2014 to the current 3.1%, and the weighted average interest rate on RMB loans of financial institutions has decreased from 6.96% at the end of June 2014 to the current 3.67%, a drop of over 300 basis points. Corresponding to the significant decline in loan rates, the bond market rates have also experienced the longest downward cycle since the reform and opening up, with the yield on 10-year government bonds dropping from around 3.88% in early December 2017 to less than 1.8% currently. In summary, the continuously declining bond market yields reflect the fact that China’s liquidity and monetary policy have been relatively loose.

So, why explicitly propose the implementation of a moderately loose monetary policy when the monetary policy has already been loosened? Fundamentally, this is the need of the macroeconomy. The Central Economic Work Conference pointed out in diagnosing the macroeconomic situation of our country, “Our country’s economic operation still faces many difficulties and challenges, mainly inadequate domestic demand, operational difficulties for some enterprises, pressure on increasing employment and income for the masses, and still many hidden risks.”

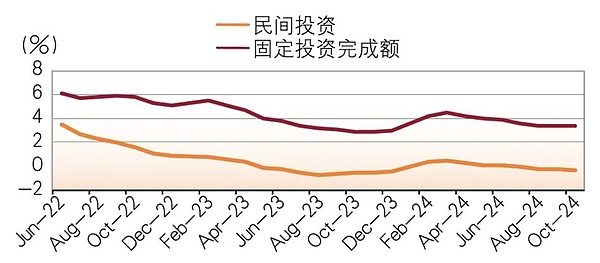

First, investment and consumption demand are weak. Fixed asset investment has been low after the epidemic, with the growth rate of fixed asset investment staying below 5% since 2023. In particular, private fixed asset investment is extremely weak. Since December 2022, the growth rate of private fixed asset investment has been below 1%, and most months since May 2023 have shown negative growth in private fixed investment (see Figure 1). Due to insufficient private investment, in order to stabilize growth and investment, it has been necessary to rely on government investment, which has increased the financial pressure of governments at all levels and added to government debt burden. Ultimately, consumption is also very weak. In the early stages after the end of the epidemic, although the total retail sales of consumer goods in the domestic market rebounded briefly, it did not last long, revealing a relatively weak trend. In December 2022, when domestic epidemic control measures were relaxed, the growth rate of total retail sales of consumer goods was -0.2%, rebounding to 9.3% by May 2023, and then steadily declining, dropping to below 4% after June 2024.

Figure 1: The completed amount of fixed asset investment in China and the growth rate of private investment

Source: According to Wind

Secondly, low prices. Since October 2022, China’s PPI has been in negative growth for 26 consecutive months, with PPI below -2.5% in the recent three months (September to November 2024). Although CPI has performed slightly better than PPI, it has been hovering around 0 for 17 months, significantly below the 2% inflation target of major global countries (see Figure 2). Therefore, Pan Gongsheng, the governor of the central bank, stated in October 2024, “Promoting a reasonable rise in prices will be an important consideration.” Due to the sustained low price levels, it has also created a more flexible space for further implementation of moderately loose monetary policies.

! image.png

Figure 2 China’s CPI and PPI

Source: Compiled according to Wind

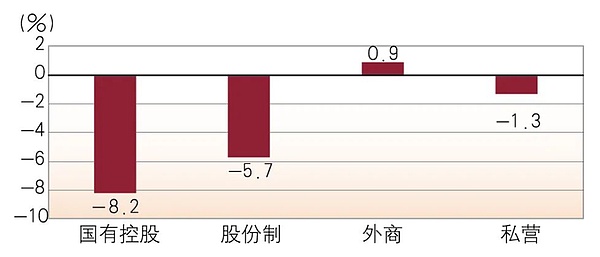

Third, the growth rate of corporate profits has continued to decline. **According to data from the National Bureau of Statistics, from January to November 2024, in addition to the profits of foreign-funded enterprises and enterprises with investment from Hong Kong, Macao and Taiwan, which barely maintained positive growth, the total profits of state-controlled enterprises and joint-stock enterprises decreased significantly, with the profit growth rate of China’s state-controlled enterprises being -8.2% and joint-stock enterprises being -5.2%, and the profit growth rate of private enterprises not falling as much as the previous two, but also -1.3% growth. Corresponding to the continuous decline in the growth rate of corporate profits, the capacity utilization rate of industrial enterprises has also declined significantly (see Figure 3), with only 74.6% capacity utilization in the third quarter of 2024, which means that more than 25% of capacity is idle. In fact, the 2023 Central Economic Work Conference pointed out that “some industries have overcapacity”. The continued decline in profit growth and the high level of idle production capacity are bound to further adversely affect the confidence of enterprises, which is one of the important factors for the weak private investment.

Profit growth rates of industrial enterprises of different ownerships from January to November 2024 in Figure 3

Data Source: National Bureau of Statistics

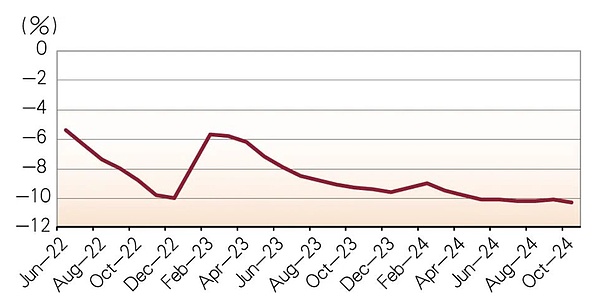

Fourth, the real estate industry is still undergoing a deep adjustment. In the past few years, despite the government issuing multiple policies to support the development of the real estate industry, the downturn in the real estate industry has not been fundamentally reversed, and the real estate industry is still in a deep adjustment phase. From April 2022 to November 2024, the completed investment in real estate development in China has been in negative growth for 30 consecutive months, and the negative trend has not only failed to converge but has slightly worsened. From May to November 2024, the growth rate of completed investment in real estate development exceeded -10%, while from September 2023 to April 2024, it was between -9% and -9.8% (see Figure 4). What has decreased even more than the decline in completed investment in real estate development is the construction area and sales area of real estate. Since 2024, the growth rate of real estate construction area has been below -10%, and although the decline in sales area growth rate has narrowed, it still remains in the range of -15% to -20%. In particular, the growth rate of presale area of real estate is in the range of -25% to -32%, putting great pressure on the capital turnover of real estate development enterprises (see Figure 5).

Figure 4 Growth rate of real estate development investment in China

Source of information: Compiled according to Wind

! image.png

Figure 5 Growth Rate of Real Estate Sales Area in China

Source: According to Wind

Fifth, there is greater pressure on youth employment. **Although the statistical urban unemployment rate has remained stable on the whole and has not increased significantly, a large number of rural migrant workers, who were originally concentrated in the construction, real estate and other industries, have had to return to their hometowns due to the adjustment of the real estate industry, which has reduced the statistical unemployment rate. In June 2022, the youth unemployment rate for those aged 16-24 was 16.7%, and at the end of March 2023, the youth unemployment rate reached 19.6%. According to the spokesperson of the National Bureau of Statistics on the operation of the national economy in the first half of 2023, the youth unemployment rate at the end of June 2023 further rose to 21.3%. The Bureau of Statistics has since stopped publishing data on the youth unemployment rate, but in the case of declining investment and capacity utilization, at least one thing can be roughly judged - the youth unemployment rate has not been fundamentally reversed. This is exactly what the Central Economic Work Conference pointed out that “the masses are facing pressure to increase employment and income”.

0****2 Possible measures for the central bank to implement moderately loose monetary policy

The Central Economic Work Conference pointed out: “Give full play to the dual functions of total and structural monetary policy tools, timely cut reserve requirements and interest rates… Explore and expand the macro-prudent and financial stability functions of the central bank, innovate financial instruments, and maintain financial market stability.” This clearly outlines the general operational approach of moderately loose monetary policy.

First, continue to reduce the statutory reserve ratio for deposits. Although the central bank has reduced the statutory reserve ratio for deposits more than 20 times, there is still considerable room for further reduction. In fact, many central banks in developed economies around the world have already abolished the statutory reserve requirement system. Even in countries that still maintain the system, the statutory reserve ratio is very low. There are multiple reasons for this. For example, the implementation of capital adequacy regulation for all commercial banks has imposed constraints on credit extension by commercial banks. Even in the absence of a statutory reserve requirement, commercial banks cannot expand credit indefinitely. In addition, multiple crises have shown that the statutory reserve ratio is also difficult to ensure that commercial banks in liquidity distress can obtain sufficient liquidity and means of repayment in a timely manner, and ultimately have to rely on the central bank’s lender of last resort mechanism for assistance. Currently, the statutory reserve ratio for large commercial banks in China is 9.5%, and for small and medium-sized commercial banks, it is 6.5%. In the future, commercial banks as a whole still have at least 4.5 percentage points of room for reserve ratio reduction, because the amount of deposits absorbed and the volume of credit provided by large commercial banks in China account for the vast majority.

Secondly, the total amount of central bank loans is complemented by structural tools. Between the expansion of total central bank loans and the reduction of the statutory deposit reserve ratio, moderately loose monetary policy should prioritize continuing to lower the statutory deposit reserve ratio. Due to the very low interest rates that the central bank pays on statutory deposit reserves to financial institutions, it increases the opportunity cost for commercial banks, which will inevitably pass on the costs to borrowers. Although reducing the statutory deposit reserve ratio is the preferred policy tool option for moderately loose monetary policy, the role of central bank loans remains very important. The central bank will still increase the total supply of liquidity through refinancing and guide the allocation of financial institutions’ credit resources with various structural monetary policy tools. However, it is necessary to prevent some enterprises from arbitraging the preferential interest rates of structural monetary policy.

Third, increase the amount of government bond purchases in open market operations. Unlike central banks in other advanced economies that hold a large amount of government bonds, the proportion of government bonds held by the central bank of our country is extremely low compared to its total assets, which actually hinders the central bank from guiding market interest rates and managing expectations through monetary policy operations. In 2024, the central bank of our country began to reattempt open market operations on government bonds, but the scale was very small, with limited impact on the total liquidity. In order to better implement moderately loose monetary policy, the central bank should increase the repurchase transactions of government bonds in open market operations. Given the relatively low ratio of government bond balance to GDP in our country, if necessary in the future, the central bank may even consider purchasing a part of low credit risk provincial general bonds as a supplement to the central bank’s government bond operations in the open market, in order to better manage the total liquidity.

Finally, as a researcher, the author has always advocated for the abolition of the benchmark interest rate for loans and deposits. Since 2015, China has not adjusted the benchmark interest rate for loans and deposits. In fact, the LPR has long replaced the central bank’s benchmark interest rate for loans and deposits and become the new interest rate benchmark for commercial bank loans. The central bank is also guiding the 7-day reverse repurchase rate to become the main policy rate in monetary policy operations, but at the same time, it still retains the benchmark interest rate for loans and deposits, which is a planned economy relic, which is inconsistent with the market-oriented reform of the Chinese economy. After the market interest rates have experienced an almost 5-year-long downward cycle, and both loan interest rates and bond market yields are at the lowest level since the reform and opening up, continuing to retain the benchmark interest rate level from 9 years ago is not appropriate. It does not reflect changes in the liquidity conditions of the macroeconomy and financial markets, nor does it convey monetary policy intentions.

! [Photo.com_500951529_Online Virtual Currency ( Non-Enterprise Commercial ).jpg](https://img.gateio.im/social/ moments-50d9506e1a52aa42469740a08cb12551)

0****3 Possible Impact of Moderately Loose Monetary Policy

There is no doubt that a moderately loose monetary policy will have some positive effects on the macroeconomy and financial markets. **First of all, it will change the reserve structure of commercial banks, and the release and new liquidity of the central bank will affect the supply of loanable funds, and the abundant liquidity will keep market interest rates generally low for some time to come. In other words, China has entered an era of ultra-low interest rates, which is both the result of loose monetary policy and the natural result of macroeconomic operation. In view of the extremely low level of bond market interest rates and deposit and loan interest rates, this may lead to a readjustment of the financial asset structure of institutional investors and residents. In this sense, a moderately loose monetary policy will be conducive to the realization of the goal of “stabilizing the stock market” put forward by the Central Economic Work Conference.

In addition, the RMB exchange rate will make necessary responses according to changes in domestic economic fundamentals and the international environment. **After Trump’s re-entry into the White House, China’s exports are back under tariff pressure, and hedging tariff risks objectively requires a certain degree of exchange rate depreciation. At the same time, China’s persistently falling interest rates have further widened the interest rate gap between China and the United States, which will also put pressure on the RMB exchange rate. Of course, exchange rate fluctuations may in turn contain changes in the level of market interest rates, because exchange rate depreciation may certainly promote exports, but it will also weaken the competitiveness of the currency, which is in conflict with the need for a “strong currency” in the construction of a financial power.

However, China’s loose monetary policy also faces some challenges. First, the total amount of money and liquidity in China is already very abundant. As of the end of November 2024, the balance of China’s broad money M2 has approached 31.2 trillion yuan, exceeding 200% of GDP, making China the economy with the largest total money supply in the world. This itself indicates that the difficulties and challenges facing the Chinese economy at present are not the result of insufficient money supply. We can clearly see that although the broad money M2 still maintains a significant positive growth, the balance of demand deposits held by non-financial enterprises has been continuously decreasing, indicating that the demand for money held by enterprises based on business motives is insufficient.

Second, at the end of 2023, China’s macro leverage ratio has reached around 350%, and the debt stress that China faces today is closely related to the debt risk of some local governments, to some extent, with past monetary and credit expansion, so moderately accommodative monetary policy must weigh credit expansion against future credit risk.

**Third, the difficulties and challenges facing the Chinese economy at present are the result of the inherent laws of economic development, especially the economic difficulties brought about by the deep adjustment of the real estate industry. It is the result of changes in the supply and demand pattern of the real estate market and the qualitative change in the industrial cycle. It is impossible to expect the real estate industry to re-enter the era of rapid expansion of about 20 years after the new millennium through moderately loose monetary policy. At the same time, the adverse impact of global trade and geopolitical changes on China also seems to require a considerable amount of time to digest.

Moderately loose monetary policy is just a temporary measure. **In order to achieve the goals of “stable growth” and “stable investment,” it is more necessary to deepen reforms and improve the market economy system to enhance confidence while implementing a moderately loose monetary policy, especially the confidence of private entrepreneurs in the future, enabling them to invest with courage, peace of mind, and confidence. This requires truly and effectively “protecting the legitimate rights and interests of enterprises of all ownership types equally in accordance with the law,” ensuring that enterprises of all ownership types can compete fairly without discrimination. To achieve this, government departments at all levels need to fully understand the operation and laws of the socialist market economy, learn to better engage with the market economy, and “confine power within the framework of the system,” with power serving the fair competition of the market rather than overriding it.

In addition, in order to enhance the effectiveness of a moderately loose monetary policy, China needs to better integrate with the global economy.