Coinbase CEO Brian Armstrong opposes bank lobbying to amend the “GENIUS Act,” emphasizing that stablecoins must not be interest-bearing and viewing this as a red line in cryptocurrency regulation that cannot be crossed.

As the banking sector intensifies lobbying efforts to curb competition from stablecoins, Coinbase CEO Brian Armstrong has set a firm bottom line, opposing any attempts to revisit the recently passed “GENIUS Act” and marking this as a “red line” for the crypto industry.

Brian Armstrong issued a stern warning to major U.S. banks that any attempt to lobby Congress to amend the “GENIUS Act” to allow banks to issue interest-bearing stablecoins would cross Coinbase’s “red line” and trigger widespread opposition. He accused banks of using political pressure to block competition from stablecoins and fintech platforms.

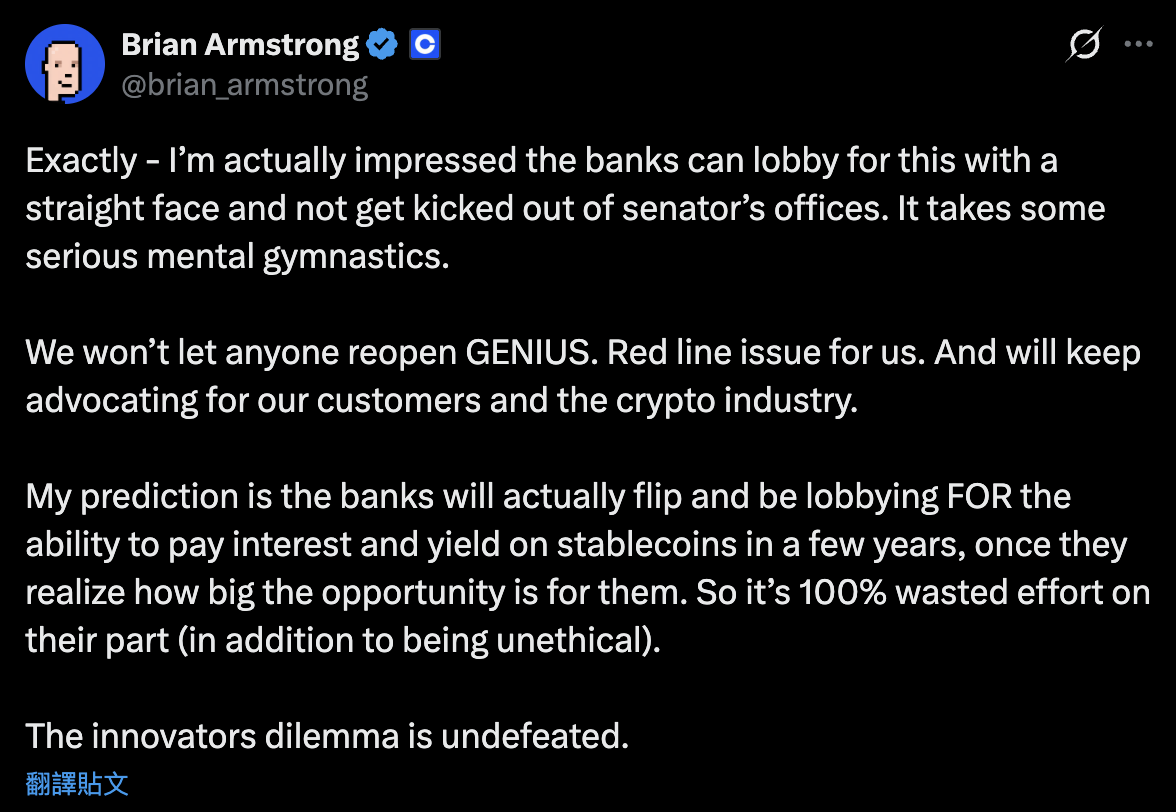

In a post on X, Armstrong criticized traditional banks for actively lobbying Congress to amend the legislation, stating that this would stifle innovation in fintech and digital assets. He expressed being “impressed” by banks now publicly lobbying Congress to block competition from stablecoins and fintech platforms, and added, “We will not let anyone revisit the GENIUS.”

In the increasingly tense environment between crypto innovators and traditional finance, Armstrong believes banks are trying to dominate the stablecoin market, which he predicts could grow to trillions of dollars in value. Although Coinbase is collaborating with top banks on pilot projects for stablecoin custody and trading, it remains wary of existing institutions seeking unfair advantages.

Bank lobbying targets stablecoin “Rewards”

The “GENIUS Act,” after lengthy negotiations, was enacted earlier this year. Passed by the U.S. Senate in early 2025, it established the first federal stablecoin framework, requiring stablecoins to be backed 1:1 by high-quality assets like U.S. Treasuries, and prohibiting interest payments to holders to prevent bank deposit outflows.

Banks have consistently lobbied against stablecoin rewards offered by platforms like Coinbase (currently 4.1% for USDC), claiming these rewards threaten community deposits and lending capacity. Armstrong dismisses these as “false threats,” comparing them to past resistance to ATMs and online banking, and predicts banks will soon see stablecoins as a huge opportunity rather than competition.

Image source: X/@brian_armstrong

Armstrong’s comments respond to a banking industry initiative report aiming to expand the scope of bans to include “indirect revenue sharing,” effectively limiting the competitive advantage of stablecoin platforms.

Max Avery, a board member of Digital Ascension Group and a vocal critic of banking practices, pointed out that banks currently earn about 4% on reserves held at the Federal Reserve, while offering near-zero returns on consumer savings accounts. In contrast, stablecoins enable platforms to pass on earnings, threatening banks’ profitable interest margins. Avery dismissed the banks’ arguments about “community bank deposits” and “system security” as unfounded, citing independent research indicating small institutions are not experiencing disproportionate fund outflows.

Armstrong predicts that banks will eventually change their stance and, recognizing the market potential, will advocate for allowing interest and yield payments on stablecoins. He describes the current lobbying efforts as “100% a waste of effort (and also unethical) for them.”

This conflict highlights broader tensions between traditional finance and the emerging crypto sector. Driven by payments, remittances, and decentralized finance (DeFi) use cases, stablecoin market capitalization has surged past $300 billion this year. The regulatory clarity brought by the “GENIUS Act” is seen as a milestone, but amendments could delay implementation and hinder investment.

U.S. lawmakers propose tax breaks for stablecoin payments

Additionally, in the legislative landscape, last week, U.S. Representatives Max Miller and Steven Horsford introduced a discussion draft aimed at reducing tax burdens for crypto users. The proposal would exempt small transactions (up to $200) involving regulated, dollar-pegged stablecoins from capital gains tax, and allow the deferral of income from staking and mining rewards for up to five years. If successful, this could further promote stablecoin adoption by reducing compliance barriers for everyday users.

As the crypto market approaches 2025 with liquidity scarcity and Bitcoin holding around $87,000 in volatility, industry leaders like Armstrong are signaling readiness to defend hard-won regulatory gains. Any efforts to revisit the “GENIUS Act” could escalate into a high-stakes game between Washington fintech innovators and entrenched banking interests.

Globally, stablecoin adoption is surging, with Coinbase projecting a market size of $1.2 trillion by 2028, and Citibank forecasting up to $4 trillion in a bullish scenario by 2030. In Taiwan and other regions, regulators are also debating issues related to yields, bank participation, and financial stability. Armstrong foresees banks shifting to support cryptocurrencies once they recognize the “opportunity,” but Coinbase is prepared to oppose any amendments that tilt the competitive environment.

- This article is reprinted with permission from: 《BlockBeats》

- Original title: 《Coinbase CEO criticizes bank lobbying in Congress: Revisiting the “GENIUS Act” crosses the “red line”》

- Original author: Anfei

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.