Author: Castle Labs & Vincent

Translation: LlamaC

(Portfolio: Burning Man 2017, about Tomo: ETH Foundation Illustrator)

From the legend of searching for the Golden Fleece to the mines of South Africa, humanity has been endlessly pursuing this noble and mysterious treasure.

It seems to be captured sunlight, perhaps truly originating from the depths of the universe, because scientists believe that gold was born from the collision of dying stars, known as supernova explosions. Although most of the gold on Earth is sealed within the core, the remaining portion was brought to the surface by meteorites.

Throughout human history, gold has been the core hard currency in commercial activities.

If all the gold mined by humans were collected, it would form a cube with a side length of about 20 meters, weighing approximately 176,000 tons.

Such a vast wealth can be contained in a single warehouse, which is truly astonishing. While stocks, artworks, oil, or collectibles require vast physical space or management resources, gold possesses the unique trait of portability.

Gold has become the ultimate store of value because it bears no counterparty risk. It is the only asset that does not represent a liability owed to others. JP Morgan once said, “Gold is money; everything else is credit.” Its extremely high stock-to-flow ratio not only ensures scarcity but also shields it from arbitrary fiat currency devaluation. From ancient Lydia coins to modern central bank reserves, gold has maintained its status as a store of value for thousands of years, serving as a highly liquid and tamper-proof anchor amid financial, political, and social upheavals.

However, recently, a new contender has emerged vying for the title of “currency.”

Despite its volatility and cryptographic nature setting it apart from traditional precious metals, cryptocurrencies like Bitcoin are often called “gold killers.”

Bitcoin is frequently referred to as digital gold. Will it replace gold in the future? If so, is abandoning this ancient asset advisable?

This article examines gold and Bitcoin within the context of modern economics, decentralized finance (DeFi), and monetary properties. Subsequently, we will compare and analyze whether these two assets can coexist in a highly competitive macro environment, and assess current trends to determine if Bitcoin possesses the attributes of “digital gold.”

Ultimately, diversification of assets benefits the global economy. Fiat currencies—assets whose value largely depends on arbitrary monetary policies—are likely to be replaced by more pure forms of money. Whether it’s gold or some yet-to-be-invented new asset, they could escape the inherent devaluation fate of fiat money, especially given the fatal flaws in our current debt-dependent economic system.

The historical role of gold in finance

For centuries, gold has been the pillar of this system and the sole reserve asset. This status was not established by legislation but reinforced by the laws of physics of the universe. As former Federal Reserve Chairman Alan Greenspan famously testified in 1999: “Gold remains the ultimate form of payment in the world. In extreme circumstances, no one will accept fiat currency, but gold will always be accepted.”

Gold’s widespread acceptance stems from its intrinsic qualities, which distinguish it from all other materials. These qualities establish its enduring position as a store of value, what Aristotle called sound money:

- Durability: Gold is a noble metal that virtually does not react chemically. Unlike silver, it does not oxidize or tarnish, ensuring its physical properties remain stable over the long term. This unique chemical trait makes it reliable for economic reserves and high-tech infrastructure (such as electric vehicles, drones, defense systems, rockets). Additionally, gold does not rust.

- Interchangeability: Due to gold’s softness and ductility, it is easy to shape, cast, and divide. This allows gold to be standardized into interchangeable coins or bars, as long as weight (traditionally ounces or grams) and purity (most commonly 14k, 18k, and 24k) are consistent. One unit of gold is essentially identical to another.

- Stability: Gold is a reliable store of value. Its scarcity and practicality (despite high costs, it remains the best choice for critical industrial applications) enable it to retain value over time, unlike fiat currencies which are subject to inflation. Moreover, gold as the ultimate store of value bears no counterparty risk.

- Portability: As a dense, expensive metal, even small quantities of gold have high value. This super-high value-to-weight ratio makes it easy to transport large sums of wealth efficiently—unlike silver, art, or other bulk commodities. A person can carry half a kilogram of gold in their pocket.

- Recognizability: Gold’s unique physical properties make it relatively easy to verify authenticity. Modern instruments like Sigma detectors can instantly identify fake gold.

Therefore, gold is a perfect store of value—except for one case. Gold is not a replaceable credit card nor a line of code. Transporting gold, even for ordinary citizens holding small bars, is as troublesome as transporting uranium; if customs officials forget to fill out declaration forms, they have the authority to seize the gold and confiscate most of it as a fine. It can be stolen, cut, hidden, misappropriated, and so on. Due to human error, it can also be lost.

The famous “Operation Fish” in 1940 exemplifies this logistical nightmare. As Nazi Germany advanced, to prevent the enemy from seizing its gold reserves worth £2.5 billion, Britain was forced to secretly ship its gold to Canada—becoming the largest physical wealth transfer in history. Today, just a click of a mouse can transfer trillions of dollars instantly.

The most notorious example of state plunder is Franklin D. Roosevelt’s Executive Order 6102 in 1933, which made it illegal for U.S. citizens to hold monetary gold. Unlike passwords or mnemonic phrases, you cannot store gold in your memory; it must be physically held, and once found, it can be stolen. Gold offers no yield, pays no dividends, and incurs high storage and insurance costs. Most of the world’s gold is stored in vaults in London, Switzerland, Singapore, or Manhattan—like an ancient, forgotten mythic sphinx, quietly lurking in darkness.

Indeed, because humans are prone to mistakes yet ingenious, they will inevitably come up with a better alternative than that “prehistoric relic.” While gold itself is nearly perfect, the astonishing evolution of our financial system makes creating a modern substitute necessary. Born out of disappointment with outdated traditional finance access mechanisms and a desire to overhaul them, Bitcoin was originally invented to challenge the existing system. However, it quickly pioneered a powerful new paradigm far beyond its initial intent: the potential to be regarded as the digital equivalent of gold!

The advent of cryptocurrencies

In 2008, during the global financial crisis, Satoshi Nakamoto published the white paper titled “Bitcoin: A Peer-to-Peer Electronic Cash System.” This paper proposed a solution to the double-spending problem without relying on centralized trust institutions.

If gold is inherently money, then Bitcoin is money created through computer engineering. It is scarce, difficult to mine, has a limited total supply, and is virtually indestructible. The invention of blockchain triggered a “Cambrian explosion” of digital assets, some interesting, some worthless.

While Bitcoin quickly established its status as “digital gold” with a fixed supply of 21 million coins, other tokens emerged to fill various economic niches.

In 2011, Litecoin positioned itself as “Bitcoin’s silver,” promoting faster, lower-cost transactions. In 2015, Ethereum introduced the concept of the “world computer,” replacing gold’s passive store of value with active, programmable smart contracts. Today, it is the second-largest cryptocurrency by market cap, despite disappointing price performance, its position remains unshaken. Privacy tokens like Monero (XMR) and Zcash (ZEC) attempt to replicate the anonymity of cash and gold, features lacking in Bitcoin’s public ledger. This year, driven by privacy narratives, they experienced a surge amid the collapse of traditional tokens.

When competing coins, mainstream coins, and Bitcoin all declined, ZEC and subsequently Monero began a rally, costing many bears dearly. However, the total market cap of these tokens remains insignificant, not posing a serious challenge to Bitcoin.

Finally, high-performance blockchains like Solana or MegaETH sacrifice decentralization for speed, aiming to match Nasdaq’s transaction processing speeds rather than traditional wire transfer speeds. While they have attracted entrepreneurs, institutional investors, and banks, the current landscape of Layer 1/Layer 2 solutions has become so vast that it’s hard to say which will survive. The core narrative of the 2010s was not coexistence but mutual destruction, as each new trend erases the old.

The industry’s fervor to erase precious metals was perfectly embodied in the controversial 2019 Grayscale “Drop Gold” ad campaign. It depicted gold investors as burdened with heavy stones (shiny rocks), exhausted suits, while trendy millennials carried digital wealth rushing past them.

Gold is heavy, tangible, and primal, while cryptocurrencies are lightweight, digital—simply put, the money of the future. However, when Bitcoin largely remains a fringe geek asset, the claim that “gold is dead” is probably just a cheap marketing stunt lacking real consideration. Yet, after the COVID-19 outbreak, the public blindly accepted this narrative. Although Grayscale took time to clear its name, the next Bitcoin cycle gave them reason.

This renewed appetite for risk assets shows that scarcity can be engineered, not just mined.

It remains unclear whether this artificially created, human-designed commodity should replace physical assets in the eyes of sovereign nations, but the 2020s performance suggests investors have already bought into it.

The maturation of Bitcoin

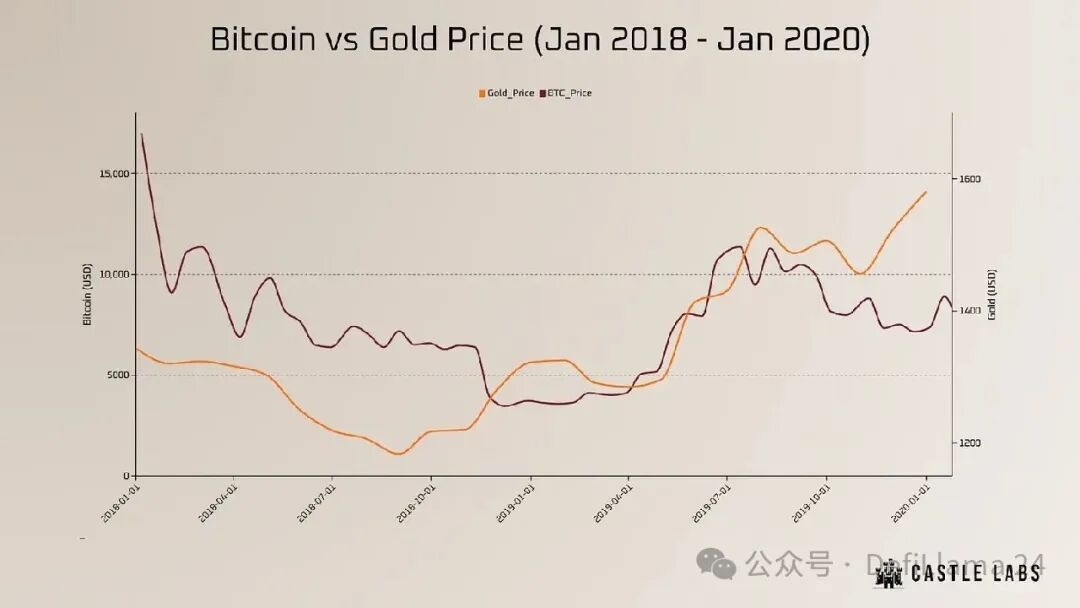

Between 2010 and 2025, Bitcoin emerged from the mysterious world of cypherpunks to become a hot topic on Wall Street, transforming from a worthless novelty to a giant worth trillions of dollars. These fifteen years have not been smooth, but whenever Bitcoin crashes, it always recovers and hits new highs.

The media has been deeply skeptical, declaring Bitcoin “dead” about 450 times. Thus, this narrative arc is far from straightforward. The story begins with retail frenzy in 2017, when some even sold their houses to buy more Bitcoin. Driven by retail hype, ICO speculation, and perhaps a general reckless mindset, Bitcoin soared from under $1,000 to nearly $20,000. But it collapsed the same year, dragging down the entire crypto market (which at the time seemed to have been completely finished).

In the macro hedge era of 2020, driven by legends like Paul Tudor Jones and Michael Saylor, this controversial asset was reignited. Bitcoin found its champions and became a macro asset capable of challenging gold. The real breakthrough came in January 2024, when the U.S. Securities and Exchange Commission (SEC) approved a spot Bitcoin ETF.

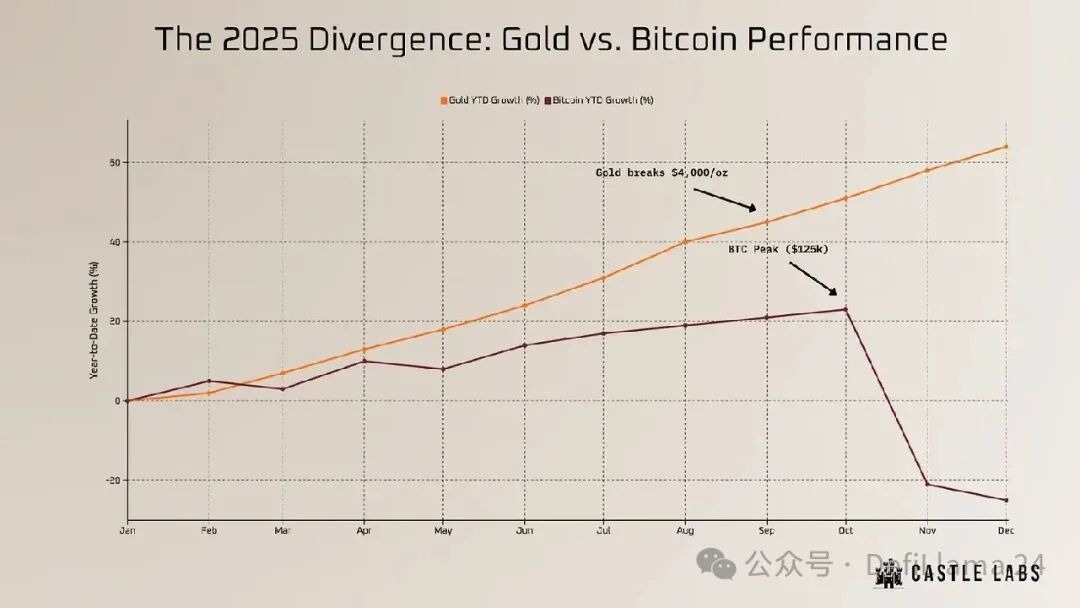

In just 15 years, Bitcoin evolved from a libertarian internet token into an ETF capable of moving tens of billions of dollars in regulated funds. BlackRock, Fidelity, and VanEck ultimately became its advocates; those once hiding in basements are now billionaires, and their previous anti-capitalist ideologies may have been abandoned for yacht purchases. Institutional acceptance pushed Bitcoin past the $100,000 psychological barrier in December 2024, culminating in a peak of $125,000 in October 2025. At that moment, the supercycle theory seemed irrefutable. The U.S. even explored strategic Bitcoin reserves, delighting crypto traders.

However, in October, Binance’s USDe pricing glitch caused a cascade of leveraged long positions to collapse. Although the market rebounded shortly after, the previous price shadow was eventually filled, and Bitcoin entered a slow decline, approaching a critical level; whispers of a drop to $67k began circulating. The seemingly endless cycle suddenly took a different turn at the end of 2025.

While Bitcoin hit new highs, blue-chip projects like Aave, Ethereum, Solana, and Ethena never regained momentum. Bitcoin remained undefeated, but its relative strength did not translate into broad market support. This divergence reinforced Bitcoin’s status: it is not only a novel asset but also a reliable, durable one.

Through absolute scarcity and especially its first-mover advantage, Bitcoin successfully replicated the monetary premium of precious metals. Unlike fiat currencies prone to endless devaluation, Bitcoin offers a decentralized beacon with durability, divisibility, and instant portability. Despite its immature stage and high volatility, it effectively digitizes the inherent qualities of gold and monopolizes its class of assets.

By November 2025, a brutal correction pushed Bitcoin back to $80,000, dragging the rest of the market down. What was frustrating was that stocks, gold, silver, collectibles, and all assets in between experienced parabolic rises. Has the crypto sector, especially assets other than Bitcoin, truly completed its cycle?

Are we trading real money promises for an ETF ticker and a pump-and-dump spectacle? Is the institutional narrative just marketing hype? An asset that is regulated, taxed, and tightly monitored now seems even more boring than gold, unable to keep pace with the market.

Gold prices surged parabolically, followed by silver, and even copper—the cheap metal used in electronics and weapons manufacturing—has gone out of control.

Has gold always been the only stable currency?

The triumph of gold in 2025

Despite Bitcoin meeting the criteria of sound money, recent developments suggest it has yet to exhibit the properties of digital gold.

In 2025, as a tool for hedging inflation, geopolitical turmoil, and war, gold outperformed Bitcoin as an investment.

The global gold frenzy is characterized by large-scale accumulation of official reserves, with Poland’s aggressive buying, along with continued purchases by the Reserve Bank of India, Turkey, and China leading the trend. Brazil joined at the end of the year to diversify assets. Although central banks shifted their gold strategies from the West to the East, China and India’s demand for jewelry and physical gold bars remains the highest, followed by the U.S., Turkey, and Iran—citizens of these countries use gold as their preferred hedge against currency devaluation and economic instability.

In 2025 alone, currencies in Turkey, Argentina, and Iran hit record lows. If you think this rally is over, institutional attitudes have shifted from “gold is dead” to “gold will rise to $5,000.” VanEck has already published that ongoing geopolitical turmoil, fiscal instability, and inflation could push gold prices to $5,000 per ounce before 2030, and undervalued gold mining stocks will inevitably explode. JPMorgan Chase predicts that driven by a non-transitory structural shift, the average gold price will reach $5,055 per ounce by the end of 2026.

The bank highlights two main reasons for this rally:

- Central banks accelerating gold purchases (continuing the 2025 trend) to diversify assets and reduce dependence on the dollar;

- The Federal Reserve’s rate cuts triggering a wave of Western ETF capital inflows.

Gold is actively traded as a hedge against currency devaluation and inflation, reaffirming that ancient customs may indeed stem from wisdom. Gold is indeed a way to bet on fear. For cryptocurrencies, increasing regulation worldwide—from the EU’s Markets in Crypto-Assets (MiCA) regulation to aggressive crackdowns on privacy coins and non-compliant stablecoins by the U.S. Treasury—reflects this trend. Ultimately, illusions shatter.

Because we are still in a turbulent transition, assessing the current situation is quite difficult. Cynics might say that the test of Bitcoin as “digital gold” has failed, and we are merely returning to the mean. After long experiments, in the eyes of public and private institutions, Bitcoin has not passed the “sound money” test. While these institutions hold a positive view of the “digital gold” concept, they ultimately tend to revert to familiar, reliable assets held extensively by central banks.

For risk-averse investors, traditional gold’s relatively stable price might be another advantage over Bitcoin; although precious metals’ prices fluctuate with the global economy, they rarely crash dramatically. Part of the reason is that influencing the price of such a large asset— even for institutions with enough capital to move markets via derivatives—is extremely difficult. Moreover, most of gold’s market value is dormant (jewelry, central bank vaults, private holdings) and not actively traded.

Conversely, Bitcoin is naturally leveraged by retail and institutional traders to capture intraday volatility. Compared to physical commodities with inertia, it’s much easier to manipulate an asset whose price is driven by dynamic liquidity. Although investors believe in the inflation hedge narrative, Bitcoin’s performance resembles an immature asset characterized by high volatility and unpredictable swings. The expected performance of a reserve asset does not match Bitcoin’s actual behavior.

Various stablecoins’ de-pegging fears remind us: if you don’t hold it physically, you don’t truly own it.

On one hand, gold is the ultimate tangible asset; on the other hand, it’s difficult to store.

It would be premature to outright dismiss Bitcoin, but it’s also shortsighted to consider gold as the only sound currency in the digital age.

Currently, the bulls have retreated, but it’s the “Baby Boomer” generation that has taken all the profits. It’s fair to say that after 15 years of maturation and frenzy, Bitcoin has not demonstrated the properties of a reserve asset. Meanwhile, a titan that has ruled our imagination, senses, and desires for thousands of years is destined to awaken from its slumber someday.

Dethroning Bitcoin: a formidable task

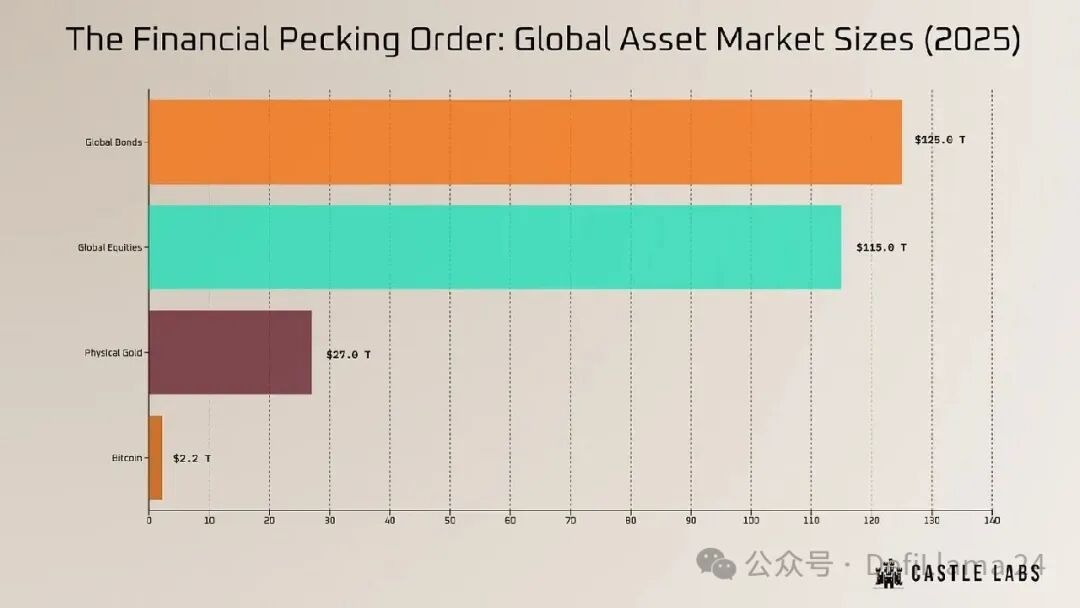

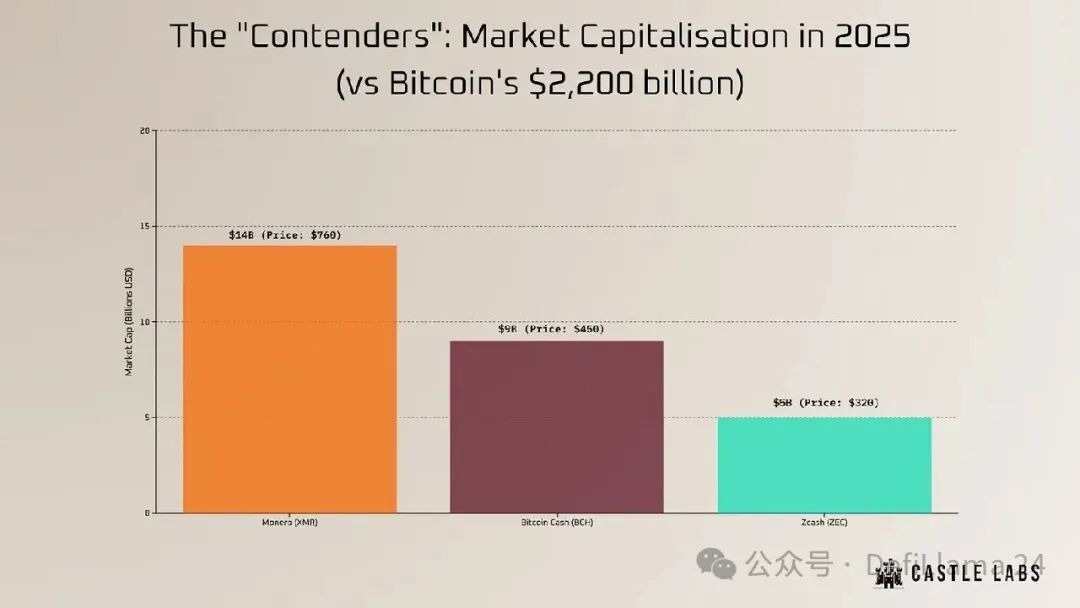

The idea that privacy coins or Bitcoin forks could replace gold as a global store of value resurged at the end of 2025, but data reveals a different reality: although gold has a market cap of about $32 trillion, the combined market cap of Monero and Zcash struggles to break through $20 billion—roughly a tiny fraction of gold’s value, often only appearing as a small peak in their ceiling fluctuations (like Nvidia).

In Q4 2025, Zcash briefly attracted attention in the crypto Twitter circle—not for its sound money properties, but due to a narrative shift: amid a wave of compliance-driven washouts of privacy assets on exchanges, Zcash survived thanks to its auditability under the EU’s MiCA framework and the U.S. GENIUS Act. Moreover, Solana’s founders launched a marketing blitz, sparking a somewhat spontaneous ZEC buying frenzy.

Compared to gold, silver, stocks, or private equity, such price movements are hard to call stable money; they resemble more a “pump-and-dump” scheme. Conversely, privacy coins in 2025 became regulated contraband. They satisfy niche demands of short-lived narratives but may be insignificant in the current boom-and-bust cycle. Even fears of surveillance and potential state intrusion trigger sporadic rebounds, but these tokens cannot attract the sustained institutional capital that cryptocurrencies are currently trying to absorb.

Ironically, tokens designed to evade institutions may only survive by relying on the very funds held by those institutions, but long-term survival comes at the cost of transparency. Funds and banks supporting assets meant to bypass them are unimaginable. These alternatives cannot withstand the test of sound money: Bitcoin Cash, for example, lost its “store of value” narrative years ago; it is a payment network more or less forgotten by institutions and retail alike. With the rise of stablecoins, Bitcoin Cash has become irrelevant, replaced by capital-rich tokens designed specifically for payments.

Having undergone two forks and lacking community attention, Bitcoin Cash appears insignificant compared to Bitcoin. The value of Zcash lies in its privacy. Any sovereign nation cannot base reserves on assets that are heavily regulated or highly volatile. Such tokens are tools for private transactions, not for public treasuries, because they lack the liquidity and stability needed to replace the $32 trillion gold market.

Although Zcash has a cap of 21 million coins, despite this attractive and familiar feature, it still lives in Bitcoin’s shadow. Monero (XMR) is an alternative to Zcash, but Monero’s privacy is mandatory. In terms of scarcity, the fixed amount of newly minted XMR (0.6 per block) and the increasing total supply cause inflation to continually decrease, approaching 0%, but never fully reaching it.

At least in this aspect, Monero is more like physical gold than Bitcoin, with a stable, low annual inflation rate similar to gold (mined new gold). However, XMR cannot replace gold as a reserve asset because it lacks auditability. Its ledger is opaque; without leaking private keys or destroying the privacy features that sustain the token, it cannot prove reserves to the public. Conversely, central banks require public trust and transparency for their reserves, even though actual accountability of U.S. and Chinese reserves remains controversial.

From the above analysis, we conclude: structurally, only Bitcoin can theoretically replace gold. It has withstood the test of sound money, is well-capitalized, and widely recognized at both institutional and individual levels.

Despite ongoing competition, Bitcoin has clearly established itself as the core of cryptocurrencies. It is the only digital asset recognized legally by the U.S. government: in March 2025, the U.S. issued an executive order officially designating confiscated over 200,000 BTC as a national asset, rather than auctioning it, thereby establishing a Bitcoin Strategic Reserve (SBR).

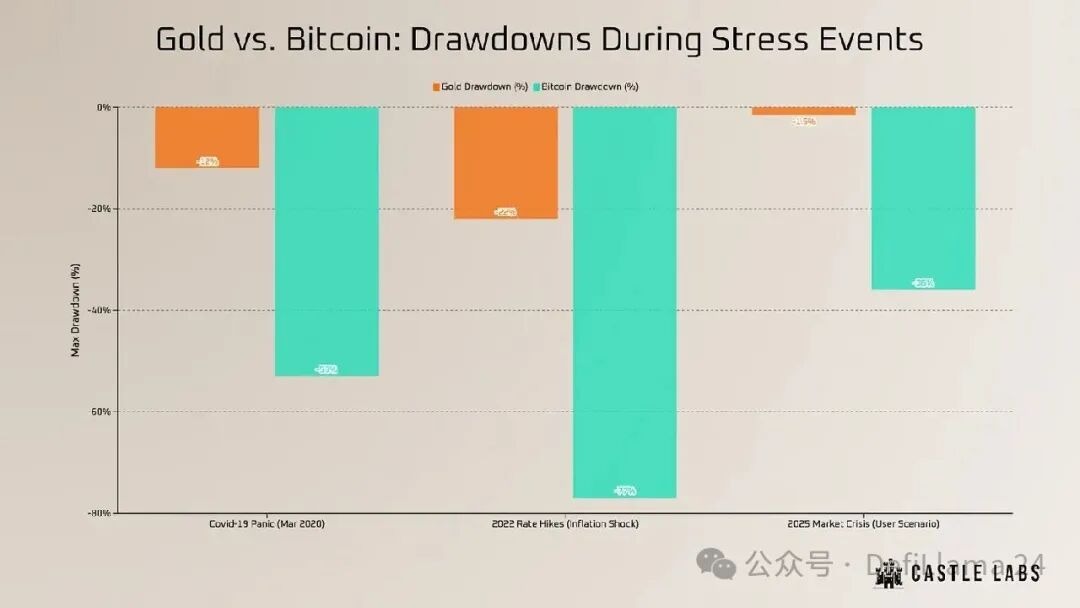

This grants Bitcoin legal legitimacy, and other countries like El Salvador (about 6,000 BTC) and Bhutan (mining about 13,000 BTC via hydropower) have also established more or less officially recognized SBRs. Currently, no other asset enjoys the support of governments worldwide like Bitcoin. However, replacing gold remains an unrealistic fantasy—not only because of Bitcoin’s extreme volatility (in 2025, Bitcoin’s annualized volatility hovered around 45%, three times that of gold’s 15%) but also because its current market cap is tiny compared to gold and silver. Sovereign nations need deep liquidity and large buffers to support their monetary policies; unless Bitcoin recovers and reaches $1 million per coin, it will never have the dominance of gold.

The best of both worlds?

For fifteen years, the fiercest debate has revolved around the conflict between massive precious metals and ambitious digital assets—namely, gold versus Bitcoin. A series of events in 2025 temporarily paused this debate: gold remains true money, while Bitcoin remains a risk asset. If its high volatility prevents Bitcoin from crashing to a level requiring caution, then, without exception, the entire ecosystem suffers significant losses. Gold reaffirmed its status as the “kingly wealth” with thousands of years of history. It is a national asset, an ultimate insurance that requires no electricity, internet, or permission to use.

Through large-scale purchases of gold by Poland, China, and Brazil, and ignoring Bitcoin’s behavior, we see that during turbulent times, gold remains the most sought-after commodity. Bitcoin, on the other hand, has matured into an asset with a high beta coefficient and an appearance of institutional authority.

Most importantly, this asset is suitable for traders who profit from its two-way, highly volatile swings. Its high volatility, portability, and liquidity enable capital to be “teleported” across borders in seconds, bypassing the outdated and sluggish traditional banking system. Although Bitcoin’s image as a frontier asset has weakened, gold’s reputation as the “king of assets” has become even more solid: it was the undisputed winner in the past year. The extremely difficult task of replacing gold has always been just a marketing gimmick. What the entire financial system needs now is coexistence, especially considering that Bitcoin has spawned a trillion-dollar industry dependent on its steady development.

Nevertheless, cryptocurrencies remain the explosive assets we relentlessly pursue. In turbulent times ahead, cautious investors will not choose between gold and code, because they are fundamentally incompatible. If gold is the generational wealth for building family dynasties and empires, then Bitcoin is that quirky, unpredictable asset—sometimes seemingly crazy, yet irresistibly captivating. Whether it can transform into the reserve asset we hope for will only be revealed after more stress tests and years of trial and error.