Why Wallet Project Shutdowns Are a Wake-Up Call for the Crypto Industry

Image credit: Official Statement from ME

Image credit: Official Statement from ME

When a wallet project shuts down, the immediate reaction is often, “Yet another product that couldn’t survive.” But if you take a step back and look at the bigger picture, these events reveal far more than just a single team scaling back its operations.

Wallets have always been one of the most crucial gateways in Web3. They’re not just for transfers and signatures—they serve as the first interface for users to access on-chain assets, DeFi, NFTs, identity systems, and payment networks. Whoever controls the wallet controls the flow of users, transaction distribution, and the accumulation of assets.

Because wallets have been assigned such high expectations, the growing number of wallet products shutting down, going offline, or moving to export-only modes should prompt the industry to ask a serious question: Are wallets still a sustainable standalone business?

What Recent Wallet Closures Really Mean

The most notable recent example is the exit of Magic Eden Wallet.

According to the official Magic Eden Help Center, starting March 13, 2026, Magic Eden Wallet will move to export/withdraw-only mode, and as of April 1, 2026, the wallet and related account wallets will no longer be supported. This timeline makes it clear that this isn’t just a minor feature adjustment—the project is systematically winding down its wallet operations.

The significance of these events goes beyond a single brand closing a product. They highlight a broader reality: even wallets with strong transaction use cases, an NFT user base, and solid brand recognition can be abandoned if they fail to establish a competitive edge in the broader ecosystem.

Wallet project shutdowns send three clear signals:

- The strategic priority of wallet products is falling.

- The “gateway value” logic alone can no longer justify long-term investment.

- The market is redefining the wallet’s role—it’s no longer naturally the best form for an independent project.

Wallets Are Still Essential, but Independent Wallets Face Steep Challenges

A common misconception is that “wallet project shutdowns” mean wallets are no longer important. In fact, wallets remain as critical as ever—perhaps even more so.

The issue isn’t whether wallets are valuable, but whether independent wallet teams can still capture that value on their own.

In recent years, the industry has treated wallets as the super gateway to Web3. The logic was simple: if users start with the wallet, then transactions, asset management, DApp distribution, advertising, Earn referrals, and payments all follow. Many projects aimed to make the wallet the starting point for user traffic, hoping to secure the entry and then gradually monetize.

But in reality, being the gateway doesn’t automatically mean profit. Users care most about security, convenience, stability, and low friction—not brand loyalty. As long as switching costs are low and assets are exportable, users can switch wallets at any time. This makes it hard for independent wallets to build the kind of strong moat seen in traditional internet platforms.

In short, wallets are essential—but “essential” does not mean “easy to monetize.”

Why Web3 Wallet Business Models Are Harder Than Ever

Most wallet projects ultimately rely on several common revenue streams: swap trading fees, aggregator transaction sharing, ad placements, Launchpad, partnership referrals, staking or Earn distribution, and a small amount from premium features.

The problem is, these revenue sources are highly unstable.

- Users rarely pay directly for basic wallet features.

Transfers, receipts, signatures, and asset viewing are basic public goods for wallets. If a wallet tries to charge for these, users will simply switch to alternatives.

- Trading and swap revenue is highly cyclical.

During a bull run, on-chain trading is active and wallets can earn from swaps, meme coin trends, and asset launches. But when the market cools and trading volume drops, wallet cash flow contracts quickly.

- Wallets are heavily dependent on external ecosystems.

Much of wallet revenue doesn’t come from unique value created by the wallet itself, but from referring users to other DeFi, NFT, or trading platforms. When market enthusiasm fades, wallets struggle to sustain their own revenue models.

This creates a tough reality: wallet revenues are cyclical, but costs are fixed.

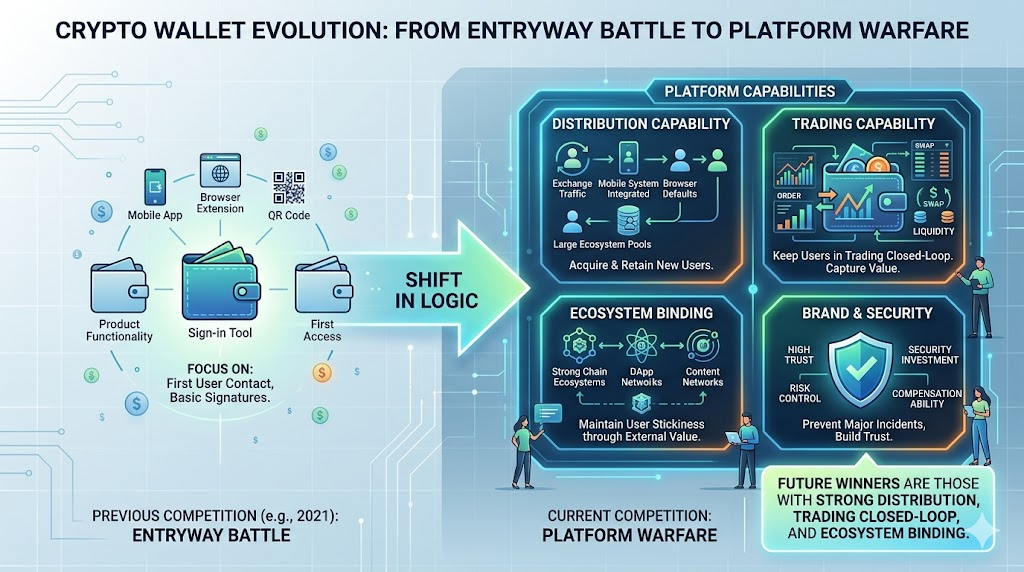

Today, the wallet industry’s competitive dynamics are nothing like 2021. The battle is no longer over who can secure the gateway first—it’s about who can build true platform capabilities. At a minimum, that means four things:

Today, the wallet industry’s competitive dynamics are nothing like 2021. The battle is no longer over who can secure the gateway first—it’s about who can build true platform capabilities. At a minimum, that means four things:

- Distribution: Who can consistently acquire new users? Is it exchange-driven traffic, mobile OS entry points, default browser extension slots, or large ecosystem user pools?

- Trading: Who can keep users within their own transaction ecosystem? If the wallet is just a signature tool, while trading, liquidity, and asset discovery all happen elsewhere, the wallet’s economic value is limited.

- Ecosystem Integration: A wallet without a strong chain ecosystem, robust app network, or powerful content distribution will struggle to maintain user stickiness.

- Brand and Security: Wallets are high-trust products. Just one major security incident can trigger rapid user migration. Large platforms typically have the edge in security investment, compensation capacity, and risk control.

As a result, wallet competition is shifting from “product battles” to “platform wars.” In the future, the winners may not be the wallets with the most features, but those with strong distribution, closed trading loops, and deep ecosystem integration.

Security, Compliance, and Maintenance Costs Are Raising the Bar

Another often-overlooked challenge for wallet businesses is their cost structure.

On the surface, wallets seem lightweight: interface, addresses, assets, signatures, pop-up confirmations—none of it looks complex. In reality, wallets are critical infrastructure with immense security responsibility. They require ongoing investment in multi-chain support, node connections, signature logic, plugin compatibility, transaction simulation, malicious approval alerts, phishing protection, mobile compatibility, and version updates.

These costs aren’t one-offs—they’re ongoing.

As regulations evolve and user numbers grow, wallet teams face greater compliance and risk control pressure. Even if a wallet doesn’t custody user assets, it may still face operational complexity from aggregator trading, third-party integrations, risk management strategies, or regional restrictions. The result is a classic paradox: users expect wallets to be free, simple, and stable, but maintaining that standard requires long-term, heavy investment in engineering, security, and operations.

That’s why, when the market cools, wallet projects are often the first to be downsized or shuttered. It’s not that wallets aren’t important—they’re so important that only teams with the necessary scale and cash flow can withstand the pressure.

What Will the Surviving Wallets of the Future Look Like?

As the wallet sector consolidates, the survivors will likely have clear structural advantages.

Exchange-Backed Wallets

These naturally have user traffic, asset accumulation, transaction scenarios, and brand recognition. They can operate the wallet as part of a broader financial platform, without needing the wallet itself to be independently profitable.

Public Chain or Large Ecosystem Wallets

Backed by strong ecosystem content, users turn to these wallets not just for asset storage, but to access the main application network of a given chain.

System-Level or Default Entry Wallets

Whoever controls the browser, mobile device, payment tool, or super app entry point enjoys the lowest user acquisition costs.

Wallets with Clear Differentiation

For example, those focused on institutional custody, social graphs, account abstraction, native interactions with specific chains, or wallets with overwhelming security and user experience advantages.

In this sense, the future wallet won’t look like a standalone startup—it will be an interface layer within a larger ecosystem. It’s the first UI users see, but the real competitive edge lies in distribution, asset depth, trading capabilities, and platform resources.

Conclusion

The recent wave of wallet project shutdowns doesn’t mean wallets have lost their value. Rather, it shows that the Web3 wallet sector has moved beyond the “anyone can build a gateway” phase.

Wallets were once the most imaginative direction in the space—described as user portals, asset accounts, social gateways, on-chain identity containers, or even the starting point for the next-generation super app.

Now, the market is asking tougher questions: Can you retain users? Is there stable revenue? Can you cover security and maintenance costs? Do you have the platform capabilities to compete long-term?

The real signal behind wallet shutdowns is that the industry is moving from the entry-point myth to the reality of infrastructure. The wallets that survive will be fewer, but stronger—more stable, more robust, and more integrated with platforms.

For the industry, that’s not necessarily a bad thing. When a sector moves beyond the “everyone can build” stage, it usually means it’s entering a truly mature competitive cycle.