The Challenging Environment Facing Miners

The fourth quarter of 2025 marks the most difficult period for the mining industry since the Bitcoin halving in 2024.

Two primary factors contribute to this environment:

- Bitcoin Price Decline

In early October 2025, BTC nearly reached its historical peak of $124,500, but by the end of December, it had dropped to about $86,000—a fall of roughly 31%.

- Global Hash Rate Nears Record Highs

Intense hash rate competition has sharply reduced income per unit of hash power.

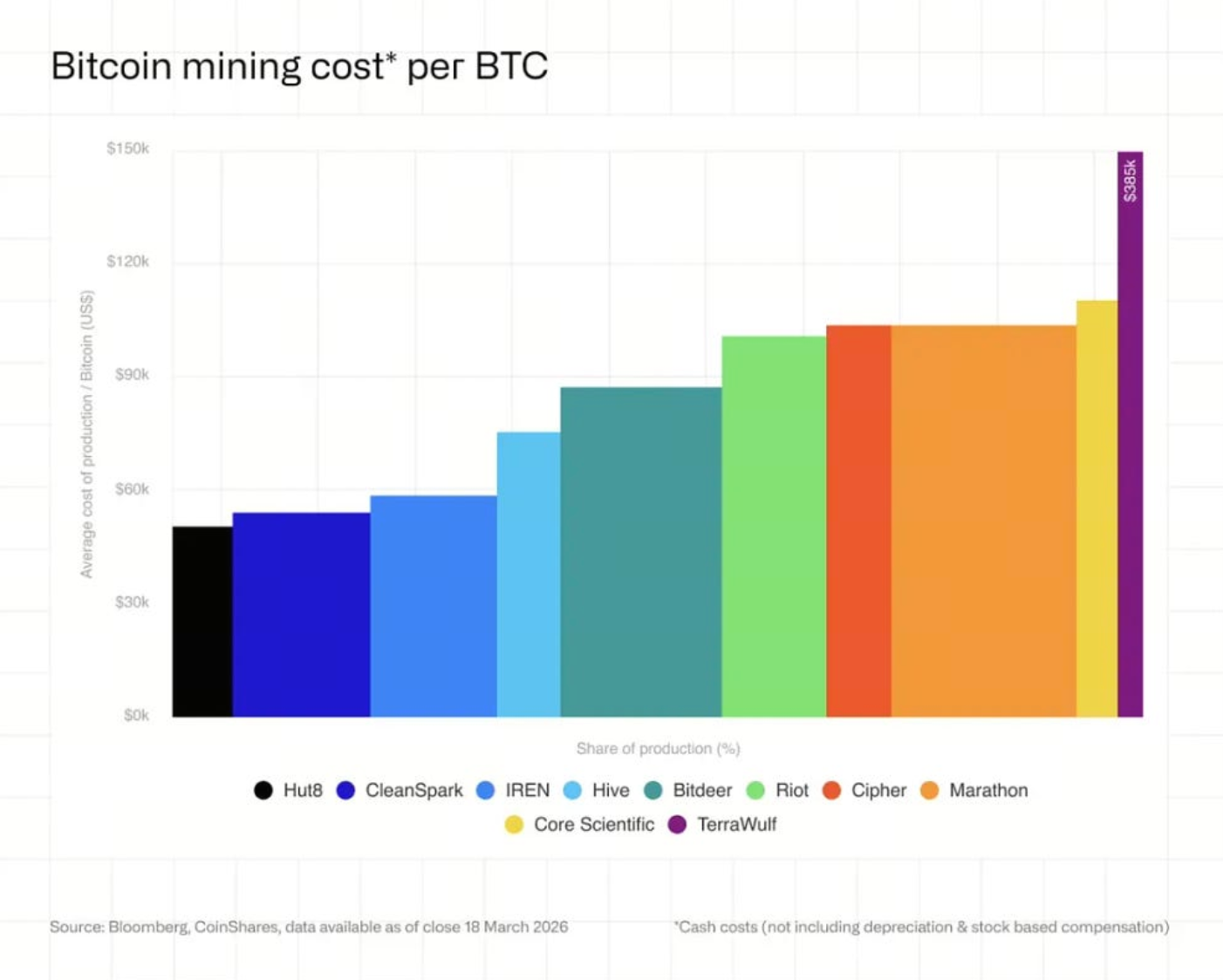

(Source: CoinShares)

(Source: CoinShares)

In this context, the average cash cost for publicly listed mining companies to produce one Bitcoin is approaching $80,000, significantly narrowing profit margins across many mining operations.

Three Key Trends Shaping the Mining Industry

Across the broader sector, three major shifts are evident in the fourth quarter of 2025.

- Mining Profits Continue to Compress

A critical metric for miners—Hashprice (hash rate price)—has dropped to around $36–$38 per PH/s per day. This level is near the breakeven point for many mining facilities. Additionally, network mining difficulty has been reduced three times in a row, a signal often interpreted as miner capitulation. Moving into 2026, hash price fell further to about $29, indicating persistent industry pressure.

- AI and HPC Drive Industry Transformation

More Bitcoin mining companies are redirecting data center resources toward artificial intelligence (AI) and high-performance computing (HPC).

The total announced value of AI/HPC contracts now exceeds $70 billion. Some miners are evolving into infrastructure firms combining mining and data center services—for example, Core Scientific, TeraWulf, Cipher Mining, and Hut 8. This approach means data centers are no longer solely dedicated to mining but also support AI computing workloads.

- Changing Capital Structures in the Industry

To build AI infrastructure, some mining companies are taking on higher liabilities.

Examples include:

-

IREN: About $3.7 billion in convertible bonds

-

TeraWulf: About $5.7 billion in debt

-

Cipher Mining: $1.7 billion in secured notes

High leverage is changing the risk profile of mining companies compared to previous years.

AI and Mining Compete for Data Center Resources

The rapid growth of the AI sector has made power and rack space in data centers increasingly valuable. Analysts estimate that by the end of 2026, AI revenue could account for as much as 70% of publicly listed mining companies' income (currently about 30%). What began as a secondary business—AI services—is now becoming a core revenue stream. Many miners are signing GPU hosting or cloud agreements with major cloud service providers, with contract totals already exceeding $70 billion.

Mining Companies Pursue Different Strategies

Not every mining operation is following the same path; three main business models have emerged.

- Transitioning to AI Infrastructure Companies

Some firms, like IREN and Bitfarms, view mining as a gateway to AI. These companies are gradually shifting resources toward GPU and AI computing services.

- Maintaining Mining as Core Business

Other companies, such as CleanSpark, continue to focus primarily on Bitcoin mining. Typically, these firms leverage their existing mining capacity before gradually exploring the AI market.

- Focusing on Low-Cost Energy Mining

Some miners opt to use extremely low-cost or intermittent energy sources, including:

For example, Marathon has deployed about 10 MW of small modular mining facilities that can operate during periods of unstable power supply.

This model is unsuitable for AI but remains economically viable for mining.

Cost Differences Between Mining and AI Infrastructure

The construction costs for mining and AI data centers differ significantly.

Estimated investment costs:

-

Bitcoin mining infrastructure: Approximately $700,000–$1,000,000 per MW

-

AI data center: Approximately $8,000,000–$15,000,000 per MW

Because AI offers more stable returns, many companies are shifting capital into this sector.

Potential Future Developments

If Bitcoin prices rebound, mining profitability could improve.

Market expectations:

-

If BTC returns to $100,000 → Hashprice may recover to about $37

-

If BTC approaches its historical high of $126,000 → Hashprice could rise to around $59

If prices remain below $80,000 for an extended period, some high-cost mining operations may be forced to shut down.

Summary

From late 2025 to early 2026, the Bitcoin mining industry is undergoing a period of transformation. Price declines and hash rate competition are squeezing miner profits, while rapid growth in AI and high-performance computing is making data centers more commercially attractive. Looking ahead, the industry may gradually divide into two roles: some companies will become AI infrastructure providers, while others will focus on sustaining mining operations with low-cost energy. Overall, Bitcoin mining remains resilient, but the industry structure is steadily changing.