Derivatives are not designed to make markets more complex, but to enable more precise risk management. They originate from real economic needs: farmers wanting to lock in crop prices, businesses aiming to hedge against exchange rate risk, and investors seeking to manage market volatility.

As derivatives have evolved, they have developed three core functions:

- Hedging risk

- Amplifying leverage

- Enhancing price discovery efficiency

Understanding derivatives is not about memorizing product names, but about grasping how they change the distribution of risk.

Futures and Forwards: Locking in Future Prices

The emergence of futures and forwards comes from a practical question: If future prices are uncertain, can I fix them now?

Forwards are the earliest form—an over-the-counter (OTC) agreement between two parties to settle an asset at a set price at a future date. Forwards are flexible but carry credit risk due to the lack of a central clearing mechanism.

Futures are a standardized upgrade based on forwards, traded on exchanges with clearinghouses guaranteeing settlement, significantly reducing default risk.

Key mechanisms of futures include:

- Standardized contract terms (quantity, delivery time, type)

- Margin requirements

- Mark-to-market daily settlement

- Forced liquidation mechanism

Futures are used not only for hedging risk but also as tools for speculation.

For example:

- Agricultural producers short futures to lock in future selling prices

- Investors go long on stock index futures to express bullish market expectations

The existence of futures markets allows future prices to be traded openly today, greatly enhancing price transparency.

Options and Volatility Pricing Logic

If futures lock in direction, options lock in rights. Options give holders the right—but not the obligation—to buy or sell an asset at a set price at a future date. Thus, option buyers pay a premium while sellers take on potential risk.

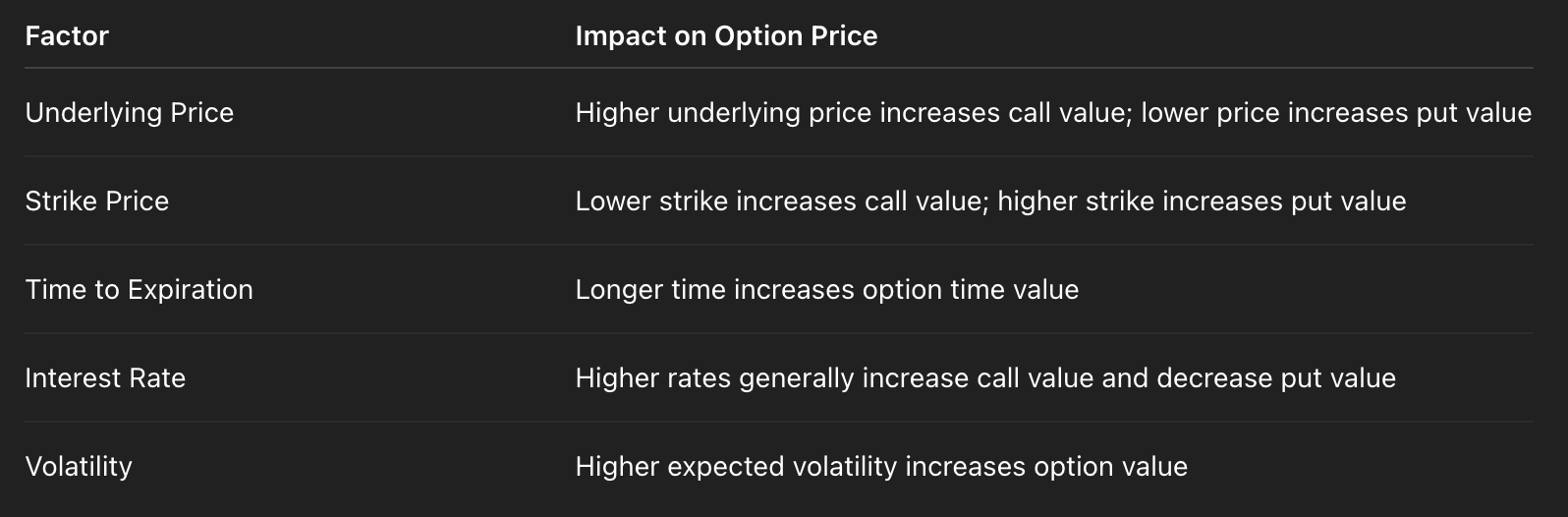

Option prices are influenced not only by the current price of the underlying asset but by several variables:

The most critical variable is volatility. The higher the volatility, the more valuable the option, as large price swings become more likely. Therefore, options markets are essentially trading the degree of future uncertainty, which is why implied volatility is seen as a key indicator of market sentiment.

For example:

- When the market panics, demand for put options rises and implied volatility increases

- When the market is calm, volatility falls and option prices become relatively cheaper

Options allow investors to bet not just on price direction but also on the likelihood of significant price movements.

Swaps and Structured Products: Risk Transfer Mechanisms

A swap is a contract to exchange future cash flows. Its core is not asset trading but exchanging risk structures.

The most common example is the interest rate swap:

- One party pays a fixed rate

- The other pays a floating rate

Through this mechanism, companies can convert floating-rate loans to fixed-rate structures or vice versa.

The essence of swaps is transferring one type of risk exposure to another party more willing to bear that risk. Structured products build on this by combining multiple derivatives. For example:

- Combining bonds and options to create principal-protected products

- Splitting cash flows of different maturities to create tiered return structures

Such products use financial engineering to break down risk into various levels and sell them to investors with different risk preferences.

Risk does not disappear; it is redistributed.

How Derivatives Enhance Market Liquidity

The size of derivatives markets often far exceeds that of spot markets—and this is no accident.

Derivatives enhance liquidity by:

- Providing hedging tools so market makers can quote tighter spreads

- Lowering capital requirements (leverage mechanism)

- Attracting more types of market participants

- Creating a more efficient price discovery process

When an asset has active futures and options markets:

- Bid-ask spreads in the spot market narrow

- Large trades are absorbed more easily

- Price movements better reflect real supply and demand

Derivatives are not merely appendages to spot markets; they are key engines driving spot market liquidity.