Trade

Basic

Futures

Futures

Hundreds of contracts settled in USDT or BTC

TradFi

Gold

Trade global traditional assets with USDT in one place

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Participate in events to win generous rewards

Demo Trading

Use virtual funds to experience risk-free trading

Earn

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and enjoy airdrop rewards!

Futures Points

Earn futures points and claim airdrop rewards

Investment

Simple Earn

Earn interests with idle tokens

Auto-Invest

Auto-invest on a regular basis

Dual Investment

Buy low and sell high to take profits from price fluctuations

Soft Staking

Earn rewards with flexible staking

Crypto Loan

0 Fees

Pledge one crypto to borrow another

Lending Center

One-stop lending hub

VIP Wealth Hub

Customized wealth management empowers your assets growth

Private Wealth Management

Customized asset management to grow your digital assets

Quant Fund

Top asset management team helps you profit without hassle

Staking

Stake cryptos to earn in PoS products

Smart Leverage

New

No forced liquidation before maturity, worry-free leveraged gains

GUSD Minting

Use USDT/USDC to mint GUSD for treasury-level yields

More

This Week's External Market Highlights | Will Trump's State of the Union Address, Nvidia's Earnings Report, and the US-Iran Situation Shake Up the Market?

Last week, the international markets experienced turbulent changes. Tensions between Iran and the United States continued to escalate, pushing oil prices higher. The U.S. Supreme Court overturned the Trump administration’s tariff decision, igniting market reactions.

In terms of markets, U.S. stocks closed slightly higher, with the Dow Jones gaining 0.25% for the week, the Nasdaq rising 1.51%, and the S&P 500 increasing 1.07%. The three major European indices performed well: the FTSE 100 rose 2.30%, Germany’s DAX 30 gained 1.39%, and France’s CAC 40 increased 2.45%.

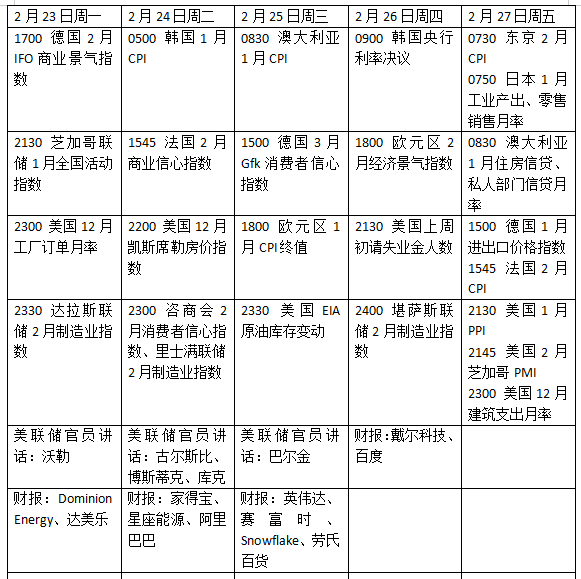

This Week’s Highlights

There are many key events this week. The ongoing escalation of tensions between the U.S. and Iran will continue to be a focus for investors. The impact of the Supreme Court’s decision to overturn Trump’s tariffs will also attract attention. Meanwhile, investors will closely monitor U.S. economic data to gauge the Federal Reserve’s next move on interest rate cuts. President Trump’s State of the Union address on the 24th will also draw market focus. In Europe, inflation data and confidence surveys will be central. Asian markets will reopen after the Lunar New Year holiday, with South Korea and Thailand releasing economic data and making central bank policy decisions.

Nvidia Earnings Ahead

The latest Federal Reserve meeting minutes show that officials are not strongly inclined to cut rates; several policymakers even indicated that if inflation remains high, further rate hikes are possible. Data shows that the personal consumption expenditures (PCE) inflation indicator favored by the Fed unexpectedly accelerated in December, and January employment growth was robust.

On the other hand, U.S. economic growth in Q4 2025 slowed more than expected, with an annualized growth rate of only 1.4% after seasonal adjustment. London Stock Exchange Group (LSEG) data indicates that the U.S. money market has fully priced in two 25 basis point rate cuts by the Fed this year, with the first cut not expected until July. LBBW analysts believe that the minutes increase the risk of only one rate cut this year.

On the data front, the Producer Price Index (PPI) for January, to be released on the 27th, will provide more clues on inflation. HSBC economists expect PPI to rise 0.3% month-over-month, with the year-over-year rate slowing from 3.0% in December to 2.8%. Other notable data include the February Conference Board Consumer Confidence Index and the December S&P Case-Shiller Home Price Index.

It’s also worth noting that the U.S. will conduct auctions for 2-year, 5-year, and 7-year Treasury bonds this week. Investors will focus on foreign demand, as recent fluctuations in U.S. Treasury yields suggest continued market interest.

As earnings season winds down, Nvidia, the AI giant, will undoubtedly be the biggest focus. Additionally, results from S&P Global, Home Depot, Lowe’s, and Berkshire Hathaway will be closely watched. Chinese concept stock Alibaba will also report earnings.

Crude Oil and Gold

Geopolitical tensions pushed oil prices higher. WTI crude futures for the near month rose 5.57% to $66.39 per barrel, and Brent crude futures increased 5.92% to $71.76 per barrel.

Both contracts hit six-month highs last Thursday amid ongoing supply risk concerns in the Middle East. Over the past week, the U.S. and Iran held negotiations in Switzerland to try to break the deadlock over Iran’s nuclear program. However, early signs of progress were quickly overshadowed by U.S. accusations—Washington claimed Iran did not respond to core U.S. demands. President Trump later said he was considering limited military strikes on Iran to pressure concessions on the nuclear issue, which kept markets stable. He added that within the next 10 days, the world would likely know whether the U.S. and Iran could reach an agreement or if military action would be taken.

Morgan Stanley commodities chief strategist Martin Ratz said, “Despite the global oil market being ‘ample in supply,’ three main factors support oil prices. First, concerns over Iran. Second, large-scale procurement by clients, raising questions about how they will handle these inventories. Third, freight rates are also high. Among these, Iran remains the most prominent issue,” he emphasized.

Barclays strategists believe that although the stock markets have so far been unaffected by geopolitical noise, tensions have escalated since U.S. Vice President Vance accused Iran of not discussing a ‘red line,’ and reports of increased U.S. military deployments in the region. “Any strikes are likely to be limited and targeted (against nuclear facilities or ballistic missiles), similar to last summer,” the bank’s report states. “Given the upcoming midterm elections later this year and the government’s priority to ensure American consumers’ purchasing power, we believe the U.S. is unlikely to tolerate prolonged or large-scale increases in oil prices or casualties. If conflict is imminent, it’s likely to be short-lived.”

The precious metals market strengthened. COMEX gold futures for February delivery rose 0.74% to $1,505.30 per ounce, and COMEX silver futures increased 5.69% to $82.283 per ounce.

Due to the federal government shutdown and soft consumer spending, U.S. Q4 GDP growth slowed sharply to 1.4%. Gold prices rallied at the close. Meanwhile, after the Supreme Court’s tariff ruling, Trump announced plans for a new round of global tariffs, adding market uncertainty. Independent metals trader Dai Huang said, “It’s hard to imagine Trump stopping here; he will try to reimpose tariffs through other regulations, which will increase market volatility.” He also added that medium-term uncertainty will not scare off gold bulls.

Additionally, the PCE inflation index favored by the Fed rose 0.4% in December, higher than the 0.3% forecast. RJO Futures senior market strategist Bob Haberkorn said, “The data shows inflation remains present in the market, but weak GDP suggests the economy is not near a turning point. There are still many unknowns and uncertainties in the U.S. economy, which supports gold.”

Bank of England Rate Cut Expectations Rise

Recent economic data have not substantively changed market expectations for ECB interest rates. On the 23rd, Germany’s February IFO Business Climate Index will kick off a week of dense economic data releases, including surveys of businesses and consumers. On the 24th, France’s February business survey will be released; on the 25th, Germany’s GFK Consumer Confidence and France’s Consumer Confidence surveys; on the 26th, Italy and Eurozone’s January business and consumer surveys; and on the 27th, the European Central Bank’s Consumer Expectations survey.

Other notable data include Italy’s January CPI inflation on the 23rd, Eurozone’s January Harmonized CPI final on the 25th, and Eurozone’s M3 money supply on the 26th. France, Spain, and Germany will release preliminary February inflation data on the 27th. Germany and France will publish detailed Q4 2022 GDP data on the 25th and 27th.

However, the more discussed topic is the rumor that Lagarde may step down early before November 2027. The final successor could be a German, or a less hawkish candidate to ensure a smooth transition and prevent euro appreciation. Attention is also on the possibility that if Lagarde leaves early, it would be the first simultaneous appointment or replacement of both the Fed and ECB presidents, adding rare uncertainty to markets.

This week, UK economic data will be relatively light. Key releases include the February GFK Consumer Confidence Index and Nationwide House Price Index. After recent soft employment data, the Bank of England’s rate cut in March is increasingly likely, and investors will monitor all data closely. LSEG data shows the market currently prices in a 78% chance of a rate cut next month.

Meanwhile, domestic political developments will be a focus: a by-election in Gorton and Denton on the 26th could challenge Prime Minister Starmar’s leadership if the Labour Party suffers a heavy defeat.

This Week’s Focus

(Article source: Yicai)